What are the Best Loans for Financing Investment Properties?

Rental properties are great way to invest your money, but qualifying for a loan on an investment property is not always easy. Loans for financing investment properties are much more difficult to get than a loan on an owner-occupied home, and it will cost you more money as well.

Many banks consider investor loans riskier than owner-occupied loans. The down payments are higher, the credit scores needed are higher, and the income requirements are greater for investor loans. This article will go over the different loans available on investment properties and how to qualify for them.

What is considered an investment property?

An investment property could be a rental property, a house flip, or a piece of vacant land. Banks are very specific regarding what they consider investment properties, and they base their loans on these classifications. Most banks lend on owner-occupied houses and investor-owned houses. Almost every bank has different loan options depending on what type of property you own.

Each bank can have a different definition, but for the most part, an owner-occupied home is a house that someone lives in for more than 6 months of the year. It is not a house that someone buys and stays in for a week on vacation. It is not a house that someone buys, leaving one room vacant in case they decide to crash there one night. One or more people on the Deed must live in the home more than half the time for at least one year (sometimes more). All other houses are considered investment properties, and the banks have much different loan programs for them than for owner occupants.

If you buy a house as an owner occupant with the intention of using it as an investment, it could be considered loan fraud. If you pretend to be an owner-occupant on a HUD home, it could even be a felony with potential prison time!

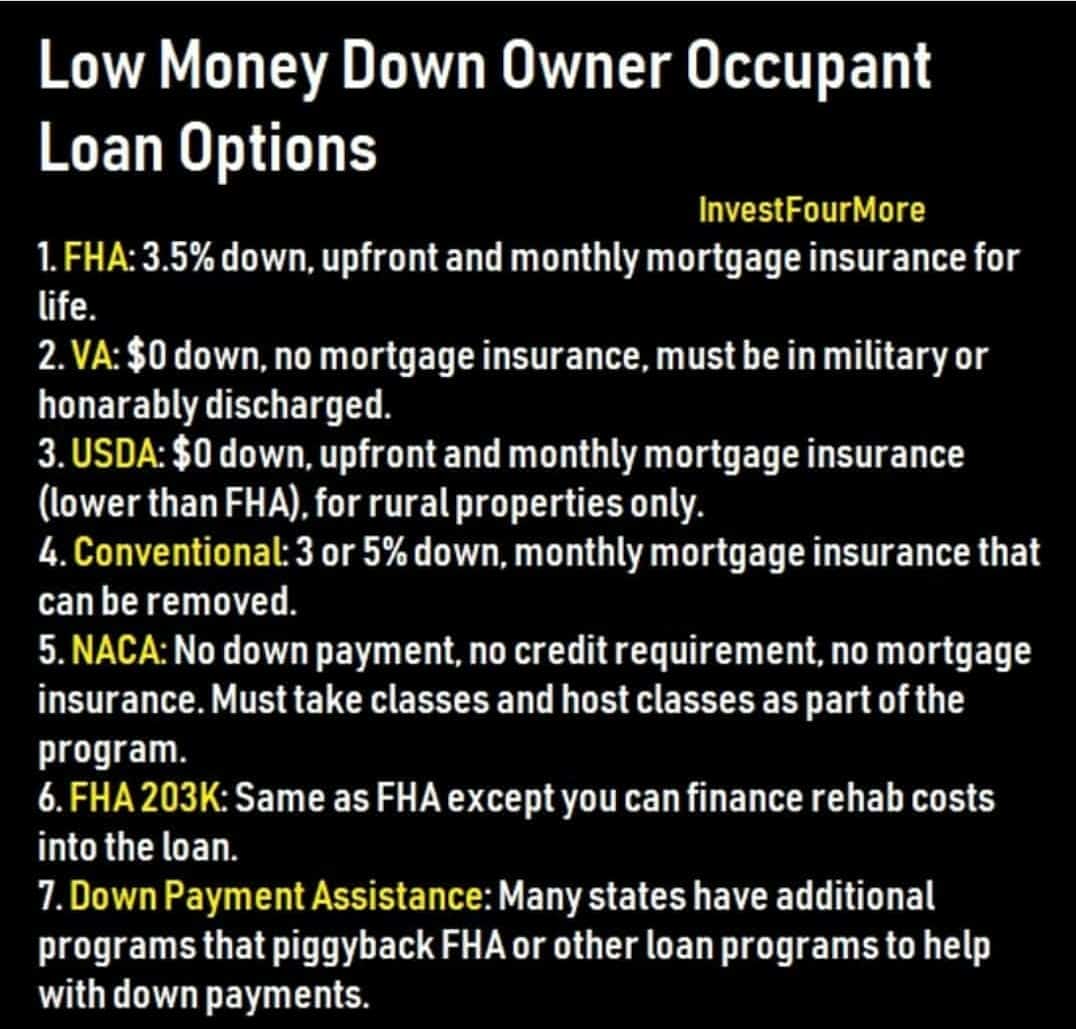

Owner-occupant loans

Owner occupants can typically qualify for FHA, VA, Conventional, USDA, or other loan options that have low down payments. The down payment for FHA can be as low as 3.5%. VA has a $0 down payment as does USDA. Conventional loans also have down payments as low as 3 percent for some buyers and 5 percent for most buyers. It is fairly easy for most buyers to qualify for an owner-occupied home if they have decent credit (over 620), make decent money, and have reasonable debts.

If you want to get into investment properties cheaper, one option is to buy as an owner occupant, live in the property 1 year (in most cases), and then rent the property out. You can also do this with a house flip, and if you live there for two years, the profit becomes tax-free in most cases!

Rental-property loans are much different. An investment loan requires at least 20 percent down in almost all cases, requires higher credit scores and better debt-to-income ratios, and there are limits to how many loans you can get with big banks. Most big banks will only let an investor have 4 loans in their name. Some smaller banks will allow an investor to have 10 loans in their name, but all the requirements get even stricter.

There are other options for investors that we will get into in this article, so do not lose hope if you don’t have the down payment, or have too many mortgages.

Why is it harder for an investor to get a loan?

Banks consider real estate investing riskier than normal home ownership. Banks figure that, if things go bad, someone will work harder to keep the house they live in than they will an investment property. The government also encourages homeownership with programs like FHA, USDA, VA, and local down payment assistance programs. Because the government helps with or runs these programs, the banks are more willing to offer low down payments to owner occupants.

How to qualify for loans for financing investment properties

When qualifying for a home mortgage, most banks look at multiple factors. One of the biggest issues investors run into is that they have to qualify for two houses if they have a loan on their personal residence. It is very important for people not to buy the most expensive house they can because of this. You must have a low debt-to-income ratio to qualify for a new loan, whether as an owner occupant or as an investor. If you max out your qualification on your personal home, it will be very difficult to qualify for a loan on an investment property.

Here is what banks look at on investor loans:

Debt-to-income ratios

You debt-to-income ratio is how much money you make each month compared to what your debt payments are each month. The percentages a bank will be okay with depends on the loan. Debt-to-income ratio does not take into account how much the balances are on your mortgages, only what the monthly payments are. Lower debt payments make it easier to qualify for a loan, and that is one reason I prefer a 30-year loan to a 15-year loan (30-year loans have lower monthly payments).

Time at a job

Most banks want to see a borrower at the same job for two years before they will give them a loan. If a borrower switches jobs but stays in the same field, banks will usually still lend, but you have to be careful when switching jobs. The bank will want to verify income to make sure you are working full time and actually have the job you say you have.

Credit score

Some loan programs allow credit scores under 600, but the lower your score, the more fees and costs you will pay. Almost all low-credit-score loan programs are for owner occupants. Investors usually need a credit score over 680 and sometimes over 720 if they are trying to get multiple mortgages in their names. You will get the best rates and terms the higher your credit score is.

Tax returns

Banks will verify your income with tax returns. If you claim very little income, it can be hard to get a loan. Many people who are self employed or who own businesses have a hard time qualifying for loans because they write off so many expenses. If you have little income, your debt-to-income ratio may be too high for you to qualify for a loan. One option is to claim fewer expenses and show a higher income on your taxes.

Foreclosures/short sales/bankruptcies

Banks do not like to lend to people who defaulted on past debts. If you had a foreclosure, it does not mean you can never get a loan again, but it makes it much tougher. Many banks will want to see a solid credit history up to 7 years after a foreclosure before they will lend to a buyer again. Other banks have shorter time frames. Short sales and bankruptcies also affect your ability to get a loan but usually have a shorter time frame than foreclosures.

What are the costs for an investment loan?

It is important to know that, when you get a loan on investment property, you need more than just the down payment. You need money for closing costs, loan costs, and reserves.

Closing costs

The closing costs on a loan consist of the origination fee, appraisal, recording fees, doc fees, and closing company fees. These costs can be up to or more than 3 percent of the loan amount. It is possible to ask the seller to pay these closing costs for you when buying a house, but it makes your offer weaker than one that is not asking the seller to pay closing costs.

Reserves

Lenders do not want an investor spending every penny they have on a house. They want to see some money left over to handle carrying costs or other issues that may come up. You need to have reserves left over after paying the closing costs and the down payment. Most banks require an investor to have at least 6 months of reserves. Reserves usually include the cost of any mortgages you have, including the property you are buying.

Interest rate

Interest rates on investor loans can also be higher than on owner-occupied loans. If the going rate on an owner-occupied 30-year loan is 5%, an investor may pay 5.5% or 6% depending on the bank. They may even pay higher rates if they have shaky credit or other issues.

What are the alternatives to bank loans?

Up to this point, we have talked about how investors can get a loan from a bank. You must be in a good financial position to get a loan from a bank. Some people do not have that luxury. So what are their options if they want to invest in real estate? There are many ways to get financing other than from big banks:

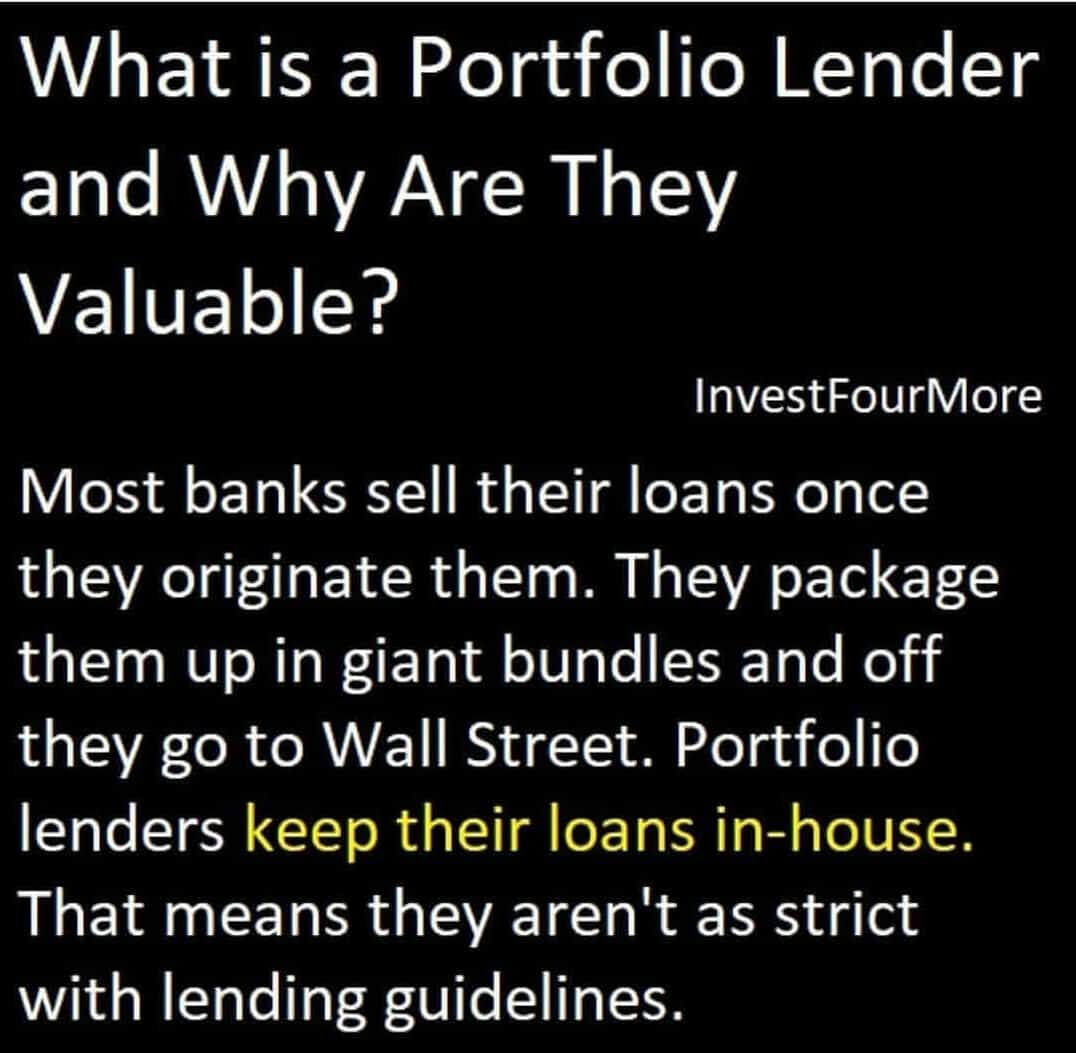

Local banks/portfolio lenders

Big banks have very strict lending guidelines because almost all of them sell their loans to other investors. Those investors set the guidelines that the banks must adhere to. Some local banks do not sell their loans and can be much more flexible when lending to investors. They are often called portfolio loans or portfolio lenders. I have gotten almost all of the loans on my rental properties from local banks.

Some local banks will also lend on house flips. They have much lower rates than hard-money lenders but require more down payment. Usually, a bank will finance 75% of the purchase price on a flip, and some banks will also finance the repairs.

Hard money

Hard-money lenders specialize in financing house flips, but they can finance rentals as well. A hard-money lender will have much higher rates than banks and will charge more fees, but most investors will have a much easier time qualifying with them than a bank. Hard-money loans have short terms (usually one year) and cannot be used on owner-occupant properties.

Hard-money loans are typically used for house flips, but you also may be able to use a hard-money loan to buy a rental and then refinance it into a long-term bank loan. I have seen hard-money rates as low as 8% recently, which is much lower than they used to be. A hard-money lender will often lend up to 90% of the purchase price and 100% of the repairs. Some hard-money lenders will finance the entire deal, but they are much more expensive, with rates above 12%.

Private money

Many hard-money lenders call themselves private-money lenders, but I think of private-money lenders as individuals. They are people you know: a family member, friend, co-worker, or another investor. I use a lot of private money on my house flips and on my rentals. Private money is easy for me because I literally send a text message or email, and the lender lets me know that day if they have money or not. Getting private money is all about relationships. I get most of my private funds from other investors.

The rates and terms for private money can vary greatly! I have some loans at 6% and others at 12%. The rate I pay depends on the lender, the deal, the time I need the money, and other factors. I am able to borrow 100% of the purchase price with most of my hard-money lenders, and one lends me 100% of the purchase price and 100% of the repairs upfront!

National rental property lenders

In the last few years, national lenders who specialize in lending to real estate investors have popped up. They are not banks but rather funds or companies that specialize in investor loans only. They have higher rates than most banks but do not worry as much about debt-to-income ratios or credit scores. They are more concerned about the property being a good rental and making money.

I have seen rates on rental properties as low as 5% with some of the bigger lenders. I have even seen 30 year fixed rate loans being offered. I am in the process of refinancing one of my properties to a 30 year fixed rate loan with one of these lenders. They will usually lend from 70% to 80% of the purchase price or value.

I have a list of hard money and rental property lenders here.

What is the best type of loan for an investor?

There are pros and cons to each loan. There is no best option because everyone has different goals, levels of experience, cash available, and different types of deals. I use different loans on my properties as well. I use bank money, hard money, and private money depending on the situation. The video below goes over the exact costs of these loans on my house flips:

This article goes into the details of financing house flips as well.

Rental property owners will usually want a different type of financing since they hold the property for longer than a flip.

This article goes into the details on getting loans for rental properties.

What is the first thing to do?

If you want to be a real estate investor but do not know where to start, I have a simple answer for you:

Talk to a lender or bank.

Even if you think there is no way they will give you a loan, go talk to them. They can tell you if you can get a loan, how much you qualify for, and what the loan will cost you. The meeting is free, and there is no reason not to do it. If the lender says you cannot get a loan, they should be able to tell you exactly why and help you fix any problems. They do all of this for free as well. Even if you want to wholesale, use hard money, use private money, or aren’t ready to invest for years, talk to a bank!

How to lower your debt-to-income ratio

One of the most common problems people have when qualifying for an investment property is a high debt-to-income (DTI) ratio. Most lenders will want to see a DTI ratio of 45 percent or lower. If your DTI ratio is higher than this, it will be very hard to qualify for a loan. I have investors emailing me all the time and asking how to get around high DTI ratios. Even my portfolio lender, who is very lenient with lending requirements, will not lend to people with high DTI ratios. However, some of the national rental property lenders and hard-money lenders mentioned prior do not care about DTI ratios.

DTI ratio is calculated by taking your monthly debt payments and dividing them by your gross income before taxes. If you have $2,000 of monthly debt and $5,000 of gross income, you would have a DTI ratio of 40 percent ($2,000/$5,000 = 40 percent). That is a very simple equation, but it is not always simple coming up with the monthly debt and income, especially if you own rental properties.

You must count the property mortgage payment against your DTI ratio. Even though your DTI ratio may be 35 percent right now, a new mortgage payment may push that number to 45 percent, and you may not qualify for the mortgage. The DTI ratio will generally be the deciding factor on how large of a loan you can qualify for. The most payments you can qualify for on a new mortgage would be the payment that pushes you to the maximum DTI ratio a lender will allow. If a lender will allow a 40 percent DTI ratio and a $1,000 house payment pushes you to 40 percent, that would be the highest payment you could qualify for.

It is your monthly income and monthly debt payments that the banks pay attention to, not total balances. If you have a $2,000 credit card balance, it may not seem that it would affect your ability to qualify for a loan. But if your payments are $200 a month, that would have a huge impact on how high of a mortgage you can get. A $200 dollar a month difference in mortgage payments can reduce the amount you qualify for by as much as $40,000!

What expenses and income are included in DTI ratios?

If you are applying for a loan, everyone who will be on the loan will have to include these figures in debt:

- Minimum credit card payments

- Auto loans

- Student loans

- Consumer loans

- Other financial obligations including child support and alimony

- Your current housing payments do not count if you are going to sell the house before you buy the new house. If you are keeping the house, you will have to count the payments as debt.

- Your estimated future housing expense, which includes principal, interest, taxes, insurance, and any HOA fees.

To calculate your income, you use:

- Your gross monthly salary before taxes, plus overtime and bonuses. Include any alimony or child support received that you choose to have considered for repayment of the loan.

- Any additional income like rental property profits. This is tricky because some lenders will not count any rental income until it shows up on your taxes. Other lenders will count 75 percent of your rental income if you are an experienced investor or have the house leased.

Usually, it is a little tricky calculating the DTI ratio because different banks calculate things differently. It is best to let the lender you are using calculate the DTI for you. If the bank comes up with a DTI that seems very high, double-check how they calculated it to see if they are doing something strange or put a wrong number in somewhere. Some banks will count depreciation of investment properties against you, even though that depreciation is not a monthly expense.

Why do different banks use different debt-to-income ratios?

Different banks use different DTI ratios, and different loan programs use different DTI ratios. VA and FHA typically limit borrowers to a 52 percent DTI ratios but in some circumstances may increase that percentage slightly. Fannie Mae allows up to a 45 percent DTI ratio on some loans, but you must have great credit. With credit scores under 700, you typically would have to have your DTI ratio under 36 percent.

As you can see, this can all get very confusing trying to figure out yourself. Here is a link to the Fannie Mae lending matrix which is even more confusing. The best thing to do is to talk to a lender, and if your DTI ratio is high, work on lowering it.

How can you lower your debt-to-income ratio?

The easiest way to lower your DTI ratio is to make more money. The more gross income you make, the higher your DTI ratio will be, but that is not the only thing lenders look at. It is not easy to simply start making more money, but many investors and self-employed individuals or business owners claim very little income on their taxes. Claiming little income is great if you don’t want to pay much in taxes. If you want to qualify for a loan, claiming little income can make it nearly impossible to buy a house. You may think you are making $10,000 a month, but if your taxes show you making $2,000 a month, your DTI ratio could be much higher than you think. Claiming more income on your taxes will mean you have to pay the IRS more, but it may be worth it if it allows you to get a loan.

Reducing debt is another way to improve your debt-to-income ratio. DTI ratios take into consideration all monthly debts that show up on your credit report. Usually, the shortest debts hurt you the most because they have the highest payments. Even though you think you are doing the smart thing by getting a 15-year loan instead of a 30-year loan on your primary house, it actually will hurt your DTI ratios. A three-year loan on a car will make your DTI ratio higher than a six-year loan. I am not saying you should always get the longest term possible on debt, but the lower your minimum payments are, the lower your DTI ratio will be. You can always make extra payments if you want to pay off your loans quicker.

What else affects the DTI ratio?

- Minimum credit card payments: credit cards typically have very high interest and very high monthly payments. If you can pay off credit cards, it will greatly improve your DTI ratio, but you must pay off the entire balance.

- Auto loans: car loans can destroy a DTI ratio! A $600 car payment is equivalent to a $120,000 mortgage and will reduce your ability to qualify for a mortgage by $600 a month.

- Student loans: student loans may have low interest and low payments, but they still hurt DTI ratios. I think it is usually better to pay off other debt first depending on what the rates are.

- Consumer loans: do you have a loan for a TV, furniture, home equity line of credit, or any other monthly payments that show up on your credit? Even a home equity line of credit that you are not using can count against your DTI ratio.

If you don’t have the money to pay off your debt, you may be able to consolidate it with a larger loan against your home that would have a lower interest rate and monthly payment.

Refinancing investment properties

A fantastic strategy to make your money go further when investing in real estate is to refinance properties. A refinance is when you get a new loan on a property that you already own. A cash-out refinance is when you get a new loan a property you already own, and the new loan pays off all other debts plus gives you back money. If you owe $80,000 on a house but refinance the property with a $100,000 loan, you would get $20,000 in cash back minus any closing costs for the new loan.

The BRRRR strategy is a great way to buy rentals with less money because you get most, if not all, of your investment back after the refinance. It stands for:

- Buy: you have to get an awesome deal (can use financing or cash).

- Repair: most houses that are awesome deals need some work.

- Rent: with most income properties the banks want a home rented out before they lend on it.

- Refinance: get a new loan that pays off any old loans, pays off the repairs, and any down payments.

Conclusion

Financing is one of the most important aspects of investing in real estate. You can make more money with loans than by paying cash. You can also multiply your money quickly using refinances, and there are many options for investors, even when you have bad credit or low income. It can be confusing figuring out what the best option is, but talking to a bank or lender is the first step.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

Does portfolio lenders offer 30 years fixed rate?do you think it is better to buy cash, rehab, then refinance than morgagte, rehab, then refinance? As a server, my w2 is horrible because mostly my income is from tip which does not show in w2. So I don’t have much choice, but to buy rental property by cash and wait for my w2 to get better and cash out refinance and hopefully qualify for the mortgage in next year or couple years.

James

Hi James, my portfolio lender does not. They only offer 5, 7 year ARMs or 15 year fixed. The ARMs have a 30 year amortization though. I don’t think many portfolio lenders offer 30 year fixed. If you have the extra cash it probably saves you money to buy with cash and then refinance, but most lenders are going to want to see you hold the home for at least a year before they will refinance for more than the purchase price. You could always show your tips on taxes, but then you’d have to pay more in taxes. A tricky situation for those in the field.

I cannot show my tips in my tax due my restaurant policy(they want to hide their “real” income), and I don’t want to pay more tax on earned income. However, last year I bought 3 rental properties; two of them are rented, but the 3rd is on rehab and ready to be rented next month. My situation is kinda strange because my this year income in w2 will be almost 100% higher compared to last year. Do you think I need to wait one more year to qualify for the mortgage? because my income inw2 suddenly go up from rent and also I heard that bank want borrower to have steadily income for year or more. Be honest I want to be qualified for mortgage now because I don’t want all of my money tied down in my properties. I rather use leverage to increase my passive income. (I strongly agree with your article about leveraging to increase ROI)

I would check with your lender and see what you qualify for now. They can usually average the last two years so you may be able to do it now.

The brand new home finance loan guidelines ended up drawn up through the Client Monetary Protection Agency, created following enactment with the Dodd-Frank Act this year. Some fresh rules are created to shield home owners coming from lender along with mortgage-service abuses.

How do you find out your personal qualifications and debt to income threshold that banks will give you loans for?

Hi Ken, Talking to a lender is the best bet. You can also try online qualifiers.

Skips the banks. Their outdated underwriting models/practices best suit the age of W-2 wage earners, not the real estate entrepreneurs of the new millenium, where speed counts and the Gig-Economy disrupts! Whether large commercial banks or community portfolio lenders, their market dominance in the sphere of lending is rapidly eroding. Income stability is shifting from W-2 to 1099, Schedule C and other forms of revenue reported to the IRS. The age of non-bank fintech lenders (be they institutional/insurance companies, private equity, et al) often require far fewer docs, since they’re not hindered by banking regulations, and actually lend on the asset’s performance, rather than the borrower who may not conform (eg self-employed, etc). There are many new mortgage products now tailored for investors, including those that factor STR Airbnb income. Mortage brokers can also supply investors with many more sources of mortgage financing than banks.

https://www.inman.com/2016/11/01/big-banks-cede-market-share-to-nonbanks/

https://thefinancialbrand.com/70240/business-banking-strategy/

http://www.bain.com/publications/articles/retail-banks-wake-up-to-digital-lending.aspx

https://gomedici.com/are-traditional-players-losing-out-on-retail-and-commercial-banking/

https://www.nytimes.com/2017/01/21/business/dealbook/quicken-loans-dan-gilbert-mortgage-lender.html

local banks can be a huge asset

In regardd to our free ebook, I would like a regular book copy, if one is available. I do not download.

I have books on Amazon you can buy hard copies of but not the free ebook