Is It Better to Invest in Real Estate or Stocks?

I have invested in both real estate and the stock market, and I believe real estate is hands down the better investment. Even with the stock market increasing significantly, I am making more money on my rental properties, and they allow me to retire much earlier than the stock market would. The conventional thoughts are that if we invest enough money for a long enough time in the stock market, we should have enough money to retire without much risk. The problem is how long it takes to invest and how much money you have to invest in the stock market to be able to retire. With real estate, you can retire by investing much less money over a much shorter time if you do your homework and spend the time needed to choose great properties. Leverage and the ability to buy real estate below market value are a couple of the many advantages real estate has over stocks. In the end, investing in real estate or stocks is a great practice either way, but real estate will always be much more lucrative in my books.

Investing in real estate or stocks

In this comparison, I use rental properties and the traditional way of investing in stocks. Most people who invest in stocks buy mutual funds or individual stocks with a retirement account. To be honest, it takes more work to buy great rental properties than it does to invest in the stock market. However, there are other ways to get higher returns in the stock market like trading options or buying on margin. These can be extremely risky strategies that take a lot of time to master. Investing in rental properties can take much less time and involve much less risk than trading on margin or training options. You could invest in real estate with more active methods like flipping or wholesaling and make more income.

I decided to compare rentals to the traditional way of investing in the stock market because that is the choice many people find themselves considering.

How long does it take to retire with stocks?

Traditional investment models encourage us to invest in the stock market because, over time, the stock market always goes up. I was taught this in college, and I invested in the stock market before I became frustrated because it took so long to make my money grow. When I plugged my current level of investing in retirement calculators, I was shocked at how much and how long I would have to invest before I could retire with the stock market.

For example, if I start with $5,000 and invest $10,000 every year for the next ten years, it would grow to $148,000 if the stock market goes up 7% a year. After 20 years of investing, things get better and I end up with $429,000.

Is 7% the right return to use for the stock market? That is tricky because there are different ways to judge the market. Depending on how far back you go, if you use the stock market, S & P, or some other metric, you will get different returns. The returns have been greater during the last ten years, but we have been on one of the greatest runs in history. The market could always go down as well.

If we use 10% as the return for stocks, my investment turns into $176,000 after ten years or $606,000 after 20 years. That is not enough money for me to retire! Either I have to invest much more money into the stock market or I have to wait longer, or make a much higher return. If I invest for 30 years at 10%, I will have more than 1.7 million dollars! That is great except inflation will make that money worth less than half of what it is now.

A calculator like this can allow you to play around with the numbers.

The kicker was I had to guess when I would die with the retirement calculators to see how much I needed to invest. I also had to guess what return on my investment I would get. Hopefully, I do not live too long or underestimate the return on my investment or I would run out of money in retirement. I knew there had to be a better way to invest than to play a guessing game with my future.

The video below goes over stocks vs real estate as well:

Do rental properties offer a better return?

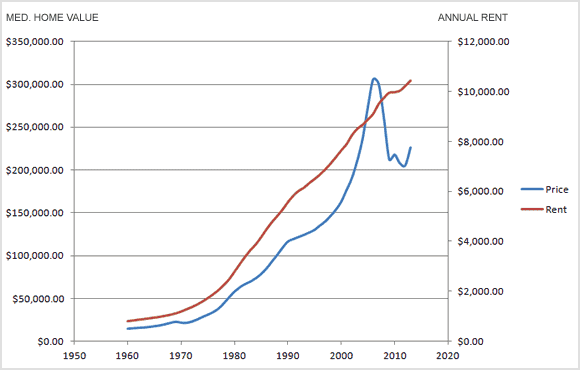

The historical increase in housing prices since 1900 is only 3.1 percent a year. Looking at those figures (which is all many stock market proponents do) makes it seem like the stock market blows real estate out of the water. However, real estate investing is completely different from buying a house and hoping it goes up in value.

- Real estate investors should be investing for cash flow, not appreciation. Only counting the housing price increase is like saying stock market investors cannot count any dividends they made on their stocks.

- Real estate investors tend to use leverage or loans to buy rental properties. The overall housing market increase does not take into account using any leverage. It assumes an investor buys a house with all cash.

- Even if an investor buys a house with all cash, they will still make money from the rent they receive. The only situation I can think of that would meet these scenarios is an investor who buys land, never rents it to anyone, and holds on to it assuming it will go up in value. However, most investors still make some income from land whether it is a CRP, mineral rights or farming.

- Real estate investments can be depreciated and stock market investments cannot. The tax savings from depreciation can equal thousands of dollars a year, blowing that 3.1 percent out of the water on its own.

- You can buy real estate below market value; you can’t do that with the stock market.

Is the housing index a good indicator of the returns real estate produce?

The closest thing to the 3.1 percent return is an owner-occupant buying a home. But, they would have to pay cash for the property because as soon as they use leverage they will be putting much less money down and increasing the return on the cash they have invested. There are more problems with assuming an owner occupant paying cash will only make 3.1 percent on the money they invest.

- People have to have a place to live in. If they do not buy a house to live in, they will have to pay rent. You cannot take the money you would have used to buy a house and stick it in the stock market. You would have to use it to rent a home, which would give you a guaranteed zero percent return.

- In my market, it is more expensive to rent a home than it is to buy a home. Even when you consider the taxes, insurance, and maintenance that homeowners have to pay, it is usually more cost-effective to buy a home.

- When you buy a home with a loan, you can deduct the interest from your income taxes. You are also paying money towards your mortgage, and you have a house of your own. Life is not all about the exact return you get on your investment. Sometimes, you have to think about the fun factor and what the pride of owning your own house is worth.

After looking at real estate investing or buying a personal residence, there is almost no situation where you would only make the 3.1 percent increase in the housing market has seen since 1900. Having said that, there are some more factors to consider when buying or selling a house. When you sell a house, you have to pay selling costs, which may include paying a real estate agent. You have to pay title insurance and closing costs. But, if you live in a house for two or more years as an owner-occupant, you may not have to pay any taxes at all on the profit you make. This goes to show there is much more to real estate returns than the historic housing market average gain, especially if you invest in rentals.

Why rentals are a great investment

I did not buy my rental properties for appreciation, I bought them for the cash flow they produce. My rental properties have all produced close to $500 a month in cash flow from a $25,000 to $35,000 investment, which produces around a 15 percent cash on cash return. That cash flow is completely independent of the increase of the value of the home. The values of my rentals could go up 40 percent or they could go down 40 percent and that could have no effect at all on my cash flow. There is a chance that a huge downturn in the housing market could cause lower rents. However, the last housing crisis did not cause rents to drop significantly in my market.

The cash flow from rental properties keeps coming in as long as I own the home, and it even increases over time. As inflation goes up, so do rents and my income. When my mortgages are eventually paid off, my cash flow increases even more. My rental properties have been like a stock that has a 20 percent annual dividend that will automatically go up with inflation.

For more information on investing in rentals, check out my book: Build a Rental Property Empire: The no-nonsense book on finding deals, financing the right way, and managing wisely.

Why are my returns so high?

It is not easy to get 15 percent returns from the cash flow on my rental properties. One of the reasons I get such great returns is I can buy real estate below market value. I can buy a home that has a fair market value of $150,000 for $120,000. That doesn’t make sense to many people, but some sellers want to sell quickly, a home needs repairs, or other circumstances create an opportunity to buy below market value. Stocks can’t be bought below market value.

Yes, you can buy stocks that are “undervalued”, but that is not the same as below market value. Market value is what someone would pay for something today in an open market. Undervalued means someone thinks the market has not valued something correctly based on the fundamental financials. You are hoping that the market changes its mind or the asset performs better causing the value to increase in the future.

Being able to buy rental properties below market value allows me to get better cash flow and gain instant equity. When I make 15 percent on the cash flow from my rental properties, I do not even consider the returns from buying below market value. I bought rental property number 11 for just over $109,000. I made about $12,000 in repairs, and the home could have been sold after the repairs for at least $150,000. If you take $150,000 minus the repairs and purchase price, I would make $29,000. For those experienced in real estate, you know I don’t get to keep that entire $29,000. I would have to pay a real estate commission to sell the home, title insurance, recording fees, and closing company fees. On a $150,000 sale, those costs would equal about $7,000 (I am a Realtor and would not have to pay a listing agent).

I came away with an instant $22,000 in equity when I bought and repaired this house. I spent about $32,000 on the down payment and repairs, which means I made about 65 percent on my investment from buying below market value if I ever decide to sell the house. People may say well you have not realized that return if you do not sell, and that is true. However, the same thing can be said for the stock market, except for the stock market.

Because I get really good deals, I am able to make much higher returns on the cash flow.

The stock market produces dividends

I get some push back when I talk about cash flow on rental properties because stocks also produce dividends which are payments while you own the stock. It is true that some stocks pay dividends, but the returns are usually less than 5% and the stocks that pay the highest dividends tend to have the least amount of appreciation.

The returns I used in this article of 7 to 10 percent per year include those dividend returns. The cash flow on rentals tends to be much higher than dividends.

What has the return been on my rental properties?

If you consider the cash flow I make plus the instant equity I gain when I buy a home, I make a great return on my rentals. We have not even considered the increase in value every year that comes with average housing prices or many other factors.

- I put 20 percent down when I buy a rental property, and I pay down my mortgage every month. On rental property number 11, I paid off about $1,500 in principle on my loan in the first year. That amount increases over time as the principle goes down and more of my monthly payment goes towards the principal and not interest.

- When you consider the tax advantages of rental properties, I make even more money. I can depreciate rental property number 11 over 27.5 years, which equates to about $1,050 in tax savings every year.

With those two factors, I make another $2,550 a year, which equates to another 8 percent in returns on my $32,000 investment. If you total the returns I make from cash flow, buying below market value, tax advantages, and equity pay down, I am up to 93 percent. I have not even considered the appreciation or annual housing price increases yet. To be honest, my returns will not be that high every year because I will make the 65 percent only once when I first buy the house. That is still close to a 30 percent return per year.

Why leverage creates greater returns

Another great advantage of investing in real estate is I can buy a $100,000 property with $30,000 in cash (that includes closing costs and repairs). I have to put 20% down, I usually spend at least $7,500 on repairs, and I spend a few thousand on closing costs and carrying costs before the home is rented. By being able to put less money down on a home than the actual cost of the home, the advantages of rental properties are multiplied.

Interest rates are still extremely low on real estate, and I pay about 4 to 5 % on investment properties. When you leverage, price increases and rent increases make the returns even greater.

If I have $30,000 invested into a property that is worth $150,000 (remember I got a great deal) and that house goes up 10 % in value, I gain $15,000 in equity. That is a 50% gain! If you are using low-money-down loans as an owner occupant, the increase in returns is even greater because you have less money invested.

It is possible to leverage some money with stocks by buying on margin. However, margins can be called due when stocks decrease in value and you can’t get a 30-year margin! Margins also will not let you borrow 80 percent of the value of a stock like you can with real estate (usually 40 or 50 percent).

Tax advantages

Rental properties have another huge advantage over the stock market when it comes to taxes. Rental properties can be depreciated over time, which means the initial cost of the structure of a rental property, repairs, and improvements can all be depreciated. The IRS will allow an investor to deduct the depreciated value of the structure from their taxes over 26.5 years and less for improvements. If the structure is valued at $100,000, $3,700 can be deducted from your taxes every year. That is not a $3,700 savings in taxes but a deduction, meaning you would save $1,100 if your tax rate is 30 percent.

You can also deduct most expenses, including the interest on the loans. A 1031 exchange allows you to sell a rental and invest in another property without paying capital gains taxes.

Rental properties get better with time and inflation

When you leverage rental properties, you have a mortgage on the property, which scares some people. But when I calculate my cash flow, I include paying the mortgage payments every month. Every month the mortgage is being paid off slowly by the tenants who are renting the home. On my loans, about $1,500 a year is being paid off every year.

As inflation increases year over year, the price of the property and the price of rent increase as well while the mortgage stays relatively the same. The principal and interest on a loan will stay the same on a fixed-rate mortgage, but the property taxes and insurance will increase with inflation. In most markets, the taxes and insurance will be relatively low compared to the interest and principal.

What are the downfalls of rentals?

So far, real estate sounds amazing, but there are downsides to investing in real estate.

The time needed to invest in real estate

I have mentioned getting great deals and properties with great cash flow. That sounds great, but it takes time and knowledge to learn how to get those deals and analyze rentals. You could invest in a REIT, but I do not consider that the same as investing in real estate. It is definitely more difficult learning how to invest in rentals.

Money needed

It can take tens of thousands of dollars to invest in a rental property but only $100 or less to invest in a stock. There are ways to buy rentals with less money down, but again, that takes more work and knowledge.

Where to invest

Not every market is great for residential rentals. I invested in Colorado, and we have seen huge increases in prices. The increase in prices was great for my net worth, but it made it harder to find cash-flowing rentals and more expensive to buy properties. There are still great markets in the US for rentals, but it is tough for those who live in California or NYC to buy a cash-flowing residential property. There are ways to invest in other markets and in other niches. I invest in commercial rentals now instead of residential.

Liquidity

It is much easier and cheaper to sell stocks than it is to sell rental properties. It can take months and tens of thousands of dollars to sell a property. It can take a few seconds to sell a stock. One nice thing about rental properties is you can access the equity with a refinance or line of credit. That takes time as well, but it is one way to use the equity without selling the property.

Housing market

The housing market could go down as well, but so could the stock market. If the housing market goes down, you are not going to lose all your properties. If you have equity, cash flow, and reserves, you just wait for prices to go back up as they did in the last crash.

How have my rental properties done over the years?

I bought 16 residential rentals from 2010 to 2016. I then bought 10 commercial rentals from 2017 to 2020. I was able to create about $8,000 a month in cash flow from the residential rentals from about $350,000 in cash. I spent over $500,000 to buy those rentals, but I refinanced a few, which gave me quite a bit of cash back. That $8,000 would come in forever and increase over time as rents go up. For some people, that is enough money to retire!

In order to create that $8,000 a month with stocks, I would have needed to invest close to 1.5 million dollars to build up enough money to last 40 years, and that is making 10% a year. However, that $8,000 a month turns into much less over time with inflation.

Those are the numbers from my residential rentals. I have done even better with my commercial rentals, but they take even more work and knowledge.

Conclusion

It is clear to me that rentals are the best way for me to invest my money. They are not for everyone as they do take work. I don’t mean work in the sense that I am getting calls from tenants or repairing the properties—my property manager does all of that. It takes work to learn how to buy rentals and to find great rentals. Stocks are much easier to invest in, but they are much harder to leverage, and it takes longer to retire with stocks than rentals when the right properties are purchased.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.