Is It Smart to Buy Rentals When You Are Young?

There are many challenges if you want to buy rentals when you are young, but there are also many advantages. The biggest challenge to buying rental properties is getting enough money to pay for down payments, repairs, and reserves. However, there are many ways to buy rental properties with little money down, and it is easier to buy with less money down when you are young. When you are young, you can be more flexible, don’t have as many responsibilities, and have more time. When we get older, we have many more responsibilities, less time, and are not willing to make as many sacrifices in our living situation.

How much money do you need to buy a rental property?

The biggest challenge to buying a rental property is saving enough money for the down payment and other costs. As an investor, you will have to put down 20 percent or more when dealing with traditional banks. I usually spend at least $30,000 on the rentals I buy priced around $100,000. I need 20% for the down payment, money to repair the home, and I have to pay for carrying costs. I like to buy homes that need repairs because I am getting a great deal and will make more money in the long run. You do not have to spend $30,000 on a rental property if you can be flexible in your living situation.

A big problem that many people have, including myself, is that it is tough to find rentals that are $100,000! I used to have my pick in Northern Colorado after the housing crash, but now those houses are $300,000! If you have to spend $300,000 to buy a rental property, you don’t need $30,000—you need $90,000.

You have the option to buy in another market or change niches, which is what I did by purchasing commercial rental properties instead. Or you can look for ways to buy with less money down.

How to buy with less money

The easiest way to buy a rental property with little money down is to buy as an owner occupant. An owner occupant usually has to live in a home for one year to satisfy the owner-occupancy requirements. The tough part about buying as an owner occupant is many people don’t want to live in the houses they use as rental properties.

When you buy as an owner occupant, you can put 3.5% down with an FHA loan or even $0 down with VA or USDA. There are even down payment assistance programs that will decrease the down payment, and you can ask the seller to pay for the closing costs, which can eliminate them. Buying as an owner occupant can reduce the money needed from $30,000 to $5,000 or even less. It is entirely possible to buy a house with $1,000 in the right market with the right loan.

There are also ways to buy multifamily properties with little money down as an owner occupant. This is commonly called house hacking and someone lives in a property and collect rent while living there as well.

Why is it easier to buy rentals when you are young?

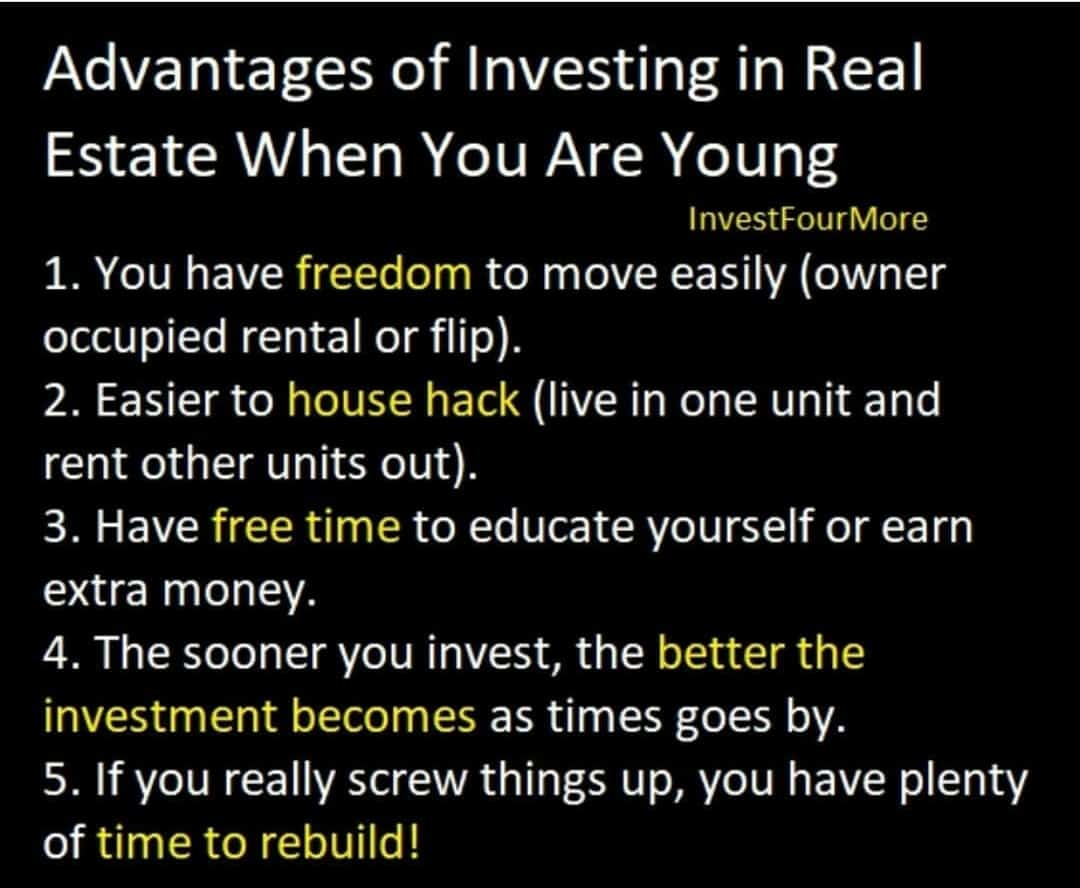

One of the tough things about investing with little money down is it takes a lot of sacrifices from the investor and their family. If you are older with a family, it can be really hard to move over and over. It can also be really hard to move into a property that makes sense as a rental. It is also tough for families to live in a home that needs work.

When you are young, you can buy a rental property as an owner occupant and live there for a year and move out of the property. The next move for many investors is to buy another rental property and repeat the process. This strategy takes a lot of moving and flexibility, and most families do not want to move every year. When you are young with nothing to tie you down (and less stuff), it is much easier to move every year. The great part about buying as an owner occupant is you can keep buying houses with little money down.

You also do not have to spend money on repairs right away because you can slowly repair the house while you live in it. There will be requirements pertaining to the condition the home must be in to get owner-occupied loans, but it is still very possible to get a great deal as an owner occupant buyer.

Young investors have more time

It takes time to learn how to buy rentals properties; what strategy you want to use, where you want to invest, and to learn about your market. As we get older we have less and less time. You get married, have kids, have a job and it is tough to find time for your kids, let alone your own hobbies or learning how to invest. Younger people often have more time to learn and educate themselves. Even if you are young and have no possible way to buy a property, you can still learn how to invest in rentals and develop a strategy that fits your goals so that when you can buy, you are ready.

I like to be a very positive person, but that does not mean I do not plan for the worst-case scenario. Another advantage of being young is you have more time to recover if you make a mistake or run into bad luck. If you buy a rental property when you are 25 and end up losing money on the rental, or even worse, losing that rental property, you have a lot of time to recover and build. If you are 60 and lose a rental property or make a bad investment, it is much harder to recover. I am not saying you should not invest when you are 60. I think any age is a great time to buy rental proprieties, but the sooner you buy the better.

I wrote a book for young investors called: Buying Into Success. It is all about a college grad on the rat race who discovers real estate. You can find it on Amazon as a paperback and Ebook.

Young investors only have to convince themselves to invest in rentals

There are many people with negative beliefs about rental properties and real estate. Those beliefs are not always founded on facts, but rather, hearsay. Convincing someone to change their beliefs is not easy no matter how favorable you think your argument is. When you are young without a spouse or children, you only have to convince yourself that investing is a great idea and will help you financially. When you get married and have children, you will have to convince your wife, children, and possibly your in-laws that investing is a good idea. If just one of those people has a belief that real estate investing is dangerous and could hurt the family, you may never be able to change that belief.

If you invest in rentals or real estate at a young age and make money with investments, you won’t have to worry as much about convincing someone it is a good idea. You will have proof that you made money, and your loved ones will get to know you as someone who is a real estate investor.

Why do the returns on rental properties increase as time goes by?

The longer you own rental properties, the better investment they become. Here are a few basic advantages of buying rental properties when you are young and holding them long-term.

- Cash flow: Cash flow increases with time as rents rise and mortgage payments stay the same or mortgages are paid off. Rents will not always increase, and it may take years, but historically, rents have always increased.

- Appreciation: I do not count on appreciation to make money, but houses also appreciate over time. The longer you own a home, the more it appreciates. If you get a loan on a house, the the gain in appreciation is multiplied. As an owner-occupant, you might only put $5,000 down on a house, but it could appreciate $20,000 in one year. A house may also decrease in value over the short-term, but if you own it long enough, it will increase in value.

- Tax advantages: You are allowed to depreciate rental properties for over 27.5 years, which saves a lot of money on your taxes. You can also complete a 1031 exchange into another investment, which could allow you to sell for a huge profit without paying taxes.

- Build passive income: Over time, one rental property may not make you a ton of money, but if you buy multiple rental properties, you can make a lot of money.

How much money do you need to buy a rental property as an owner occupant?

The amount of money needed to buy a rental property will vary on the property and the loan program. I discuss various loan programs here, but most owner occupants should be able to get a loan with 5 percent down using conventional, 3.5 percent down using FHA, and no money down using VA or USDA. There will be closing costs associated with the loan, which can run from 2 to 5 percent, but you can ask the seller to pay those for you. If you buy a home that needs repairs, you will have to spend money making those repairs, but you don’t have to do it right away. You could repair the house as you live in it, saving time and money over hiring a contractor.

I usually do not recommend doing the repairs on investment properties yourself if you do not live in the property. If you try to make the repairs on an investment property yourself, it often takes much more time and costs you more money in the end over hiring a good contractor. If you are living in the home, it is easier to make the repairs because you are always there, and taking more time to make the repairs will not cost you money since you can’t rent out a single-family house for a year anyway.

If you use a no-money-down loan and make repairs while you live in the home, you could buy a rental property with no money and then spend less than $5,000 in total on repairs depending on what you fix. If you have to use a higher down payment loan, your costs will increase, but it will be much less than buying as an investor. Remember, with less money down it will be harder to get positive cash flow on a home because of the higher mortgage payments.

How can young investors qualify for a loan?

The biggest challenge for young investors is qualifying for a loan. The good news is that it is easier to qualify as an owner occupant than an investor. With current lending guidelines, you will need a steady job, good debt-to-income ratio, and good credit to qualify on your own. Many young investors cannot qualify for a loan on their own because they have bad credit, too much debt, or they do not make enough money. There are options for those who cannot qualify!

- Kiddie Condo loan: A kiddie condo loan allows relatives to co-sign on a property. The co-signors credit and income will help to qualify for the loan.

- Regular co-signor: Depending on the loan program, any co-signor may be able to help with poor credit or income.

- Seller Financing: Seller financing is when the seller of the home loans money to the new buyer. It is rare to find seller financing in my area, but it can be a great deal for both parties in certain situations.

- Partners: Many investors are looking for a place to earn higher returns than a CD but want more security than the stock market. Real estate provides collateral, and some investors may be willing to loan money on real estate because it is safer than the market.

If you cannot find any options to qualify for a loan, you can still learn about investing and start working on qualifying. It is better to know as soon as possible what you have to do to qualify for a loan than to wait until you are ready to buy and find out you have to wait 18 months to get a loan.

Buying a multifamily home as a young investor

I like to buy single-family homes for a number of reasons, but mostly because they give me better returns in my area. It may make more sense to buy a multifamily property depending on your market and situation. Investors can buy a multifamily property as an owner occupant if it is 4 units or less and they occupy one of the units. You would have to live in one unit for a year, but you can rent out the other units as soon as you buy the property. In many cases, the rent from the other units will cover the mortgage payments and let you live in the property for free. Once the year is up, you can continue to live for free or move into another property and repeat the process.

Why is it harder for people to invest in rental properties when they are older?

Many people have a plan to invest in rental properties once they have become settled in life.

“When I have a great paying job, a family, and a nice house, I can use my extra money to invest in rentals.”

The problem is that the older we get the more responsibilities we have and the more money we spend. The nice house, nice cars, and family all cost a lot of money! We also have much less time than we used to because of a great job, a nice house, and the family. It is not a given that you will have a lot of extra money when you get older. However, rental properties are a great way to give yourself extra money when you are older without having to depend on a job to produce income. I love the cash flow my rentals produce, even though I make much more income from flipping.

Conclusion

Most people wait to invest in rental properties or to do any investing at all until later in life. Young people tend not to think about their future or feel it can wait to start building passive income. I think it is actually harder to invest later in life because we all have so many responsibilities, less time, and more to lose. The sooner you start investing, the better off you will be later in life, and we get older sooner than we think.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.