How to Buy a Rental Property with Little Money Down

Many people want to buy investment properties because of the fantastic returns they can provide. However, many people do not have the 20 percent down payment (or more) that most banks require. There are ways to buy an investment property with little money down. The easiest way to buy an investment property with less than 20 percent down is to buy as an owner-occupant and later rent out the house, but there are many other options for investors as well. Using a line of credit, refinancing your home, house hacking, the BRRRR method, or even credit cards can provide ways to buy investment properties for less money. Seller financing is a great way to put less money down on a rental property if you can find sellers who are willing. A more advanced technique is to use hard-money financing that you can refinance into a conventional loan. Whatever way you choose to buy a rental property, research the method to make sure that it is legal in your state, your lender approves it, and that you are not stretching your finances too thin.

How much money down do most banks require?

An investor will have to put down at least 20 percent to buy a property from a typical bank. If you own more than four properties, that figure can increase to 25 percent down, providing that they are even willing to finance more than four properties. On top of the down payment, an investor will have to pay closing costs, which can range from two to four percent of the loan amount. It is very expensive to buy an investment property using financing from a typical bank. I have found a great portfolio lender who will finance as many properties as I want with 20 percent down, but they are not easy to find. Once you factor in repairs, carrying costs, down payment, and closing costs it can cost as much as $30,000 to buy a $100,000 rental property.

The video below goes over ways to buy with little money down as well:

How to buy as an owner-occupant

The easiest way to buy an investment property with little money down is to buy as an owner-occupant, satisfy your loan requirements, rent out the property, and keep it as an investment. Most owner-occupant loans require the buyer to occupy the home for at least a year. Once that year is up, you can rent out the house and turn it into an investment property. There are many owner-occupied loans available, with down payments ranging from 0 to 5 percent down. You can put as much money down as you want if you want to put 20 percent down or even 50 percent down. USDA and VA have great no-money-down programs and little to no mortgage insurance, which will save an investor a lot of money each month. You will have more costs with little money down loans because mortgage insurance is required. Mortgage insurance can add hundreds of dollars to your house payment and eat away at your cash flow. The process of buying as an owner-occupant and then turning the house into an investment property is as follows:

1. Buy a house as an owner occupant, which will cash flow when you rent it out.

2. Move into the house and live there for at least a year.

- After the year is up, find another house that will cash flow and purchase that home as an owner-occupant.

4. Move out of the first house and keep it as a rental. Move into the new house and repeat the process every year!

Eventually, you will be building up equity and extra cash flow, which will enable you to buy properties with a 20 percent down payment. Repeating this process 10 times would be an excellent way to get started, but no one wants to move ten times in ten years. It can also be tough to convince your family to live in a home that would be a great rental.

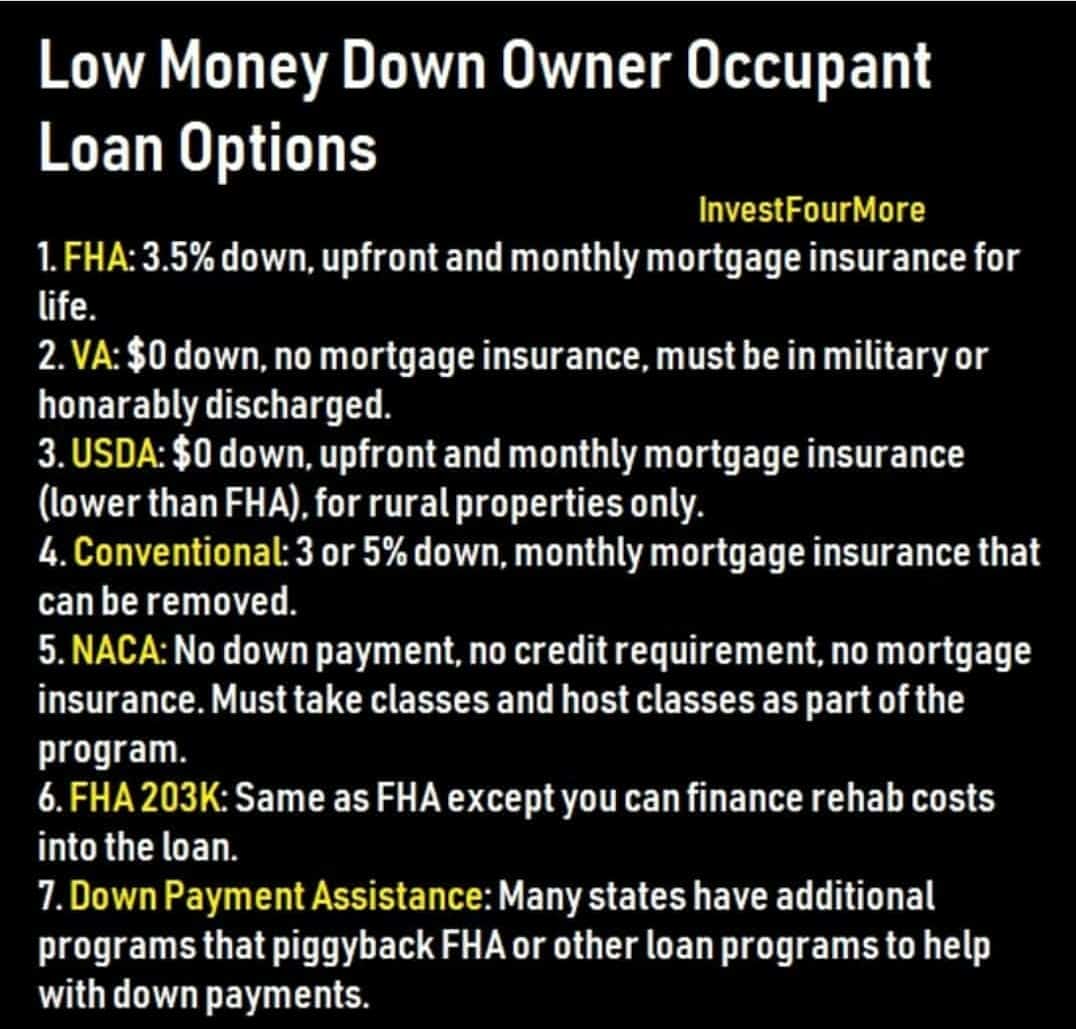

Low down payment owner occupant loans

If you are going the owner-occupant route there are many loans available that have from very little to nothing down required.

FHA loan

FHA loans are government-insured loans that can be obtained with as little as 3.5 percent down. You can only have one FHA loan at a time unless you have extenuating circumstances like a job relocation. You do have to pay mortgage insurance on FHA loans, which I will discuss later in this article. There are limits to the amount an FHA mortgage can be, which varies by state and even city.

USDA loan

USDA is a loan that can be used in rural areas and small towns. The loan can’t be used in medium-sized towns or large towns/metro areas. The loan is a fantastic loan for those that qualify and want to buy a home in the designated areas. USDA loans can be had with no money down, but do have mortgage insurance as well.

VA loans

VA loans are run through the United States Veterans Administration. You have to be a veteran to qualify for the loan, but they also can be had with no money down and no mortgage insurance! VA is a great option for those that qualify because the costs are so much less without mortgage insurance.

Down payment assistance programs

Many states have down payment assistance programs. In Colorado, we have a program called CHFA. The program helps buyers get into owner-occupied homes with very little money down. CHFA actually uses an FHA loan but allows for less than a 3.5 percent down payment. Check with lenders on your state to see if you have any programs that help with down payment assistance.

Conventional mortgages

Even conventional mortgages have low down payment loans available for owner-occupants. For owner-occupants, conventional loans have down payments as low as 3 percent. You will most certainly have to pay mortgage insurance with any conventional loan that has less than 20 percent down. Unlike some of the other loan options available, you can have as many conventional mortgages in your name as you want as an owner occupant.

FHA 203K Rehab loan

An FHA 203K rehab loan allows the borrower to finance the house they are buying and repairs they would like to complete after closing. This is a great loan for homes that need work, but the buyer has limited funds to repair a home. There are more costs associated with this loan upfront because two appraisals are needed and lenders have higher fees for 203K loans.

NACA Loans

NACA is a non-profit program with:

- No down payment

- No closing costs

- No points or fees

- No credit score consideration

- Below market 30-year and 15-year fixed-rate loans

This sounds like it is too good to be true, and it is a great program. However, you do not simply apply for the loan and hope the lender approves you. You must take classes, and even host classes when in the loan program.

More details are on the NACA site.

What loan costs does a buyer need to consider besides the down payment?

On almost any loan you will have more costs than just the down payment. The lender will charge an origination fee, appraisal fee, prepaid interest, prepaid insurance and possibly prepaid mortgage insurance. Plus you may have more costs the title company charges like a closing fee, recording fees, and possibly title insurance. In most cases, the seller pays for title insurance, but with HUD and VA foreclosures the buyer has to pay for title insurance. These costs can add up to another 3.5 percent of the mortgage amount or sometimes more. When you talk to a lender they can give you an estimate of exactly how much these costs will be before you get your loan.

Can you ask the seller to pay closing costs?

Even though the lenders and title company will charge you more fees than just the down payment, that does not mean you have to pay that upfront. You can ask the seller to pay closing costs for you. If you can get the seller to pay your closing costs for you, loans like VA and USDA may be obtained with no out-of-pocket cash. You may still have to put down an earnest money deposit, but that can be refunded at closing in some cases. When you ask the seller to pay closing costs, it reduces the amount of money they are getting from the sale so you might actually be paying more for the home than if you didn’t ask for closing costs. But in my mind paying a little more for the house and financing those costs to save cash is better than paying more money out-of-pocket for a little cheaper home.

House Hacking

House hacking is when you buy as an owner-occupant but you buy a multifamily property instead of a house. By purchasing a multifamily property you can live in one unit while you rent out the other units. This strategy allows you to rent the property faster, which may mean the bank will be more willing to give you a new loan as soon as you are ready to move out. You will also have help from the other tenants to pay your mortgage. In some cases, you may be able to live for free while you own the house because the other rent covers your costs.

Virtual real estate

Yes, you can now buy virtual real estate! This is land in the metaverse that only exists digitally. Some pieces of virtual real estate have sold for millions of dollars and others can be bought for almost nothing. Here is some more information on getting started!

BRRRR Method

BRRRR stands for buy, repair, rent, refinance, and repeat. It is a great way to get into rentals with less money down. You will need to get an awesome deal to make this strategy work, but you may be able to get all of your money back. You buy a house that is an amazing deal, fix it up, rent the property, and then refinance it. Once the refinance is done you repeat over and over! The key to making this strategy work is getting an awesome deal with plenty of equity. You also need to be prepared if things do not go perfectly. Appraisals can come in low, the banks may not want to finance you, you may not get the property rented or repaired as fast as hoped, etc.

Hard money loans

Using hard money can save you a ton of cash in the short-term, but it is more expensive in the end. Fannie Mae lending guidelines, allow you to refinance a home with no seasoning period, which means you do not have to wait six months or a year after you purchase a home, to refinance at a higher value than what you bought it for. Fannie Mae guidelines base the refinance amount on a new appraisal, and they will allow a 75 percent loan-to-value ratio. Fannie Mae guidelines do not allow a cash-out refinance, but they do allow the refinance to pay off any existing loans. Many hard money lenders will allow a buyer to borrow up to 100 percent of the purchase price and to finance repairs as well.

Since Fannie Mae guidelines allow a 75 percent loan-to-value refinance, theoretically an investor could buy a home for $100,000 and get a loan with a hard money lender for $100,000 plus $30,000 in repairs for a total loan amount of $130,000. The investor could refinance the home for as much as 75 percent of a new appraisal. If the appraisal came in at $180,000, then 75 percent loan-to-value would allow a refinance of $135,000. Fannie will not allow a cash-out refinance, but the investor could refinance the full $130,000 loan amount. This strategy can be costly due to hard money fees, but it allows the investor to refinance the entire purchase price and repairs!

This strategy can also be very risky because you are depending on a high appraisal to get your money out. Most hard money loans are only one year and you must pay off the loan after that year. Refinance appraisals are not always as high as we would like them to be. Make sure you have an exit strategy if the appraisal comes in lower than you expect.

Private money loans

One legitimate way to buy real estate with no money down is to use private money. Private money is from a private investor, friend, or family member. The private investor will give you money at a certain interest rate to buy a flip or rental property. Private money rates can vary from very cheap to very expensive depending on the relationship, investment, and terms of the loan. I use private money from my sister for my fix and flips. She charges me six percent interest. It is a great way to reduce the amount of cash I have into the properties.

I have used private money to buy commercial rentals and then refinance into a long-term loan with a local bank.

Can being a real estate agent help?

There are many advantages to having your real estate license, but the biggest benefit is you can keep your commission on almost every house you buy. On a $100,000 house, your commission could be $3,000 dollars or more. Here is an article that details why it is an advantage to become a real estate agent if you are an investor. Being a real estate agent also gives me an advantage in finding and purchasing great deals. I detail how hard it is to get your real estate license here. I saved more than $270,000 a year on commissions by being a real estate agent. That does not include the money I made on deals that I got because I was an agent.

Turnkey rentals

A new trend in the US is buying turnkey rental properties that are purchased, repaired, rented, and managed by a turnkey provider. Turnkey properties are a great opportunity for investors to buy rental properties out-of-state when homes are too expensive in their area. There are turnkey providers who offer as little as 5 percent down for investors, but they tend to have very high-interest rates. Here is a great article about turnkey providers or send me a request here for turnkey providers I know of. I bought a turnkey rental in Cleveland a few years ago.

Line of credit

I have had many lines of credit in my career. I have had lines of credit against my personal house (the house I live in) and my investment properties. It is much easier to get a line of credit against your personal house and some banks will not even offer lines of credit on investment properties. A line of credit is basically a loan against a home, but you do not have to use the money all the time. If you do not need the money you can pay it back to the bank and not be charged interest on it. When you need the money again, you can borrow it very quickly as long as the line is open.

Off-market properties

Off-market properties are purchased through direct marketing or by word of mouth. Buying off-market usually means less expensive properties and in some cases, owners with flexible terms such as owner financing. Many investors wholesale off-market properties, which you can purchase with no down payment. Wholesaling is a process of buying and selling properties very quickly. The properties must be very good deals and are usually found by direct marketing for properties. Many investors make a great living by only wholesaling properties to other investors.

Seller financing

Some sellers may be willing to finance the house they are selling or finance a second loan on a home that allows a buyer to put less than 20 percent down. If your bank is willing to offer 80 percent loan-to-value, the seller may offer to loan the other 20 percent, which would amount to no money down for the buyer. The seller may also offer a number of other loan-to-value percentages to help a buyer get into a home for less than 20 percent down.

Finding seller-financed properties is the tricky part. Most sellers are not looking to finance a loan when they sell. To find seller financed listings, look for homes that have no loans against them or an MLS listing description that say seller financing is available. The seller’s terms can vary greatly depending on how desperate they are to sell and what exactly they are looking to get out of the deal. Do not expect to pay four percent interest on a seller-financed loan; they will want a premium on any money they lend. It is also harder to find great deals with seller financing, which is key to my strategy.

There are many new restrictions on financing thanks to the recent Dodd-Frank Act.

Refinance

In most areas of the country, home values are rising and interest rates are at record lows. You may be able to refinance your home and get enough money to buy an investment property. Once you are able to buy an investment property, you can refinance it in one year (sometimes less with the right bank). With rates as low as they are, if you bought the home below market value, you should be able to take out as much as you put into the house and still cash flow. I use this refinance technique all the time. Getting lenders to do a refinance is tricky when you own multiple investment properties. I use a portfolio lender who has allowed me to use a cash-out refinance on as many properties as I want.

Below is a property I refinanced:

Move in ready Houses

A move-in ready property means all the repairs are completed and it is ready to rent as soon as you buy the home. There can be many advantages to buying a nice home. The biggest advantage is you do not have to pay for repairs. You also do not have to spend time waiting for repairs to be done, which saves money on mortgage payments, utilities, and other carrying costs. The downside of a move-in ready property is that it is usually more expensive and provides less cash flow than a home that needs work.

Credit cards

A few other ways to get quick cash can be very expensive and are usually reserved for people looking to do a quick flip. If you have a killer deal you cannot pass up, you may want to consider these options, but I do not recommend using them unless it is necessary. The easiest way to get quick cash is with credit cards. You can get a cash advance or pay for repairs using your credit card. If you use a credit card to finance your down payment or repairs and cannot pay it off right away, do not pay the 17 percent interest rate. Do your best to get another card that will allow a balance transfer. Many times, you can transfer all of your balance and pay little to no interest for up to a year. That may give you enough time to pay off the card and not to be stuck with a high-interest rate eating all of your profits. I also suggest using a rewards card for repairs on your investment properties. If you pay the balance off every month, this is a great way to make a little extra money.

Self-directed IRA

If you have money invested in an IRA, you are not limited to investing in stocks or mutual funds. There are special self-directed IRAs that you can use to purchase an investment property. You can use your IRA for down payments and repairs and then collect rent in the IRA.

401K

Some 401ks allow an investor to take out a loan against them. You usually have to pay back the loan relatively quickly and pay interest on the loan. You have to be very careful when borrowing from a 401k because the money you borrow is no longer earning interest or growing in your retirement fund. If you lose your job, you also may be required to pay back the loan within 60 days or pay a 10 percent penalty and income tax on the loan.

Subject to loans

With a subject to loan, you buy a house without paying off the previous owner’s mortgage. This is another tricky situation; investors must be very careful with it. Most bank mortgages are not assumable; when the homeowner sells the house, they have to pay the loan in full. The bank most likely will have a due-on-sale clause that says the loans must be paid in full, once the property transfers ownership. With subject to loans the new investor buys a house subject to an old mortgage and does not pay off the loan. There is a chance that the bank will require the loan to be paid off if they find out that the home has been sold.

Investors buy homes subject to a mortgage so that they do not have to get a new loan. It may be hard for the investor to qualify for a mortgage or they may be maxed out on being able to get new loans. If you buy a home for $80,000 that has a $75,000 mortgage in place, the investor would only need $5,000 to buy the house instead of the normal 20 percent or more.

Fannie Mae Homepath program

The Fannie Mae Homepath program on their REO properties allows investors to put only 10 percent down and allows up to 20 financed loans in one person’s name, which is also a huge bonus. It is very difficult for many investors to get loans on more than four properties.

This program has been discontinued.

Conclusion

Rental properties can be expensive, but there are ways to purchase them with less than 20 percent down. If you are short on cash, buying properties with little money down can accelerate the purchasing schedule and increase your returns. However, you will most likely make less money on each property, because borrowing that last 20 percent can be much more expensive than the first 80 percent.

My book Build a Rental Property Empire, goes over how to buy investment properties with little money down. It also covers how to find deals, finance rentals, manage them, and much more! It is available as a paperback and ebook on Amazon or as an audiobook on Audible.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

You didn’t address IRA’s and 401’ks

Lease for Rental to yourself, re-invest all monies back into Ira’s upon sale of house deposit any & all gains to Ira Then there is NO! Taxes on your Capital Gain’s, then repeat process over and over!

Thank you for the comment Miki,

I think the IRA and 401k route deserve their own article. I’m not a huge fan of retirement plans because you have to wait so long to touch the money. But, I think that is a great strategy for those who already have a lot of money in retirement accounts.

I’m planning on using my IRA and withdrawing up to $10,000 to buy my first duplex. I don’t own a home yet so I shouldn’t be penalized for it.

441586 702577Excellent post man, maintain the good function, just shared this with my friendz 229389

There are certain ways to purchase an investment property with low start up financials such as seller financing. You can also save money by converting your house into a rental property which is one of the quickest methods.

Hi Mark,

Recently I found your blog and inspiring because I just bought a duplex and am thinking of investing more properties as well:)

When you keep purchasing homes as owner occupant as you mention above, do you have to use different lender each time you purchase one? Or you purchase the second and more homes as investment property? I wonder that the same lender could give you finance on multiple homes as owner occupant.

Thank you for the comment! You should be able to use the same lender. When I talk about this strategy, you should always stay within the rules, which means you have to occupy the home for at least a year. You can only have one FHA loan as an owner occupant, but you can have multiple owner occupant conventional loans. As long as you lived there for a year, the same lender will most likely give you another owner occupant loan.

Always enjoy reading your good article. I m in the process of looking into way to financing for my first true or says 2nd rental investment. I bought my first home with intention to rent it out completely after I live in it for a year and move on to the next one, currently live in it and rented out half of it. Talked to a couple lenders, financing second home is a little stricter, even if you plan on live in it. Do you run into this? what’s your experience and any suggestions. I mean harder as qualifying for 2 mortgages. Was told that you can’t use your current rent (house that you live in) or potential rental income to qualify unless it is on 2years tax return. I know the DTI for investment is 45%, is that number run across the board for 2nd home owner occupy as well? I do have some good equity for the first home but don’t want to use it just yet, as it will also count against my overall DTI. Thanks in Advance.

This can be an issue with conventional lenders. MY portfolio lender counts my potential rents, at least 75% of them. I would try to find portfolio lender.

Very informative article. Thank you for sharing

Thank you Brian!

I am looking at a property that has two quad plexes on it. I am wondering if I can buy the property and qualify as owner occupant if I live in one of the units.

Hi Stacy, see my comment in the purchase 100 properties thread

check out http://www.wholesa….. . Can you let me know if this would be a good start?

I have no idea Jim, You could probably learn more from bigger pockets, but without buying the course who knows how good it is

THIS IS ALL TOO CONFUSING? LOVE THE IDEA OF THIS GAME? BUT I REALLY DONT UNDRSTAND HOW YOU CAN JUST BUY A HOME WITHOUT CASH OR CREDIT? I MEAN MONEY TALKS, HOW WOULD ANY 1 TAKE YOU SERIOUSLY? AND THEY ARE ALWAES WANTING AND UPFRONT DEPOSIT AND WEEKLY PAYMENTS?

Hi Frank, no one said no cash or no credit. But there are ways to buy with less than 20% down.

I’m only 23 and I have nobody to help me that is relatively close. But when I buy a property, however I do that, I will have help fixing it up from my father. No financial help though I will have to do whatever I can by whatever means necessary to myself. I was hoping to buy something that would provide housing for around 5 families but something that needed work so I could purchase it right because I didn’t want to be too deep in my first property. What do you think my best strategy would be since this will be my first ever property purchase and since I will be doing it on my own? Should I search for an investor and maybe flip the first couple properties to gain some capital to then purchase a property outright and take a loan against a that to purchase what would be my second property in my portfolio. Do you suggest tax sales? I have heard a lot about them. Not too sure just fishing for ideas so I don’t make a costly mistake on my first property.

Thanks

Nate

Hi Nate, have you thought about buying as an owner occupant and then renting out the other units? you could try finding an investor to flip with, but it will bot be easy. What will you have to offer that investor?

Most banks will require investors to put at least 20 percent down when they buy an investment property. However, there are many ways you can buy investment properties with a much smaller down payment.

Probably the most common type of “no-money-down” purchase is when investors use credit lines (their own or from a group of lenders acking them) to cover the entire purchase price of a property. This is what buyers at foreclosure auctions often do. They use the credit lines to come up with the cash to buy the property.

There is also something called a purchase money mortgage (PMM), where the seller lends you money. In this case, the bank might lend you 80% and the seller 20%.

f you’re buying property for your own home, there are government-backed programs that allow up to 100% “loan to value” (LTV). The Department f Housing and Urban Development (HUD), for instance, has the FHA loan program.

In all the above cases, you can use these special loans to buy residential properties of up to four units.

Not sure how you can describe putting a down payment of 100% of the purchase price as “no money down”. It sounds more like putting the “most money down.”

Fannie Mae Homepath program has been discontinued 🙁

I currently own a $140,000 home through a zero down USDA loan in TX. I’d like to rent it out and buy a home under 100k, live in it for a year, repeat that process once, then buy a home around 200k to live in long term. I spoke to a loan officer who told me that my idea wouldn’t work and I’d have to buy a home of equal or greater value to my current home. Is that accurate? Thank you.

I have no idea why you would need to buy a home for equal value to your current home.

1031 maybe, and he’s a little confused on how it works?

NM, he’s trying to keep the current home, not sell it….my bad.

Thanks for the valuable information, I have learned so many things from this post.

Hi Mark,

Very helpful article. Seller financing is a good idea,however,it doesn’t work in Los Angeles and Orange County area. The market is hot, therefore, most sellers are not willing to do that. 20% down is a lot of money when buying an investment property with average price 400k to 500k. That’s why you got to have some cash to invest in real estate in California. Little money or no money down strategy doesn’t apply in the local market.

It doesn’t work in most markets, but you may get lucky. You can still buy as an owner occupant in Cali and live there for a year.

I want to buy property but I don’t have the best credit. I would be a first time home owner. I really don’t know where to start. Please help!

Why is your credit bad and how long will it take to fix it?

Hello, I have been reading your articles and would like your opinion on our situation. We bought our first home when the market was low, 3 years ago. We paid $65,000 for it as a HUD home. The home was almost completely renovated in 2007 (not permitted, but done well). It had a new roof, central AC/heat, new sheetrock, nice details like rounded edges on all corners, new crown and base moldings in every room, and new vinyl windows all done in 2007. We laid laminate planks throughout the entire home, repainted all rooms, repainted the kitchen cabinets & put in all stainless steel appliances ($1,200 craigslist etc.), also updated bathroom. Our home is probably worth about $140,000 now, because we bought it so under value & updated it (according to Zillow & my own review of the market). …sorry, maybe TMI. Anyway, would it be better to save a down payment for another home and keep this as a rental, or sell it to have approx. $75,000 to reinvest in 1 or 2 other properties? We owe approx. $55,000 still. It seems like it has way to nice of upgrades that would be wasted on a rental, but one doesn’t come across a $55,000 mortgage often either. One other side note, it is not connected to sewer. Because of the location, if the septic fails we will be forced to connect with a price tag of $20,000. -Thanks

I would think about selling depending on what you can buy now and if it will cash flow. The nice thing about your situation is you shouldn’t have to pay taxes on the profit.

Okay. To buy a 800-1,500 sq ft reasonable fixer we’re looking at about $70,000-$100,000 each. Would you recommend a home with multi units and income potential that has half the top floor burned (4,500 sq ft home & $40,000 price & good location). Or would you not recommend homes with burn/water damage that extensive even with savings? Thanks

I would be very careful with any burned homes unless you have experience with it. There are huge risks involved. Many times the entire house has to be demoed because of smoke damage, the smell never goes away.

Hello,

I would like to purchase the condo I currently reside in and am interested in a “Owner Occupant” purchase as I have little money for a down payment. I have resided in this condo for the past year and a half. My question, can this time be considered as my “time occupied”. Is there flexibility with this? Im guessing no but I thought Id ask.

Also, the landlord of the condo recently listed it for sell in hopes of selling it by January when my lease ends. Is there an advantage in selling to your tenant? If so, I would like to ask him to wait for me 6 months, in which time I will be fully ready to make the purchase. Meanwhile, of course, I would continue to reside in his property paying him rent. Does this sound reasonable?

He purchased this property in the 90’s for around 90,000 and it has since increased to around 290,000. It is priced just below market value, it is in great condition, in a great location and I see reasonable potential to make this my first purchase.

I still have lengthy research to make which is why i want to wait 6 months.

I am young (early 20’s) and have a lot of research to do, but I am ambitious and want to learn all I can to possibly make this my first investment property.

Thank you,

Monica

You would have to live there for a year after buying it.

If I was a landlord I do not see any benefits to waiting to sell it to you versus someone else. He may be ready to sell right now and may not want to wait. You can always ask and see what he says.

Hi Mark,

I have a home that i owe 178,000 on I am trying to stay another few years until my son is out of school. At that time I want to know what would be the best option . The loan is in my ex husbands name but the home was goven to me by the court. With that said it looks like I do not have a house payment or have ever owned a home . Do I sell this own and put the money down on a duplex and then rent out both sides or do I live in one side of the duplex. I am trying to make the most money to put toward retirement for the future

First off If there is a loan against the home you would have to pay it off when you sell the house, it doesn’t matter whose name the loan is in. As far as the other scenario that depends on the numbers and the deal you find.

Hi Mark,

We are considering buying a second home, rent out the current one and move to the one we are buying. However, the one we are liking so far is closer to our work but far from our children’s school. They are in high school and the older one just started driving. So we won’t want them to drive far. We also don’t want to wait longer to buy since the house prices and interest rates are going up. We can’t afford a huge downpayment either so we want to live there (required if rental property). So can we buy as rental but not really live there yet, but rather rent it out, since we cannot afford 2 mortgages? And then after a couple of years when our kids are done with high school, move in to that house?

You have to live in most owner occupied homes for one year and usually you have to move in within 90 days of purchasing depending on the loan.

Hi Mark,

I am considering buying a duplex that is already rented out and doesn’t need repairs. What is a good offer to make? 5x what it brings in annually?

That depends on many, many factors. Rents, expenses, market value etc

Mark,

I am considering a vacation/rental in Florida. Prices of those I’m looking at are 500-775,000. Good GRI on all of them (50,000 – 80,000). It will be a challenge to put 20% down, although I have it, a little hesitant to put it all in one basket. I own 3 homes, one of which I live in and one I rent. The other my son lives in (basically no rent). Your suggestions are good, but I’m wondering if 20% on a turn key property is typically required – its fully furnished, booked through 2016 season,(not offered by turn key company, just through regular realtor).

Just remember the returns on vacation rentals are hampered greatly by the expenses. https://investfourmore.com/2015/03/can-you-make-money-with-vacation-rentals/

I own 2 rental properties out right that both have tenants. My credit isn’t that great, but I only have around $5,000 in debt total. I would like to borrow money to do repairs to each property as well as buy another investment property. Would it be better to use a hard money lender or could I get an equity loan?

I would get an equity loan if you could. The hard money will only be good for a year

I am a Loan Officer with 16 years’ experience at a mortgage company in Maine. If you own a home, and wish to purchase another home as your primary residence (and rent your current home), you will experience difficulty getting conventional or government financing if the property you are trying to purchase has more units or is inferior to your current home. This is up to the underwriter’s discretion. If they feel you are simply trying to “work” the system and purchase an investment property utilizing the better terms of an owner occupied loan program, they will either deny the loan or insist that it be underwritten as an investment property. I’ve been down this road several times with clients. Be prepared to provide a detailed letter of explanation to the underwriter and it had better make sense.

Hi Richard, I have heard this a couple times. I am always baffled since the HUD guidelines say the owners have to live there one year. It seems weird that HUD would give guidelines for what they require an owner occupant to do, but then turn around and say people are working the system when people follow those guidelines.

Great article mark. Would prefer to get more detailed in each strategy especially for foreign national investors.

Each strategy has more information on it if you follow the links. I also have some programs for investors as well. https://investfourmore.com/blueprint-for-successful-real-estate-investing-2016/

What if you live from paycheck to paycheck & have nothing saved. Plus working on clearing up bad debit. Can someone like me still profit from this? If so, what should I do?

I would concentrate on bad debt first

Mark, I have a question that nobody has really answered for me. If I bought a home for sale are there any difficult laws or taxes that you have to go through to turn it into a rental property? Or can I buy a home then immediately post it up as a rental home on real estate websites, without it being illegal as I don’t have some kind of ‘okay’ to rent that specific property out to tenants? Thanks.

Depends on where you live, some cities require you to register rentals and others require nothing.

Dear Mark,

It has been an year since I am working as an architect. I have a small saving and a basic salary. You know architects initially earn very less. But, I am keen on starting investing in real estate. Can you suggest something. Should I invest in real Estate Bonds?

Since I am an architect, do you think I can take some advantages from my profession?

Thank you for this article.

I don’t know anything about real estate bonds

this is really awsome thanks for sharing such a informative artical

You are welcome!

We are in California. Someone mentioned that a realtor would need to put more money down when purchasing a property. True or false?

I have never heard of that

I’ve read that USDA loans are only for primary residences. Can you get one for investment properties? What is a good lender to use for them? I live in California but I’m looking at property in Kansas. Thanks

Correct, you cannot use a USDA loan on an investment property.

Hi mark, quick question. Besides from actually residing in the home , what actual “proof” would you have to show to validate that the home your purchasing is an owner occupant?

Well, if you are getting an owner occupant loan, you should be living in the home