How to Live for Free by House Hacking

[lmt-page-modified-info]

House hacking involves buying a multifamily property, living in one unit, and renting out the other units. House hacking can be a great way to start buying rental properties because you can buy with low-money-down owner-occupant loans and still collect rent right away. House hacking can make it much easier to buy multiple rentals quickly without a lot of money. You can also house hack a single-family home, but you have to be careful with zoning laws. With the right properties, you should be able to live for free in a property, or at least come very close to living for free.

How does house hacking work?

House hacking is a simple idea, but it can take some work to implement it. Here are the basic steps:

Get qualified for a loan by a lender

Before you can house hack, you need to make sure you can get a loan. It is easier to get an owner-occupant loan than it is an investor loan, which is one reason why house hacking is a great real estate investing technique for beginners. A good real estate agent can get you in touch with a good lender. It is important to use a good lender because bad lenders are one of the most common reasons real estate deals fall apart. It is usually best to use a local lender who is familiar with the customs for purchasing properties in your area. If there is a problem with your credit or qualifying for a loan, a lender can help you fix it for free!

Figure out what an amazing deal would be for you

There are many ways to house hack. Some people do it with multifamily properties while others do it with single-family homes. I am a huge proponent of there being no best way to do something in real estate. Everyone is so different that you need to figure out the best route for you to take. Figure out what kind of property you want, where you want it to be, and what the numbers will look like as far as income, expenses, and if you will be paying anything for the mortgage or making money.

Figure out how much money you need

When buying a house, many people are clueless. They let the real estate agent and the lender dictate everything that happens. If you want to take control of your financial future, you need to be involved in the decision making including how much money to spend. Houses can be very expensive, but there are many amazing loan options for owner-occupants. After talking to a lender and then deciding what type of property you want, you should be able to come up with a dollar figure for the property and how much cash you will need to purchase it. If you do not have any money, your first goal should be to work like crazy to save as much money as you can so you can buy your first house hack.

Find a property

If you are just starting, you will most likely want to have a real estate agent helping you track down the deal you are looking for. I highly suggest you buy a great deal even if it is not the perfect place to live for you. You need an agent who can act fast, has time for you and knows the market well. They do not have to know everything about investing, but that can help. It may take some time to find the right property, but that is okay. Buying a property is a big deal, and it does not have to happen right away.

Buy the property

This is the part that many people get hung up on because they never pull the trigger. They find the right property or properties, but they always find a reason not to buy. If you want to get ahead in life, you will have to take chances at some point. Buying a property is a big chance, but it is one that can pay off huge with less risk than you might think. You do not have to find the perfect property. You may only be living in the place for a year. If you hate it or things don’t work out like you thought they would, it is not the end of the world.

Rent out the property

Whether you buy a multifamily property or a single-family house, you may need to rent out a unit or two…or a bedroom. You must take your time finding the right tenant, especially if you are living in it. There are so many tenant horror stories from people who did not take their time finding the right person to rent from them. It does no good to house hack if your tenants will not pay you rent!

Live there for a year and plan your next move

If you buy a place as an owner-occupant, you must live there at least one year with almost every loan available. It is great that you bought a house hack, but buying one will not make you a rich person. If you really want to get ahead in life, you need to buy a lot of rentals. You need to figure out what to do after that year is up. Are you going to buy another property to hack? Are you going to refinance, take money out, and buy a regular rental property? There are a lot of options, but hopefully, this site and article can help with all of that.

Here is a video that goes over house hacking as well:

Why is it so hard to buy rentals?

There are many roadblocks to investing in real estate. When buying rental properties, you must have 20% down in most cases. There are ways to invest with little money down, but you usually have to buy as an owner occupant. I think good rental properties are usually at least $80,000 if not much more. Multifamily properties can cost $200,000 or more in an affordable market. If you live in an expensive market, houses and multifamily properties are much more expensive.

To buy a rental property as an investor, you would need at least $20,000. You will need money for the down payment and money for the reserves. Most banks will require an investor to have cash reserves for at least 6 months of mortgage payments for every property they own, including the one they are buying. You may also have to pay for closing costs, which could be 3% of the purchase price. If you are buying more-expensive rentals, you may need $30,000 or more in cash and twice that if you are buying multifamily rentals.

How can you buy properties cheaper as an owner occupant?

You can put much less money down when you buy as an owner occupant. You can get loans for as little as 3% down or even zero down with certain loan programs (VA or USDA). Banks are also less concerned with reserves on owner-occupied loans, and owner-occupied loans are easier to get than investor loans. When you buy a house as an owner-occupant, you must live in it for at least one year. Living in the house means you are there more than 50% of the time. If you are not living in the home, it could be considered loan fraud.

Why are multifamily properties used for hacking?

When you buy a single-family home as an owner-occupant, you can’t rent out the entire home for a year (because you are living in it), which can make it harder to buy multiple properties. You may need to count rental income in order to qualify for a new loan. A lot of people will live in a property for a year then try to buy another property as soon as that year is up. The problem is that many banks will not count rental income until the rents show up on your taxes. Many people do not show enough other income to qualify for two mortgages at the same time.

When you buy a multifamily property as an owner occupant (which is perfectly legal as long as it is 2-4 units), you can live in one unit and collect rents on the other units right away. This helps you build a rental history sooner, and you may be able to qualify for more rentals sooner than if you bought a single-family home. You start renting the property right away, and in a year that money will show up on your taxes.

Can you house hack a single-family property?

While it is tougher to house hack a single-family home, you can do it. There are options to rent out basements or even bedrooms. The tricky part is not breaking zoning laws. Most towns have laws that say how many people who are unrelated can live in certain “zones” of the town. In my area, most towns allow either two or three unrelated people to live in a zone.

Can you hack a property with more than 5 units?

The reason you can house hack properties with up to 4 units is they are still considered residential properties up to that point. When you have more than 4 units, almost every bank will consider the property as commercial, and you must get an investor loan. FHA loans work great for house hacking but cannot be used on any property with more than 4 units. It will be virtually impossible to get an owner occupant loan on anything with more than 4 units, and that is why everyone says to use 2 to 4 unit properties.

How should you buy the property?

Living in a house for free or making money while you live in a property is great, but you can also buy below market value. I flipped 26 houses last year and bought all of them below market value. I am a professional, but others can do it as well, and owner-occupants even have an advantage over me. As an owner-occupant you:

- Do not have to get as good of a deal as a house flipper. When I am flipping houses, I must pay financing costs, carrying costs, and selling costs…plus make a profit. As an owner-occupant, you don’t have to get as good of a deal because you won’t be flipping the property. Since an owner occupant can pay more than house flippers, they have a better chance of buying the property.

- Many banks give owner-occupants the first chance to buy their foreclosures. HUD, Fannie Mae, Wells Fargo, and many other banks have an owner-occupant bid period only at the start of the listing period. That allows owner-occupants to make offers before investors.

Buying properties below market value has many advantages. You make more cash flow because the mortgage payments are lower and you build instant equity. That equity comes in handy if you decide to sell the property or refinance it later on.

What kind of loan can you get?

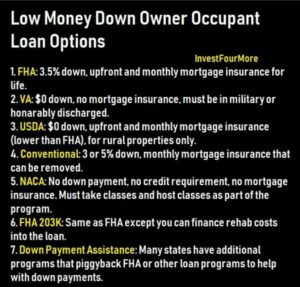

FHA

FHA will allow up to a 4-unit property with their loans as we just discussed. FHA loans have as little as a 3.5% down payment, but they also have mortgage insurance. Mortgage insurance will add a couple of hundred dollars a month to your payment, and you have to pay a certain amount upfront. However, the upfront mortgage insurance can be financed into your loan with an FHA loan. Most owner-occupant loans will have mortgage insurance, although VA does not.

The downside to an FHA loan is the mortgage insurance is expensive and it cannot be removed. With other loans, mortgage insurance may be able to be removed when there is 20% or more equity in the property.

VA

VA loans will also let you finance properties with up to 4 units just like an FHA loan. VA loans can only be obtained by those who are in the military, veterans, or honorably discharged. The VA loan is one of the greatest benefits available to those who are in or have been in the military. VA offers zero down and no mortgage insurance.

Conventional

You are only allowed to have one FHA mortgage in your name, but that does not mean you cannot buy more properties with conventional loans or VA loans if you qualify. Conventional loans have down payments as low as 3% for owner-occupants, have lower rates, and often have mortgage insurance that can be removed. I think the conventional loan is better than FHA unless you are trying to max out your buying power. Conventional loans have cheaper mortgage insurance and often cheaper rates as well.

Some lenders or agents will tell you that you cannot use an FHA loan on a multifamily property, but they are wrong. It says right on the FHA website that you can.

Can you buy a house hack that needs work?

I think buying a great deal as an owner-occupant is one of the best ways for the average person to get ahead in life. One issue that comes up with this strategy is that good deals often need work. I flip a lot of houses. Some of those need a little work and some are full-blown gut jobs down to the studs. If you are buying a property without much experience in real estate investing, I would suggest not buying massive remodel projects.

In fact, many lenders will not give you a loan if the property needs too much work. Owner occupant and even investor loans with conventional lenders require properties to be in livable condition. That does not mean they cannot need any work, but it means they must be in relatively decent shape. Here are some things the lenders will look out for:

- Holes in the drywall: most banks want to see the walls and ceilings intact. That means no holes in the drywall.

- Major system damage: the plumbing, electrical, HVAC, roof, and foundation all need to be in decent shape and in working order.

- No peeling paint: most loans will not allow peeling paint, even though it seems like one of the most minor repairs there is.

- No broken windows or doors.

- Must have a working kitchen and baths: you need to have a kitchen and bath that is not gutted or inoperable.

While some of these repairs may seem minor, you do not need flooring. You can have bare subfloor or plywood as your floor and still get a loan. You do not need a fridge, oven, or dishwasher either. The yard condition does not affect the loan unless there is water pouring into the basement from poor grading.

If you want to buy a house that needs some work, you need to make sure the loan you are getting will not be denied because of that work. If you are buying your first place, you do not want a place that will need to be gutted anyway. Find a property that needs cosmetic repairs, and you should be okay.

How does the lender use an appraisal?

When you first buy a home, you usually get an inspection done to see what shape the property is in. That inspection is usually not shared with the lender, so how does the lender know how much work the property needs? The buyer could tell the lender, but that is not usually a smart choice. Even if the buyer keeps their mouth shut, the lender will order an appraisal on the property. The appraiser will inspect the property for major problems but will not look as closely as an inspector will. If the appraiser sees obvious problems, he will call them out and request them to be fixed prior to closing (when the house sells).

If the seller is not willing to fix any items the appraiser calls out, the loan will not go through and the deal dies. The appraiser will also want to make sure the utilities are on and working. Finally, the appraiser will value the property to make sure the bank is not lending much more money than what the property is worth.

What options are there for a property that needs a lot of work

If you have your heart set on a property that needs a lot of work, there are some options available:

Seller repairs

In some cases, the seller may be willing to make repairs to the property to bring it up to lending condition. When you are getting a really good deal, there is often a reason for it. That reason usually involves the seller not wanting to make any repairs or selling the property in as-is condition. It is rare, but in some cases, the seller will be willing to make some repairs if the appraiser calls them out.

FHA 203k loan

Another option is the FHA 203k loan. The 203k loan allows the buyer to finance the repairs into the loan. There are two different 203k loans: the streamline and the full-blown 203k. With the 203k streamline, you can only make certain repairs, but the loan is quicker and easier to get. With the full-blown 203k loan, you can build three more stories if you want. There is no limit to the number of repairs you can do.

The 203k loan is not easy to get. You will need two appraisals: one of the as-is value and one for the value once the property is repaired. The buyer will have to qualify for the final loan amount after the repairs are completed, not just the initial purchase price. The loan also takes longer than a regular FHA loan or conventional loan, which means fewer sellers will be willing to accept 203k financing. You also must use contractors who are approved with the 203k loan program. You cannot do the work yourself.

A 203k loan is a great option for those who can make it work, but it is not easy to pull off.

What are the disadvantages of house hacking?

House hacking is a great way to start buying rentals, but it takes some sacrifice. When you buy as an owner-occupant, you have to live in the property for at least one year. If you are buying a multifamily house, you will have to live in one unit of the property for at least one year. You can’t just leave one unit vacant and pretend to live there.

Depending on what stage of your life you are in, living in an apartment can be fine or a nightmare. If you are a single college student, you are probably used to living in apartments. If you have a family and kids, you may be used to living in nice single-family homes. It would be very difficult to move into an apartment in a multifamily property if you are used to nicer properties.

I personally would never move into a property to house hack at this stage in my life, but I also do not need to. I also have a five-car garage, and it would be tough to find that in a multi-nit building! To really take advantage of house hacking, you should move very frequently to buy multiple properties with low down payment loans. It is not fun moving every year or two with a family either. While it is a great strategy to use, it is not for everyone.

Do you have to refinance the loan after one year?

When you buy a house as an owner-occupant, you do not have to live in the house as long as you have that loan. The loan requires you to live in the house a certain amount of time, but that does not mean when you move out you cannot keep the loan. I have had lenders claim you must refinance the property if you move out, but when I asked them to show me that clause in writing in the loan documents, they could not do it. If you are planning to buy a house to live in and then turn it into a rental, it is wise to read the entire loan contract and not blindly trust what your lenders says. If they say something that does not sound right, make them show you the clause in writing.

That does not mean you cannot refinance if it makes sense to do so. FHA mortgage insurance stays with the loan until the loan is paid off. If you bought the property below market value as we discussed earlier in the article, you could refinance into a conventional loan. If you have at least 20% equity in the property you may be able to get a new loan and eliminate the mortgage insurance without bringing any cash to the deal. You may even get cash back to invest in new properties.

Cash-out refinance strategy (BRRR)

Here is an example of how the refinance could work.

- Buy a property for $150,000 that is worth $190,000 with an FHA mortgage

- Wait a year or 6 months and then refinance the property into a 20% down conventional loan

- If the appraisal comes in at $190,000, you could get a loan for $152,000 and still have 20% equity

You would break even on this deal or pay a little bit to refinance because there would be closing costs to get that new loan, but you would save a couple of hundred bucks a month in mortgage insurance. If you got a better deal, the property increased in value, or you added value, you could get a loan that pays off the previous loan and all costs plus puts money in your pocket. Plus it frees you up to get another FHA loan if you want to go that route.

What do you do after the year is up?

Different loan types have different requirements, but most loans require an owner occupant to live in a house for one year. After that year is up, you can sell the house or rent the property out. If you lived in one unit of a multifamily house, you could rent out that unit after living there one year. You have to live in the property more than 50% of the time to be considered an owner occupant. You can’t leave one unit vacant and pretend to live there.

After renting out the unit you were living in, you could then buy another rental as an owner occupant and repeat the process over and over. As I already discussed, it is easier to qualify for more loans when you have a longer rent history. House hacking makes it easier to buy more rental properties more quickly than buying a house to live in and collecting no rent if your debt-to-income ratios are tight.

If you buy the right multifamily property, you may be able to live there for free or even make money while you are living in one unit. For example:

- 3 unit property with 3 bedroom 1 bath units and rent is $800 per unit.

- The property cost $150,000, and with a 3% down the payments would be $900 per month (including mortgage insurance).

- With taxes, insurance, maintenance, and vacancy costs the total monthly expenses would be about $1,450 to $1,550 depending on what taxes are in your area.

- You would bring in $1,600 per month in rent, which is less than your monthly expenses, and you get to live in the property for free (excluding utilities). When you move out, your cash flow would increase even more.

This kind of deal is not available in all markets, but they are out there.

Is house hacking worth it?

House hacking takes some sacrifice and hard work. You not only need to do everything you would do to buy a house normally, and you need to rent out the property and find a great deal. I think house hacking is definitely worth it for those looking to get ahead in life. There are very few ways to invest in real estate with little money, and this is one of the best ways to do it. One year may seem like a long time now, but it goes by very fast.

Conclusion

House hacking can be a great way to get started buying rental properties with little money down. It can also be a great way to buy more rental properties faster because it makes it easier to qualify for new loans. House hacking is not for everyone, especially if you have a family that would disown you or the numbers don’t work for multifamily in your area.