The ABCs of Real Estate Investing

I believe that real estate is one of the best investments to gain wealth and security. However, many people feel it is risky and does not produce great returns. They never get into the ABCs of real estate investing because they get scared away. I think many of those risks are overstated and many of the advantages of real estate are glossed over when people downplay real estate as an investment. Real estate is a great investment not just because it can appreciate but also because it provides cash flow, tax advantages, and the ability to gain instant equity due to real estate being an imperfect market.

The ABCs of real estate investing

The first thing we must talk about is what is a good investment property or type of investment. When discussing the ABCs of real estate we are looking at a very high-level view. House flipping, wholesaling, and note buying are all often lumped together as real estate investing. I think that true real estate investing is owning rental properties. I flip houses and love it, but it is more of a job that can be turned into a business than it is an investment, like how wholesaling and notes are like being a banker. Rental properties are an investment because they make you money month after month, year after year, with little work if you have property management in place. This article is all about rentals, although some may consider the other techniques real estate investing as well.

The video below goes over why most people never invest in real estate.

Leverage

One of the greatest advantages of rental properties is they are easy to leverage, which means finance. Most banks will require at least 20% down when you finance a rental property, but it is possible to buy rentals with less money down. You can buy as an owner occupant then turn the property into a rental later on, or you can house hack or use the BRRR method.

When you use leverage to buy a rental, you are able to buy an expensive asset with less money than the asset costs. If you buy a $100,000 house with a $20,000 down payment (there will be more costs), a 5% increase in value does not equal a 5% increase in your investment. It equals a 25% increase in your investment because you only invested $20,000…not $100,000.

It is true that real estate does not always outperform the stock market when you compare the average increase of the stock market to the average increase of the housing market. That assumes you pay cash for rentals and are not financing them. It is also much harder to leverage stocks, and you can leverage a much smaller percentage of the investment.

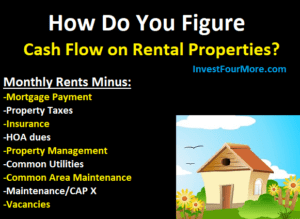

Cash Flow

Another great advantage to rentals properties is cash flow or the income you make every month after paying all expenses. Even when you have a mortgage, a good rental property will produce cash flow every month. On the residential rental properties I bought, I would make from $400 to $500 per month in cash flow after paying for property taxes, insurance, mortgage payment, property management, maintenance, and vacancies. Many people will forget to include maintenance and vacancy costs because you do not have them every month, but they will come into play eventually and need to be accounted for.

I am looking to make at least a 15% cash-on-cash return on the rentals I buy. That means I get a 15%t cash return (cash flow) on the money I have invested into the property. It is not easy to find properties with these types of returns, and other people may be happier with much smaller returns, but rental properties can make a ton of money.

Cash flow can also make it much easier to retire early as opposed to other investments. That cash flow will come in every month for the rest of your life as long as you own the property. The cash flow will increase when rents increase and as loans are paid off. Rentals are a natural hedge against inflation because the returns increase as rents increase with inflation. The cash flow is relatively steady, which means it is easier to know how much money you will have in retirement instead of having to guess when you will die and if you will run out of money.

Buying below market value

Another awesome thing about real estate is you can buy it below market value. When you buy a stock, everyone knows what the price is. A stock has a price you can buy it for or sell it for. That value may increase or decrease over time, but you know what it is worth right now. You can buy a house for less than it is worth due to many factors. Every piece of real estate is different, and that makes it hard to value. Every house is in better or worse shape than the next, bigger or smaller, and in a different location. That makes real estate hard to value. Sellers also have different motivation, and there are different ways to sell houses. Some people list with an agent or sell the house themselves, or they may not even be trying to sell but are willing to if the right person comes along.

I completed 26 flips last year, and I bought every house well below market value. You do not have to be a professional house flipper to buy houses below market value. I bought most of my houses from the MLS (multiple listing service), where anyone can buy. It is possible to buy a house that is worth $200,000 for $180,000, $160,000, or even less. Sometimes, the houses need a lot of work, and sometimes they don’t. Houses can be priced low because the seller needs to sell fast because there are tenants in the house, because the real estate agent priced the house wrong, or because it needs work.

Buying real estate below market value is a huge advantage over other investments. Many people use the BRRR strategy to buy with none of their own money because they buy below market value. BRRR stands for: buy, repair, rent, refinance. An investor buys the house below market value, fixes up the house, gets it rented out, and then refinances it. You can usually refinance a house for 75% of the market value so the investor has to get a great deal to get all the money back from purchasing the house and refinancing it.

Tax advantages

Rental properties also have amazing tax advantages compared to other investments. You can make money with a rental property every month but show a loss on your taxes. And, it is legal! The reason you can show a loss is you can depreciate rentals. The IRS makes you depreciate the structure of the rental over 27.5 years on residential rentals. That means you deduct part of the value of the structure every year on your taxes. When you sell the rental, you may have to pay taxes on that depreciation you recapture, but the pay back tax rate is most likely lower than the tax rate you pay now. You can also use a 1031 exchange to avoid the recapture or paying capitals gains taxes.

When you sell a rental property, you have to pay capital gains taxes on the profit unless you do a 1031 exchange. However, the long-term capital gains tax rate is usually lower than the normal tax rate you would pay for earned income. You can also depreciate or deduct most expenses on a rental including the interest you pay on the mortgage. If your rental properties are in a corporate structure, you may even be able to take advantage of the new tax laws to save even more money!

Always talk to an accountant for specific advice on rentals or information on the exact tax laws.

Appreciation and loan pay down

Most investors who are not familiar with rentals will mention appreciation as the main return you get with real estate. Appreciation is the increase in value of a property simply based on the market values increasing. Appreciation is a nice bonus, but most investors are more concerned with cash flow and the other advantages as they cannot control appreciation.

As we mentioned before, the increase in value of a property is not the return on your money when you use loans. If someone tells you houses only increased 5% per year and that is why housing is such a bad investment, they are forgetting that most investors don’t pay cash, and they make much more than that just from appreciation.

When you get a mortgage, you are also paying down the principal of the loan slowly over time. On a $100,000 loan with a 30-year term and 4.5% interest rate loan, you pay $131.69 towards principal and $375 towards interest the first month. The portion of the payment that goes towards principal increases over time, and the portion that goes towards interest decreases over time. The higher the loan amount is the more you pay off. I have a commercial rental that I bought for $2.1 million, and we took out a $1,575,000 loan on it. We paid off more than $50,000 of that loan in the first year making minimum payments.

Conclusion

As you can see, there are many advantages to rental properties and investing in real estate. I am not the typical real estate investor, but I routinely buy properties at least 20% below market value (after accounting for any repairs needed), make 15% cash-on-cash return on the money I have invested, and pay down thousands of dollars in loans every month. I am also in Colorado and have gotten lucky with incredible price appreciation, which to me is a bonus.

The catch with real estate investing is that it is not easy! It is tough to find these deals, tough to finance them, tough to repair them, and tough to manage them. If you are willing to put a little work in, real estate can be an amazing investment.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.