Is It Smart to Buy a Fixer Upper or Run-Down House?

I have bought many houses that needed work. I flip houses, own rentals, and have bought multiple houses to live in. Some of the houses I have bought needed minor repairs, some were major fixer-uppers, and some were not run down at all. It is my business to buy houses and repair them or rent them out. What about those who don’t know as much about real estate or those who know absolutely nothing about fixing up houses? Should they buy houses that need work? Should they invest in run-down homes? Or, should they stick to homes that are in good shape? There are many things to consider when buying houses that need a lot or a little work. I will go over some things to watch out for and why it may or may not make sense to buy a house that is not move-in ready!

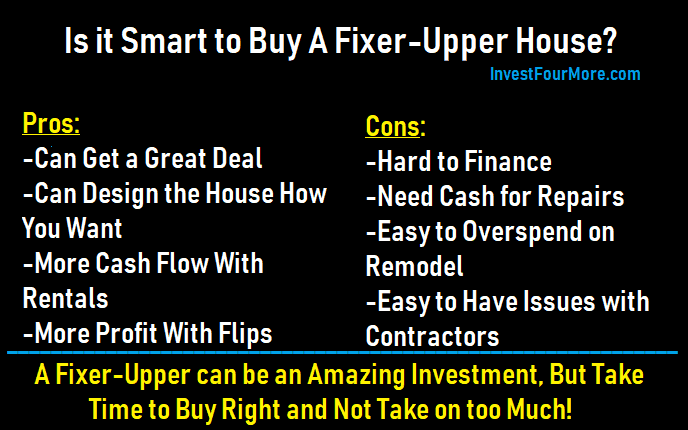

What are the advantages of buying a fixer-upper?

The biggest reason to buy a house that needs work is that you will get a good deal. The point of buying a fixer-upper is not so that you can practice interior design or carpentry but to build equity. It is harder to finance houses that need work, and it takes time and money to repair a house. You need to make sure you are getting a great deal if you go down this path!

It does not make sense to buy a house that is worth $150,000 after it is fixed up for $100,000 and then spend $50,000 remodeling it. All you did was break even. Plus, you went through the hassle of remodeling a house. When you buy a fixer-upper, you want to buy the house for $80,000, spend $30,000 fixing it up, and have the after repaired value (ARV) be $150,000. Now, you just built $40,000 of equity, and the hassle of fixing up the property should be worth it.

When you get a really good deal like this, you may even be able to refinance the house and get all or most of the money back that you spent repairing the property. I did this on the second house I bought to live in. I was able to refinance the property and get $50,000 back tax-free, which I then used to buy my first rental property.

If you are a real estate investor, you may have to buy a property that needs work if you want to flip houses or use the BRRRR strategy.

What are the disadvantages of buying a run-down house?

There are a lot of downsides to buying a fixer-upper. Don’t get me wrong—I am not trying to discourage people from buying houses that need work, but there are simply a lot of things to watch out for. I am a strong believer in the power of buying real estate below market value if you do it right. To do that, many properties I buy have something wrong with them. Here are some of those issues:

Hard to finance

It can be really tough to get a loan on a house that needs work. If only cosmetic repairs are needed, it may not be a problem, but if major repairs are needed, most banks will not want to lend on the home. Notice I said hard…not impossible. Many local banks will have fewer restrictions when buying houses that need work, and the 203k FHA rehab loan was built to finance properties that need repairs.

Hard to find contractors

It can be tough to find good contractors at a reasonable price. This is my biggest roadblock when fixing up houses, but we also do from 20 to 30 flips a year. It is easy to find contractors who will charge top dollar but much tougher to find affordable contractors who will do decent work. You have to take your time vetting contractors, and you have to keep an eye on them. I wrote a very detailed article on exactly how to find them and manage them here.

Don’t get ripped off

If you find a contractor to do the work, you need to take steps to make sure they do not take off with your money or do crappy work. Do not pay them too much money upfront. Make sure you are approving the materials used and the prices for those materials. Make sure the work you are doing makes sense and you are not going overboard.

Takes more cash

If you find a home that needs work, and you can get the bank to finance it, that does not mean the bank will finance the repairs. You will most likely need cash to pay for the work on the home unless you do a 203k rehab loan. When you see TV shows where the buyers have a $100,000 remodeling budget, that is usually not realistic. The bank is not giving those buyers the money. It usually costs more to fix up a house than you think it will.

Takes more time

It can take months to fix up a home. If you are planning to live in the home, that could mean waiting until the work is done or living with contractors in your house for weeks or months. If you are an investor, every day that goes by is money out of your pocket. It almost always takes more time to get the work done than you think.

It is not easy to buy a house that needs work, but if it were easy to gain $40,000 or more in equity, everyone would do it.

The video below goes over some of the costs to fix up a house:

How to find a fixer-upper

If you have decided to move forward with buying a run-down house, how do you find it? It should not be too difficult to find houses that need work, but it is tougher to find deals that make sense. If you are new to real estate, buying a home from the MLS is probably the best bet. If you are buying a home to live in, many distressed sellers give priority to you as a buyer. HUD homes (government-owned foreclosures) and many banks want owner-occupied buyers to purchase their foreclosures. The key to finding a great house is finding a great real estate agent to help you find that house.

When you are buying a house, it almost always makes sense to use a real estate agent. The seller typically pays for the buyer’s agent, and the agent has access to the MLS. There are good deals on the MLS system (I buy deals to flip there all the time). Plus, it is easier to buy from the MLS. You will most likely have a chance to inspect the home and get an appraisal for the loan, and HUD homes and foreclosures are usually listed on the MLS, although there are other deals on there as well.

If you want to look into more advanced ways to buy houses, I have a lot of additional information, but these techniques usually work best for experienced investors.

- Wholesalers: A wholesaler finds off-market deals that they sell or assign to an investor. There is usually no inspection and often no way to get a traditional loan on these.

- Off-market: Off-market means the home is not listed for sale. Wholesalers or investors find these deals by sending mailers, driving for dollars, websites, social media, or networking.

- Auctions: There are foreclosure sale auctions and many other types of auctions. Usually, you need cash to buy from an auction and will have no inspection.

- FSBO: For-sale-by-owner homes can offer an opportunity for any buyer to get a great deal. You can find them on Zillow, Craigslist, or just a sign in the yard.

How to finance a run-down house

Finding a run-down house may be easier than financing it. The trouble with financing houses that need work is most lenders have pretty strict guidelines when it comes to loaning money. They want a house that is in “livable” condition. That means all the major systems must be in working condition. The HVAC, plumbing, electrical, roof, foundation, and structure must be in good shape. You also cannot have any peeling paint, broken windows, holes in the walls, or a few other things.

“Good shape” does not mean the house is updated and everything is new: it means that everything works. The kitchen can be 50 years old and you can have shag carpet and a bathroom from the 1970s and still get a loan. Buying a house that just needs cosmetic repairs can be a great way to build equity without getting into a remodel that will break the bank and cause loan problems.

If you really want to buy a house that needs a lot of work, there are loan options:

Portfolio lender

A portfolio lender is a local bank that lends its own money and keeps loans in house. Because of this, they sometimes have fewer restrictions on the condition of homes. They may finance a house that has plumbing problems, bad electric, or needs a new roof. The terms may not be as good as a traditional lender, but they could be close. Investors and owner-occupants may be able to use this loan.

FHA 203k loan

The FHA 203k loan is for owner occupants only. The buyers can buy a house that is burned down with some versions of the loan and rebuild it from scratch. There are limitations with how and who does the work, but the repairs can be fully financed within the loan. The loan is more expensive than a traditional FHA loan since two appraisals are required and the interest rate is higher.

Hard-money loans

Hard-money lenders are not banks but businesses that lend money on real estate investments. They charge much higher rates than banks but will finance almost any property if the numbers make sense. Hard-money lenders will not lend to owner-occupants, only investors. Hard-money lenders will also finance the repairs, but usually not upfront. Once a certain percentage of the repairs are made, the hard-money lender will reimburse the borrower.

Escrows

In some cases, a lender may escrow money for repairs to be made after closing. This usually occurs when the repairs are minor but the seller cannot or will not complete them. The house may need a new furnace, but the seller has no money to replace it, or the house may be a HUD home and HUD will not make any repairs prior to closing. The lender might (not always) approve an escrow amount to be held by the closing company for repairs to be made after closing.

How big of a remodel should you take on?

How big of a remodel you ch0ose to take on depends on how much experience, time, and money you have. If you have never bought a fixer-upper, I would suggest not buying a house that needs a full-blown remodel or that is gutted. I have been remodeling houses for almost 2 decades, and I try to stay away from the big jobs as well. There is so much that can go wrong and so many things you will not know about until you start the job. Big remodels are also very taxing on contractors, and they may take on more than they can handle, causing even more problems.

I would also be careful about buying houses than are more than 50 years old. The older a house is, the more problems that will come up, even if it looks to be updated or well maintained. The old saying “They don’t make them like they used to” is right on many levels. I have seen old houses with literally no foundation that were sitting on dirt. I have seen old houses with rocks supporting walls, and I have seen old houses with duct tape seeming to be what was holding it up.

Newer houses can have problems as well, but there is less risk that they will have major issues. Before you buy a house, I would suggest getting a home inspection completed so that you know how much work is needed. An inspection will not find everything that is wrong, but it should give you an idea of the major problems. I would be very careful about buying houses that need:

Major electrical work

Many houses need some electrical work, but major electrical problems can not only be expensive to fix but also dangerous. If a house needs electrical work, get it checked out by an electrician to see how serious it is and what it will take to get it fixed. You could be looking at $500 to $15,000 to repair the electrical depending on the severity of the problems.

Major plumbing work

Many houses have minor plumbing issues, and some houses have major problems. It is a similar situation to the electrical system on a house where you need to get it checked out by a professional. If a house has galvanized pipes, the entire plumbing system may need to be redone. Not only are you replacing pipes, but the plumber has to cut into walls, and there will be many repairs needed after the pipes are replaced as well.

Foundation or structural work

We have fixed many foundations over the years. Some have been easy fixes and some major projects. Most foundation problems are not serious, but again, you need a professional to check out the problems. It is also important to get multiple opinions on the fix. We have had one company tell us a foundation would be $84,000 to repair and another $5,000 to repair. You can see the video of that house below:

Meth or Mold Remediation

Mold can be a major problem that either requires tens of thousands of dollars of work or can be sprayed and removed easily. The same goes for a house that has had meth used in it or been a meth lab. Some houses that have a little bit of meth residue may be remediated easily while others need to be entirely gutted. It is important to get multiple opinions on these issues as well because some companies love to overcharge for scary issues like mold, and meth.

Additions added

Adding on to a house can seem like a great way to add space and value, but be very careful. Most additions cost more than the value they add and are a very involved process. First, you must get a permit in order to add to a house unless you want to run into major problems down the road. Second, additions are expensive and it can be tough to make them flow well with the house. In some cases they make sense, but it is rare, and the market must be able to support the increased value because if your house is bigger than all your neighbors’ homes, it will be tough to sell.

Conclusion

Buying a fixer-upper can be a great way to build wealth with little money. However, be very careful with how big of a project you take on, and make sure the hassle of fixing up a house is worth it. It could take a long time to find the right deal that makes sense. If you do not have any experience in the real estate business, be wary of taking on any huge projects. Luckily, if you plan to live in the home, many banks and HUD give priority to owner-occupied buyers. There are opportunities for homeowners to get some awesome deals.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

you mentioned in one of your videos that to add air conditioning to a house would only be about $3000, I don’t see how that’s possible when we had to replace our air conditioning in our 3000 square-foot home and we did not have to add ducks just add the two machines one on the outside that big square one and one upstairs in the roof and that alone was about $10,000 because you have to buy the units I’d really like to know what you did for $3000 because many homes I look at that I like only have window units

Most our houses are 1k to 1.5k square feet and have one unit.

do you flip homes that actually have curb appeal? And do you do the outside as well,, most flipped homes that I have seen are gray/ white and they do the inside and the outside of the home and leave the rest ..like the backyard and the front yard and the old torn up shacks in the backyard just like it is and broken down fences I don’t call that completely doing a job .. we are senior citizens and certainly won’t do that kind of work and we are looking for a home within an hour and a half anywhere around Dallas Texas, so we can live near our son right now we are in Houston and we’re looking at homes under 200,000 and I will tell you that some of the flips which I won’t buy are so boring brand white and sometimes the workmanship like tile work and caulking are really crappy God only knows what’s going on behind the walls, and I don’t know how to find a flipped home that was done by an experienced flipper that takes pride in their work and uses quality Everything

That is a very tough price range to find a remodeled home in with construction costs as high as they are