Is A 15 or 30 Year Loan Better For Rental Properties?

When considering either a 15 or 30 year loan for investing, most people choose the 15 year loan. 15-year loans may appear to save money over 30-year loans because they have a lower interest rate, but I would much rather have the flexibility of a 30-year loan. Buying rental properties is a great investment, especially when you are able to use a mortgage to buy the properties and still get great cash flow. Many investors will get a 15-year mortgage because the rates are a little lower and they can pay off the properties quicker. I use a 30-year loan when I buy my rental properties because I get more cash flow and I can make much more money buying more properties than I can be paying off loans.

Why is a short term loan better?

The biggest advantage of a 15-year mortgage is the interest rate is less than a 30-year loan. The difference in rates changes daily and varies with different banks, but a 15-year loan is usually about .5 percent less than a 30 year fixed mortgage. With a lower interest rate, you are paying more towards the principal and less towards interest.

Some people think the biggest advantage of 15-year loans is the shorter length of the loan. I don’t agree because you can pay a 30-year loan off early if you want too. You will have a higher interest rate, but .5 a percent is not a huge rate difference, especially when you consider how much you can make buying more properties.

Are mortgages front-loaded with interest?

A lot of people want to pay off their loans faster because they think the interest is front-loaded on a mortgage. That means you pay more interest at the start of the loan compared to the loan amount than you do at the end of the loan. The truth is you do pay more interest at the beginning of the loan, but not because the interest is front-loaded, but because the loan amount is higher. If you have a 5% interest rate on your mortgage, 5% of your payment is paid to interest. You pay less money to interest as time goes on because the loan amount decreases.

How much do you save with a lower interest rate?

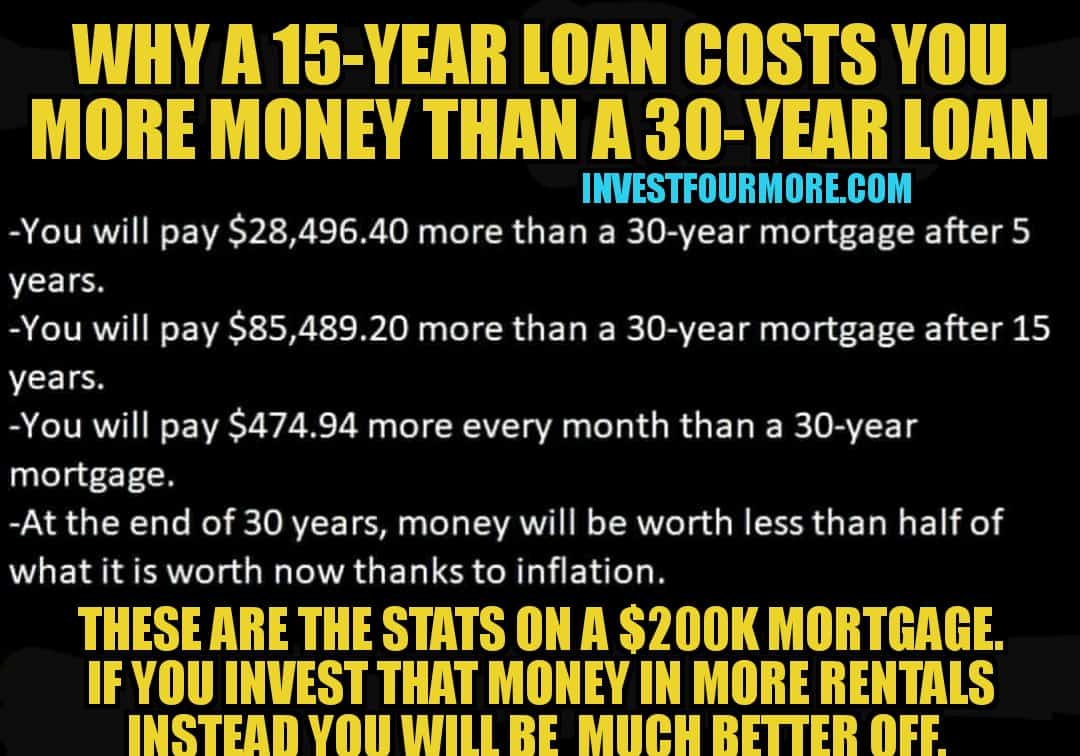

If you get a 15 year, $100,000 loan on a rental property at a 4 percent interest rate, the payments will be $740 a month (check out bank rate mortgage calculator for calculating mortgage payments). Over the 15 years of that loan, you will pay $33,143 in interest. With a 30 year loan at 4.5 percent interest, the total amount paid in interest over the life of the loan will be $82,406.

On the surface, it looks like you are saving almost $50,000 by getting a 15-year loan. However, you are paying interest over 30 years on one loan and over 15 years on the other, which is deceiving. The payment on a 30-year loan is only $507 a month, which is $233 less a month than the 15-year loan. If you were to take that $233 a month and put it back into the 30-year loan each month, the 30-year loan would cost $39,754 in interest and be paid off in less than 17 years. It definitely costs a little more to have a higher interest rate, but over 15 years that is only $550 more each year. As time goes by that money is worth less and less due to inflation.

I go over specific numbers on 15 versus 30-year loans in the video below:

Why do banks push 15-year mortgages?

You may hear banks and lenders push 15-year loans on the radio and social media all the time! I always wonder if the 15-year loan is so much better for consumers and worse for banks, why are the banks trying to convince people to get 15-year loans? There are a couple of reasons.

- The banks want people to refinance their loans because they make more money every time someone gets a new loan. You pay 2 to 5% in closing costs on a new loan and the bank or lender gets most of that money.

- Most banks do not want their money locked up for 30 years. There is a reason they offer a lower interest rate on 15-year loans because they want more people to get 15-year loans. 30 years ago interest rates were more than 10%! Now they are less than 5%. The banks know that the lower the rate is, the shorter-term loan they want. They don’t want their money tied up in long-term loans.

The banks and lenders push 15-year loans because they make more money with short-term loans.

Is a 15 or 30 year loan better?

You will pay less interest on a 15-year loan than a 30-year loan. However, you are paying a higher payment every month on the 15-year loan. If you add up the payment savings with the 30-year loan, you save $2,796 each year and $41,940 over 15 years by getting the 30-year loan.

That extra money can be used for many things that will make you much more money than that $6,000 in interest you save. You can save up the cash flow to buy more rental properties. You can use the money to build an emergency fund. You could also pay extra to the mortgage and if you ever need the extra money later, you can stop putting extra money into the mortgage.

If you have nothing to invest that money into, it might make sense to get the 15-year loan. If you want to keep buying rentals and build your empire, the best bet is to get a longer-term loan and buy as many rentals as you can now.

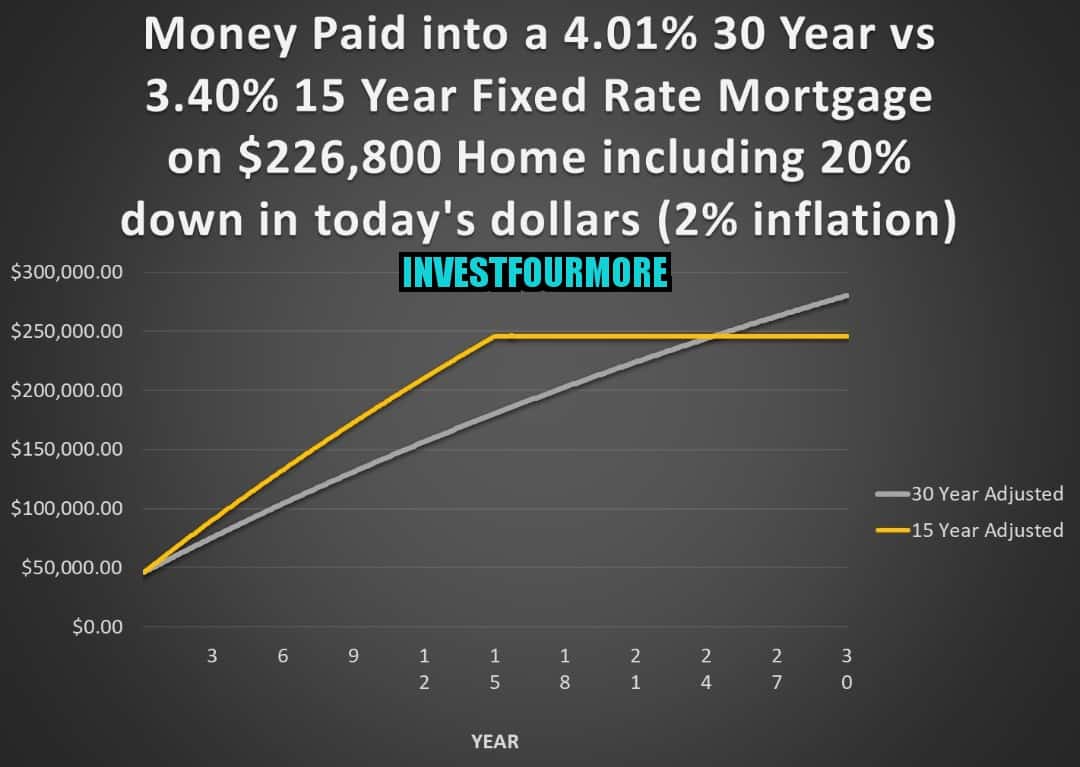

Something else to consider is that inflation makes money worth less in the future. The graph below shows how much more money a 15-year loan costs you at the beginning of the loan when inflation is considered. It takes until year 24 or longer to start saving money with the 30-year loan.

Why does a 15-year loan make it harder to buy more rentals?

Another huge factor when considering whether to use a 15 or 30-year loan, is qualifying for more properties. When banks qualify an investor, they will look at debt to income ratios. A 15-year loan will have a higher payment and increase your monthly debt payments. The higher your loan payments are, the less cash flow you will have, and it will be harder to qualify for new loans. Many banks will only count 75 percent of your rental income when qualifying an investor for a loan. Even if you are cash flowing with a 15-year loan, if you can only count 75 percent of the rental income, you may show a loss each month. If you have many rental properties showing a loss, it will be very hard to qualify for new loans.

A 30-year loan with its lower payments will make it easier to qualify for more properties.

What if you cannot get a 30-year fixed-rate mortgage?

I own 180k sqft rental properties and it is really hard for me to find fixed-rate mortgages. I use a local lender and they do not offer 30-year fixed-rate loans, only ARMs.

When I finance my rental properties, I use 30-year ARMs. An ARM is an adjustable-rate mortgage that has a fixed interest rate for a certain amount of time. The interest rate on an ARM can adjust up or down after the fixed time period is up. My portfolio lender offers 5 and 7-year ARMs with a 30-year amortization. The rate will stay the same for the 5 or 7-year term but can adjust after that term is up. There are limits on how much the rate can adjust each year and a ceiling that it can never go over. The great part about ARMs is they have a lower rate than a 30 year fixed rate loan and even the 15-year fixed-rate loan.

If you get an ARM for your rental properties you will have an even lower payment than a 30 year fixed rate loan and save money in interest costs over a 15-year fixed-rate loan. To me, it is the best of both worlds.

Why is an ARM less risky than you may think?

There are obviously some risks involved with an ARM because the rate can go up after 5 or 7 years. I always have plenty of reserves and cash flow to make sure I can afford the higher payment if the rates adjust. Even if I hold the loan well past the initial fixed-rate term, it takes a few years for the ARM to become more expensive than a fixed-rate mortgage. Chances are rents will increase in the time period as well. If you have enough cash flow and a plan for when rates could increase, you should have no problem with an ARM.

If you don’t have enough cash flow and your payments go up, you could get into trouble with an ARM. Negative cash flow is hard to sustain and it will make it harder to qualify for loans as well.

Many lenders will also only offer ARM loans after you have a certain number of mortgages in your name. I would suggest getting the fixed-rate mortgages when first starting out, and as you advance in your investing career look at the ARM option.

Why is a lower payment more important than a lower interest rate?

ARMs allow a small payment at the beginning of a loan and possibly a higher payment in the future. The nice thing about the lower payment is you have more cash flow and inflation comes into play when you are investing money. If you can pay less money now and more in the future it is a good thing, because inflation will make money worth less in the future. Even though your payment might go up on an ARM; 5 or 7 years later that money will be worth less and your rents could have gone up. If you use the money you save on an ARM to invest in more rental properties or something else with a decent return, you will be way ahead than if you had paid a higher payment with the 15 or 30-year fixed loan.

Why is a 30-year loan safer than a 15-year loan?

Many people have a tough time saving money and the higher your mortgage payment is, the harder it will be to save. Having an emergency fund is very important for financial stability. If you do not have an emergency fund, do not get a 15-year mortgage. Get the 3o-year mortgage, and save up for the emergency fund. Once the emergency fund has enough money (6 months of living expenses) you can pay off your mortgage early if you would like to.

Remember that you see no real benefit to paying off your mortgage early unless you pay off the entire loan, refinance, or sell. Your house payment will stay the same until the loan is paid off in full. If you need to access the equity you have in your house, you cannot ask the lender to give you back what you have paid early. You will have to sell the house or get a brand new loan (refinance or home equity line of credit).

If you get a 15-year loan and have a medical emergency, lose your job, or cannot work, the bank will not lower the payment for you. You have to keep paying that high mortgage payment every month. If you had a 30-year mortgage and were paying more to it every month, an emergency would not be nearly as devastating, because you could stop paying extra.

Does a 15-year or 30-year loan allow you to buy more rentals?

My goal is to buy as many rentals as I can. Not only do I want each rental to make as much money as possible, I want to buy a lot of them! The 30-year loan allows you to buy more rentals because you are making more money each month. If you take that money and reinvest it into more properties, the results are phenomenal.

My nephew, who is a math whiz, made this amazing graph. Here is how it was created:

My nephew, who is a math whiz, made this amazing graph. Here is how it was created:

- Each rental has a $120k value and $1,200 a month rent. The house was bought 30 percent below market value. but we spent $10k on repairs and 20% on down payments. We also spent 4% on closing costs to buy.

- Monthly costs are 1.5% for taxes and insurance, 8% for property management, 5% for vacancies, and 10% for maintenance.

The chart shows what happens when you buy 1 property with a 30-year loan and reinvest all the cash flow into buying more properties vs 1 property bought with a 15-year loan and reinvesting all cash flow into more properties. You buy 119 houses over 30 years with 30-year loans and 32 houses with 15-year loans. You are making $53k a month with 30-year loans vs $11k a month with 15-year loans.

This does not account for inflation! With inflation, the 30 year is even better because rents increase on more properties. You buy 147 houses vs 38. It may be tricky getting a 30-year loan on that many properties, but it shows the value of investing your money early on instead of paying off debt early.

Conclusion

On the surface, a 15-year fixed-rate mortgage may seem like the best way to go. It saves money on interest over the life of the loan and has a shorter term. I believe the 15-year loan is the worst choice because you are tying up your money, making it harder to qualify for loans, and you could be investing that money in something that gives a higher return. If you get a 30-year ARM, the interest rate will actually be lower than the 15-year loan, and you might be able to pay that loan off faster than the 15-year loan.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

Agreed. I’m looking at a $120K loan, and the difference is nearly $300/mo between the 30 yr term and 15. Even though the property should be very cash positive, an extra $3600/yr will help protect against repair cost or vacancies. I’m not counting on increased value, just the good cap rate. The cash can always be used to pay the mortgage down sooner, if not used for the next deal.

Exactly!

The timing of this post was perfect. I’ve been considering the terms of a recent purchase and was trying to decide what would be better a 15 year or 30 year mortgage. Your post helped clarify for me the advantages of the 30 year over the 15 year. On the surface 15 year seems much better, but after reading this I realize now that’s not the case.

Ben, I am glad it helped! Thank you for the comment.

We have done a 20 year ARM with a fixed rate for 5 years on our most recent deal. It seemed like a happy medium but now I’m not so sure. What do you think? How easy is it to change the terms? On our next loan I think I’ll consider the 30 year ARM as you suggested. That will make it easier to build up our emergency fund or to invest in a new fix and flip. This post really gave me some good practical tips thanks!

It is not very easy once you sign the docs to switch. You can ask your bank. I think the longer amortization the better.

As you get more and more properties, you will find that you cannot get any loans, unless you get commercial loans or get more creative.

Once you get a 5-unit or more, it’s commercial. Once you get 10+ mortgages, it’s commercial. Even anything over 4 mortgages is a bit tough to get Freddie/Fannie loans. Some banks will not do them,

That is why I suggest everyone try to find a portfolio lender! https://investfourmore.com/2013/05/12/how-to-find-a-portfolio-lender-who-will-finance-multiple-investment-properties/

Very timely article and great advice as I am working with a portfolio lender for my next rental. I went with a 30-yr. fixed rate on my first rental and am excited to go with a 5 or 7 year ARM amortized for 30 years on this next one. Wish I had known this information before! Thanks so much Mark!

Thank you Michelle! A 30 year fixed rate loan is not that bad!

Great post Mark. I never thought about using a 30 year ARM but I really like the way you think. If you have a strong cash flow then the 5 or 7 year adjustment really won’t affect you.

I would rather have the cash today.

Thank you! Most people bash ARMs, but they really are a great loan if used right.

Would this apply to people buying properties through commercial refinancing? I feel like building equity quicker (15 year) would be more ideal for my situation. It’s easier for a Canadian to buy mulitple properties in cash then refinance them after.

I think you have to look at your situation. It is easy to add principle to the payment to increase the pay down.

Hey Mark,…

Is a rental property appraised the same way as a primary resident / owner occupied home…?

The property in question has been rented for 36.4 months solid with cash flow and has room for improvement in terms of cash-flow.

Howard

Hi Howard, It depends on what type of rental it is. If it is a single family home it will be appraised for its best and highest use which is a single family home. If it is a four unit rental then it would be appraised for income as that is its best use.

In Canada, all mortgages are ARMs with a 20 or 25 year amortization. No such thing as a 15 or 30 fixed loan. the long term/ fixed loAn would be 10 years which very few people would even touch because their interest rate would be 4.5 vs 2.75 on a 5 year term.,

Mark, what you would consider to be a fairly short ARM at 5 years, Canadians would consider that as conservative long term for a mortgage. Personally though, I think that your 5 year arm with a 30 Year loan is the way to go for Canadians. Now if we could only get our average house price down below 440000$.

Wow, that makes it very tough. It’s a little surprising prices are that high with loan terms so short.

Thank you for the information. If you want to sell the property in 3-5 years and get a bigger property later, which option is better for the short term property- 15 year or 30 year?.

I think a 5 year ARM is the best option because it has rates as low as 15 with a much lower payment.

Hi Mark… I’m late to the party… maybe too late. What about when you turn your current home that has a 15 year mortgage (13.5 years left) into a rental property. Should I refinance it to the 5 year ARM or just leave it alone. Current rate on my 15 year is 2.75%

Thanks,

depends on the numbers and cash flow

Mark, do the lenders always require w2 for last 3 years to qualify for best rate mortgages?

I have three rental homes on 5Arm under commercial loan and want to get them.under residential 30yr mortgage.

Second question.. I got an email from AllStateFinancialUSA that they do finance rental propty without W2 amd base it only on rental income. Thats the first I have heard of..is this legit in case u hppen to knowiot this company…

Maybe the larger question is, is it wise to go with small name lenders vs big banks or credit unions?

Thanks Mark..love your posts!

Small lenders are much better! I have no heard of that company. https://investfourmore.com/2013/05/12/how-to-find-a-portfolio-lender-who-will-finance-multiple-investment-properties/

Deciding between a 15 and 30 yr can also vary greatly depending on your current life situation. For myself, I have a 2 year old son (2nd on the way) and my goal is to have a cash generating machine just before he hits college age. To do this I am using 15 year loans. Why? Because I don’t need the cash right now, but when its time for college tuition season… these properties will be churning out boatloads of cash as each mortgage will be paid off and rent will be straight cash (less taxes misc expenses etc).

So the choice between 30 and 15 isn’t always so clear. If you need cash now, go for 30. If you want to retire sooner, I’d go for 15 and as they are paid off your life ability to retire early because much more clear.

Additionally, you build up Equity MUCH MUCH faster with a 15 yr loan vs a 30 yr loan. So if for any reason you are forced to sell after 10 yrs, you will have built up far more equity in the 15yr loan home vs a 30 yr loan home.

totally with you on this, and with equity, allows access to Lines of Credit, giving you access to your own lower interest cash for acquisition, we use our lines to buy, then finance them after repairs, kinda like the BP “BRRR” but instead of seeking transaction funding at 10+% mine is at 4.5% and no points, and I just transfer funds no asking permission. it allows so much freedom.

For sure

much of this depends on your needs, I do my calculations on 10 year amm with a minimum of $200/mo positive, but do 3/1 commercial notes with 15 year amm. I dont need the cashflow now but want it later. I also only want about 25 properties, so that will not be a any problem for lending. we also buy with an ARV at minimum of 40% above our all in cost, those buying at retail or slightly below and take an 80% mortgage for 30 years are taking a lot of risk if the market shifts and they need to liquidate in the first 12 or so years, as the principal pay down does not really kick until about 10 years in, so that a little hope and pray that markets will go up, a little too risky in my book. all the talk on the pod casts about zero to 20% down for 30 years is great assuming outside forces dont change, and all goes well, but an awful lot can happen in 30 years.

I think you need to buy at least 20 percent below market. That builds in about 40 to 50 percent equity. Over 30 years prices will go up unless you are in a completely depressed area.

Great article. It has definitely opened my eyes on considering ARM products vs just 15 or 30 year loans.

Furthermore, you stated “Remember that you see no real benefit to paying off your mortgage early unless you pay off the entire loan, refinance, or sell.”, however, wouldn’t you be saving on interest payments if you pay off the principal quicker? Let’s say you pay $300 extra on the principal each month, that’s $3,600 a year that you’re not paying interest on or am I looking at this wrong?

You are right that you would be paying less interest, but my point was that you are still making the same payment and you don’t see that benefit of paying less interest until you sell, pay off or refi. it is only a paper advantage until that point.

half asleep, doing quick math in my head you pay 45-50% more a month with a 15 year loan. (depending whether or not you take into acount saving .5% on 15year loan.) So you maybe put 5% more of your money into equity with a 50% higher payment. Real question is whether opportunity cost are worth being forced to pay 50% more every month. I’d personally rather be able to snowball one house at a time whenever I have extra cash or put that cash into other investments. emergency funds.

All the math is in the article for how much more it costs