Why You are Better Off Buying a House Rather Than Renting

There is a growing sentiment that it is better to rent than to buy a home. People argue that owning a house is much more expensive rather than renting because you have to pay taxes and maintain the house. You also have to spend more money on down payments than you would be if renting a house. I believe that it makes sense to rent sometimes, but for most people, buying a house is a better financial decision than renting. If you look at the numbers, the majority of most people’s net worth comes from their home. Homeowners have 44 times the net worth of renters. Middle-aged people have 70% of their net worth in their homes. These are the averages for consumers who have no idea what they are doing and blindly buy whatever house they think feels right. If you take your time to get a great deal, get the right loan, and be smart when buying, it can be an amazing investment that takes very little money.

Owning a home can also be less risky than renting. Rents constantly increase while mortgage payments are usually locked in. When you own a home, the landlord cannot ask you to leave in a year because he wants to sell. You can have pets, make whatever repairs you want, and have more security.

Even if you are an entrepreneur looking to make as much money as soon as you possibly can, I think buying a house can be a great way to boost your business. I bought my first rental property thanks to the money I got from my personal residence after a refinance. When I sold my primary houses, I made huge profits tax free—another huge perk of buying real estate.

The video below goes into all the details of renting verse buying with a note where I talk about each topic as well:

What do the statistics say?

Before I get into all the reasons I think most people are better off owning than renting, I wanted to show the stats. Anecdotal stories are great to get your attention, but I like to look at studies and the overall numbers.

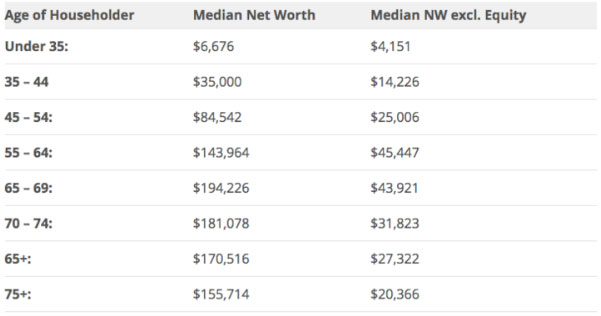

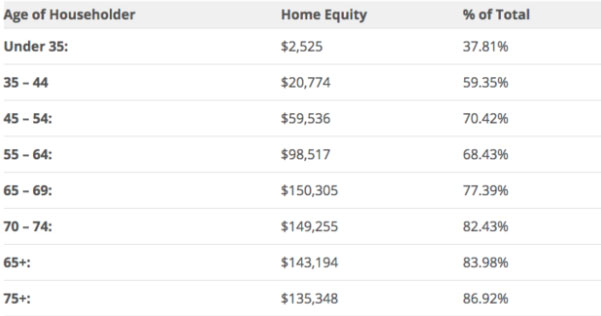

This chart shows the median net worth of US households with and without equity in their home:

The vast majority of most people’s net worth is in their house. If you look at the chart above, it shows the median net worth for people in the United States with and without their home equity. If you look at the chart below, it shows the total percentage of people’s net worth in the United States from their home equity.

Thank you to Business Insider for these stats.

Homeowners also have 44 times the net worth of renters. A lot of factors go into that stat, like the fact that most wealthy people own houses. However, while that may skew the scale, it also shows that wealthy people think it is a good idea to own as well.

Is buying always better rather than renting?

When deciding whether it is better to rent or buy a house, you have to consider where you want to be in one, five, or even ten years. The longer you stay in a location, the more sense it makes to buy a home. Real estate prices have historically always gone up, but they can also decline in the short-term. The longer you live in a home, the better chance it will go up in value. If you plan to move in one year or two years, it may be smarter to rent. Here are some other considerations when buying or selling a house.

- It costs money to sell a house. If you have to sell, you need to sell the home for six to ten percent more than you bought it for to break even.

- It can take time to sell a house. In today’s market, houses are selling very quickly, but in a down market, it can take months to sell a home. If you want to move quickly, buying a home can be a hindrance.

- Can you qualify for a loan to buy a home? If you can’t get a loan to buy a house, then renting is the obvious choice. To qualify for a loan, buyers need to have good credit, a steady job, and enough income to cover their current debt and a new mortgage. Many people don’t realize that a large car payment or two can greatly affect their ability to qualify for a loan. Credit card debt and any payments that you make for appliances, furniture, or student loans all affect your ability to qualify for a mortgage.

- Property taxes vary greatly from state to state. If you are buying in Colorado where I am, the property taxes are very low, but if you buy in New Jersey they could be ten times higher! Some states also have transfer taxes and other fees when you buy and sell.

Having said all that, even if you are planning to move soon, you can always rent the house. If you get a good deal, you can sell it. If you took your time buying and not just choosing the house that felt right, owning a home should not stop you from moving or exploring.

Why does Grant Cardone say you should always rent?

Grant Cardone is a very popular real estate investor, marketer, and social media influencer. I mention Grant Cardone in this article because so many people tell me a house is not an asset but rather a liability because of him and Robert Kiyosaki (Rich Dad Poor Dad). Cardone has been on a mission to tell everyone how dumb it is to buy a home. He likes to use the example of someone buying a $1,000,000 house with a $200,000 down payment. In this case, I would agree it might be better to rent. However, this is an extreme example, and most people are not buying million-dollar homes.

If you live in a very expensive area, it also might be wise to rent. I will go over whether it is cheaper to rent or buy soon, but in most really expensive areas, it is often cheaper to rent. In cheaper areas, it is usually cheaper to own.

What Grant misses is that it is possible to buy a house with very little money. You do not have to put 20 percent down. You can put 3.5 percent down or even $0 down in some cases. It is very tough to find any other investment where you can put so little money down with absolutely no experience investing in that asset. When you sell, if you lived in the home for 2 out of the last 5 years, you usually pay no taxes on the profit!

Is a house a liability?

Another common theme among those who are against home ownership is calling houses liabilities…. If you live in them. Now, if you rent them out or use them as an investment, they become assets. This theme was made popular in Rich Dad Poor Dad. The theory is that because you have to pay to stay in your house (mortgage payment, taxes, insurance, etc) and the property does not make you any money, it is a liability. I would argue that this definition was made up and is not the correct definition.

I like to ask people who bring up this point if a stock, fine art, gold, and silver, are liabilities as well. They do not make you any money while you own them, only when you sell them, just like a house you live in. You also have to spend money on some of them to keep them. You may need security, or you might need to pay someone else to keep them safe for you. There is also a commission or fees when you sell them.

Finally, a house you live in can make you money. You could rent out a room or buy a multifamily property and rent out the other units. You could also be earning money from mineral rights! On top of that, you would be paying rent if you did not own the house, so in a way, it makes you money by saving you rent as well. The trouble with this idea is that a house changes from an asset to a liability based on if it makes money or not.

A house is an asset, and the loan against the house is the liability. Liabilities are loans or debts, and assets are things with real value, just like a house.

Below is a video I put together on this subject as well:

Is rent or a mortgage payment cheaper?

Some markets are better to rent in, and some markets are better to buy in. In my market, rental rates are extremely high compared to what you can buy a house for. I think this makes my area great for landlords that want to make money with rental properties, but it makes it hard for people who want to rent houses. Here are some numbers on renting versus buying in my area.

Buy a house for $200,000

- Mortgage payment with 3.5% down: $928

- Taxes and insurance: $200

- Mortgage insurance: $200 (required on most loans with less than 20% down)

- Total payment: $1,328

- Total cash needed: $7,000 (assuming seller will pay for buyers’ closing costs)

Rent a house worth $200,000

- Rental payment: $1,600

- Total cash needed: $3,200 (for first month’s rent and deposit)

There are a lot of things to consider when deciding whether to rent or buy in this situation. The monthly payments are more when you rent, but there is more cash needed to buy the home. Now, if you can use a VA loan, you may be able to put less money down, which might make buying a better option. When you buy a home, you do not have to make a payment until the second month you own the house. That would save you another $1,328. Even though you are paying more cash with buying a house, that cash is going towards the house.

When you put less than 20% down, you must pay mortgage insurance on most loans (VA and some loans do not have mortgage insurance). When enough equity is built into the home, you can sometimes remove the mortgage insurance or refinance into a loan without it.

When you buy a house, part of your mortgage payment also goes towards paying off your loan. About $200 of your $1,328 mortgage payment will go towards equity pay down at the very beginning of the loan. As time goes by, more and more will go towards paying down the principal of the loan.

After one year, you would pay off $2,000 or more of your loan when you buy a house. This is why it is important to know how long you think you will live in a house or an area. The longer you live in a house, the more equity you will gain through mortgage pay down and possible appreciation. When you buy a house, your interest part of the mortgage payment is also tax-deductible. The savings from the tax deductions will vary based on your tax bracket, but for the average person, this may mean $2,500 a year (this may not be as big of an advantage with new tax laws).

Looking at the numbers more closely, buying a house saves $272 in lower payments, $200 in equity pay down, $196 in tax savings, and $500 a month if a house appreciates 3% a year. That totals over $1,100 a month in savings if you buy a home instead of renting one.

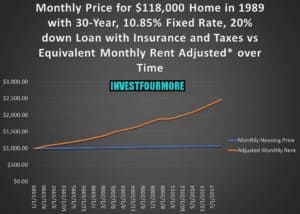

If you plan to stay in one area inflation will also cause rents to increase over time. People often forget that rent will increase and their payment will stay basically the same when they get a fixed-rate mortgage. The graph below shows how the rent has increased in the past 30 years compared to a mortgage where only the taxes and insurance are increasing. Also, note that interest rates were over 10% 30 years ago! With today’s rates, you would save more than $450 on this payment.

In markets that have cheaper houses (in the $100,000 range), you save even less money buying instead of renting. The lower the prices, the higher the rents are relative to that price. For example, if you buy a $100,000 house, your payment would be less than $500 before taxes and insurance, and most likely around $600 a month after including taxes and insurance. The rent would be from $800 to $1,200 a month.

This is how landlords make money and why they buy rental properties.

What about the maintenance and repairs a house requires?

When you rent a house, you do not have to pay for maintenance and repairs. The landlord will pay to make repairs for things that break or wear out. When you own a house, you are responsible to pay for the maintenance and repairs.

When an investor owns a rental property, a good rule of thumb is that 10 to 20% of the monthly rents will be used for maintenance. When you own a home, I think that the same figure can be used to determine how much maintenance a home will need. If your house payments are $1,300 a month, you can count on at least $1,300 a year in maintenance and repairs. $1,300 is not a lot of money to spend on maintenance, but often, we want to improve a house or make updates to houses we own. Improvements are a hard thing to value, but in most cases, they add value to a home. In some cases, they will add more value than they cost, and in other cases, they will add less.

When you spend money on your house by painting it, replacing the carpet, or remodeling a bathroom, you are adding value. It is not wasted money because it increases the value of the home.

It is also true that you must mow the grass, take care of the yard, and perform other maintenance tasks when you own. When you rent an apartment, you will not have those responsibilities, but when you rent a house, you do! Almost all single-family rentals with yards will require the tenant to maintain those yards. If you don’t want a yard, you don’t have to rent—you can buy a condo or patio home where that is taken care of for you.

Make sure you are comparing apples to apples when looking at the costs or renting versus buying. Don’t compare a 600-square-foot studio apartment to a 4,000-square-foot house with a 10,000-square-foot yard.

The video below explains how much it costs to fix up a home:

What about inflation?

Many people forget about the time value of money as well. As time goes by, inflation causes money to be worth less and less. If you are renting, the rent will go up over time. It might not go up every year, but it will go up.

- If you are renting for $1,600 now, with 3% inflation, that rent will be $3,883 in 30 years.

- If you get fixed-rate mortgage, the principal and interest portion will stay the same over 30 years. The payment will always be $928, but the taxes and insurance can increase. If taxes and insurance are $200 a month now, that could increase to $485 in 30 years.

Your total rent in 30 years would go from $1,600 to $3,883 while the mortgage would go from $1,128 (with taxes and insurance) to $1,413.

Is a house an investment?

Up to this point, it looks like buying a house beats renting a house, but there are many factors we have not considered. In many areas, rental prices are not as high compared to mortgage payments, as they are in Northern Colorado. In some areas, house prices are extremely high, and they have rent control which keeps rent low. Even in those areas, there is one thing that will always make buying a better option.

Buying Below Market Value

If you can buy below market value, you can gain instant equity as soon as you sign the paperwork. When I buy houses, I want to buy them at 20% or less of what they are worth. For me, I would want that $200,000 house for $160,000, and I would make that equity as soon as I bought the home. To get a deal like that, I might have to make repairs (if I was making repairs, I would want to buy the house even cheaper), and it would take a lot of work and patience finding the deal. If you are willing to do the work and find those deals, buying beats renting every time.

It is not impossible to get those deals either. I flip houses (did 26 flips last year), own rentals, and own a real estate brokerage. I have a huge advantage when buying houses, but I still get beat out by owner-occupied buyers all the time. Owner-occupied buyers have an advantage over investors in what they can pay and what they can buy.

Many banks give preference to owner-occupied buyers when selling foreclosures. When I buy a flip, I have to get an amazing deal because I have to repair it, sell it, and hold it. I have to cover all my costs and then some to make a profit. Owner-occupied buyers do not need to get as good of a deal, but they can still get a great deal to them that creates instant equity.

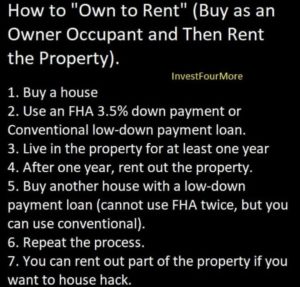

How can entrepreneurs use their house as an investment?

Many of the cases against buying a house have to do with entrepreneurs wasting their money on a house instead of using it to invest or start a business. A house can be an amazing tool to create wealth to invest! I have done it multiple times with the houses I lived in, as can almost anyone else. Here are the steps:

- Qualify for a low-down=payment loan

- Find a great deal on a house that is well below market value

- Fix up the house a little bit

- Refinance the house and get your tax free money

If you got a good enough deal, when you refinance, which means getting a new loan on the house to replace your old loan, you should be able to get back all the money you spent buying the house and then some. You have more money to invest than you did before you bought the house, and you have an asset that you own with zero out of pocket dollars. If prices go up, your return is infinite.

Doesn’t the housing market have worse returns than the stock market?

Another point that is brought up is that the housing market has horrible returns, only 3% historically over the last 100 years. I cannot dispute that number, but the number is not represented correctly when people use it against the housing market.

“The stock market makes a 7% return, but housing only makes 3%, so the stock market makes you more money!”

What they are forgetting is almost everyone uses cash to buy stocks, but very few people use cash to buy houses. What would the returns be in the scenario we used above?

- Use $7,000 to buy stocks that increase in value 7% a year

- Return per year: $490 ($7,000 x .07)

- Use $7,000 to buy a $200,000 house that increases in value 3% a year

- Return per year: $14,000 ($200,000 x .03)

After ten years the difference is astounding:

With the stock market, you turned your $7,000 into $14,000, and on the house, you turned your $7,000 into almost $70,000, or at least the house is worth $270,000, but what did you make?

- Your actual loan was $193,000, not $200,000, ,thanks to the down payment.

- You have now paid the loan down to $152,000 thanks to monthly payments.

- You did not have to pay rent the entire time.

- This assumes you paid full retail value.

Your $7,000 actually turned into more than $115,000 in ten years. If you would have gotten a great deal, you would have made close to $150,000 in ten years. If you made any improvements, you could have increased the value even more. All of this from that measly 3% appreciation per year. This is why homeowners have 44 times the net worth of renters! I personally have seen more than a 10% increase in prices on my rentals, but I would never count on that high of a return.

What do the most recent studies say?

I have thrown out a lot of numbers, but you don’t have to believe just me. A recent study from Florida Atlantic University stated renting is cheaper than buying for most people. This study was shared by many news sites, blogs, and people on Facebook (who also stated renting is better than buying because of this study). However, I think there were some major problems with this study that were left out of those stories, and the authors themselves admit that buying is still the better option for most people. The study compared buying to renting with the following assumptions:

- A renter would invest all the money they saved from not buying a house into the stock market.

- A home buyer would put 20% down to buy a house.

- A home buyer would have 2% closing costs to buy a house.

- The home buyer would hold the house for 8 years and then sell, paying 6% in selling costs.

- Property taxes would be 1.5% of the property value each year.

- Maintenance and insurance expenses would be 2% of the annual house value.

- Homeowners would pay 25% of their profits to taxes.

There are some major problems with these assumptions.

- The homeowner would not pay any taxes on their gain because of the tax-free capital gain rule on selling a house you live in for 2 out of 5 years.

- Most homeowners do not put 20% down. 70% of first-time homebuyers who get a loan put less than 20% down.

- Property taxes are often much lower than what this study assumes for insurance and maintenance costs.

- Very few people will ever invest all the money they would have used to buy a house in the stock market. They would spend it.

To show how much the assumptions made in this study change the money you would make from buying a house, I will use an example. I will assume someone buys a house for $200,000, and this is the money that would be saved:

- If the house saw a 4% appreciation every year for 8 years, the house would be worth $273,714. The study assumes a homeowner would pay 25% in taxes on the $73,714 in profit, but they would not pay any taxes with current or proposed tax laws, saving $18,428.

- The article assumes 2% of the house value would be used for maintenance and insurance each year. That means $4,000 per year would go towards these costs, but insurance would be less than $1,000 per year in most markets. That means $3,000 per year goes toward maintenance. That could be the case, but that money could also be increasing the value of the house. If you spend $24,000 on maintenance over 8 years, you are most likely making improvements as well. The increase in value caused by those improvements and maintenance are not accounted for in this article. It is hard to put a dollar figure on what those improvements would do, but I assume they will add 5% in value, or $13,685 (based on the $273,714 value).

- The article assumes the tax rate is 1.5% of the value of the house each year, which would be $3,000 per year on the $200,000 house. I live in Colorado, and the taxes on a $200,000 house would be around $1,000 per year. In many cases, the tax assessed value is also less than the actual value. You could live in a state with even higher taxes, but in my area, you would save more than $8,000 over what this study suggests.

- If you put 20% down on the $200,000 house, you would be spending $40,000 on the down payment. There are many loans available that will allow homeowners to put less than 5% down. That would mean the homeowner is putting $10,000 or less down—instead of $40,000 down—saving them $30,000.

- You would spend $70,000 less in my area over what this study suggests when you buy a house. There would be some additional costs using a low-down-payment loan, like mortgage insurance. Even with mortgage insurance that lasted the entire 8 years (some mortgage insurance can be removed), you would spend less than $20,000.

The other major problem that this study creates is the amount of money invested when renting a house. It assumes that when you rent, you would invest that $40,000 down payment into the stock market or an equivalent investment. That $40,000 would grow to almost $68,727 in 8 years at a 7% interest rate. The study also assumes if you save any money at all renting (which you would base on the high maintenance, tax, and insurance numbers they use for buying), you would invest all of that money into the stock market as well.

Most people will never do that: they will spend the money they save and not invest it. The study admits this fact and concludes that most people should buy because of it. If most people are not putting 20% down, they are not investing $40,000 into the stock market in the first year either. With a 5% down loan, they would be investing $10,000 into the stock market, which would only increase to $17,182 after 8 years at 7% growth each year.

The reason this study shows that renting is cheaper than buying for most people when almost every other study has shown the opposite is they made some really bad assumptions that are not realistic. They also made some gross errors such as the taxes on capital gains.

They admit some of these scenarios are not realistic, and that is why they also say most people should buy. In most real-life scenarios, people would make at least $50,000 more from buying than the study suggests and end up with $50,000 or less than the study suggest from renting (this assumes all money saved is reinvested into the market). That is more than a $100,000 difference, and the study still shows that it is better to buy than rent in some markets! I give a lot of credit to the study for breaking down the data in different markets based on rent-to-value ratios and other costs, but it is not very accurate compared to what happens in the real world.

What are the risks of renting houses?

I own 20 rentals and have completed over 170 house flips over the last 17 years. On my rentals, we have raised rents 50% or more in the last 7 to 9 years, yet my mortgages have stayed the same. We don’t raise rents very often on people who stay in the homes, but people leave, and we raise the rents when we re-rent the property.

On my flips, I run into tenants who have lived in properties for years. The landlords never raise rents, and the tenants get used to low rents but are forced into a very rough situation when rents are raised to market or they are forced to move.

On one house I bought, the tenants were paying $400 per month, yet the market dictated $1,000 per month. I was going to flip the property, and I had to be the one to tell the tenants they would have to find a new place to live. I gave them plenty of time to find a new rental, but it was almost impossible for them to find a place with rental rates near their current rate. There are many other cases where tenants are forced to move, and they have to come up with a deposit and first month’s rent on a much more expensive place.

Whenever you rent, you run the risk of being forced to move when your lease is up. You also run the risk of having a landlord who will not make repairs or maintain a property. If you break your lease and move out early, you can be held liable for the rent owed for the entire lease. If you damage the property, it will come out of your deposit, but if the deposit doesn’t cover it all, the landlord can take you to court to collect the rest.

What if you can’t make your payments?

One of the big scares of buying a house is that the market crashes or you lose your job and cannot make payments. People are very afraid of foreclosures as they can wreck your credit for years. They can also prevent you from buying a house for years. However, missing rent payments can also hurt you financially and be much more troublesome than a foreclosure.

When you stop paying rent, the landlord can evict you after missing one payment. Depending on what state you live in, it could take a couple of weeks or a couple of months to complete the eviction. The landlord can take you to court to go after the eviction costs and any property damage you caused. A tenant’s liability is not limited to just their security deposit. If the court finds in favor of the landlord, a judgment can be placed against the tenant, which can hurt the tenant’s credit and prevent them from buying or renting.

The process is much different when a homeowner goes through a foreclosure. The homeowner will have to miss multiple house payments, and the bank will have to go through a foreclosure process, which could take a couple of months or even a couple of years depending on the state.

The bank cannot legally kick someone out of their home until the foreclosure is completed. The homeowners can technically live in the home for free until the house sells at the foreclosure sale. Even after the foreclosure is done, the bank will have to complete an eviction to get the owners out of the house. In some cases, the bank will offer the homeowner cash for keys, which means they will pay them to move out! That will most likely never happen in a rental property.

While most people think that renting a property is the safer option, buying a home is—financially—the better option, especially if you get into trouble. It takes much longer to lose your house when you own it. If you have equity, you might be able to sell before you lose the house, and in the worst-case scenario, you get to live rent and mortgage free for months or even years. You can save up money to pull your life together. If you are renting, you will be kicked out much sooner, and it is going to be very hard to find another place to live with no money and no credit.

If housing prices plummet, you do not have to sell. Your mortgage will stay the same and you can keep living in the house just as you did before. Wait out the dip and no harm done. Even if you have to move, rents don’t always decrease when housing prices decrease. You could rent the house during the downturn.

Is it smart to be “house poor”?

Something else many people mention is being “house poor.” That means you buy the most expensive house you can afford and have no money left to invest. I agree that it is not smart to be house poor and spend all your money on a home. I think it is smart to spend less than you can qualify for.

I also think that you can be rent poor and spend all your money on rent as well. Being house poor does not make buying a house a bad idea—it makes spending too much money on a house compared to what you make a bad idea.

How can a house be a great investment?

We have talked about how a house can be a good investment for those who are not even trying. It is forced saving for those who cannot save otherwise. We talked a little about how entrepreneurs can make a house a decent investment. Buying a primary house can be an awesome investment for those who want to be real estate investors. Here are some advanced strategies:

House hacking

House hacking is when you buy a house or multifamily property, live in part of it and rent out the rest. You can get a low-down-payment loan since you live in the property, and the rent you make from the other units should pay for your mortgage and then some. Not only do you own a property, but the rent pays for all of your expenses! After one year, you can rent out the entire property and buy another as an owner occupant.

BRRRR

BRRRR stands for Buy, repair, rent, refinance and repeat. It is a fantastic strategy that has been around for a long time and has a new fancy name. The strategy is similar to house hacking. Buy a house or income property, fix up the property, rent it out, and then refinance it to get the money you spent repairing back out. If you get a good enough deal, you can get your down payment back as well after the refinance.

Live-in flip

This strategy involves buying a house as an owner occupant and, while living there, fixing it up. After living there a year or two, you can sell and repeat the process over and over. By living in the home you can take advantage of low down payments, and if you live there for two years, you pay no taxes on the profit in most cases!

What are some advantages to renting a house?

Even though buying a house is the better option for most people, it is not better for everyone. If you want to make the best financial decision, you need to look at your situation, your needs, and how much time and effort you are willing to devote to the process.

- If you move constantly, selling a house is expensive, and it can take months as well. If you are constantly moving, maybe renting is better.

- If you cannot qualify for a regular loan and have to pay high-interest rates, buying may not be worth it.

- If you do not take the time to get a good deal or overpay for a house, it could take years to make up for it.

- If your area has really high property taxes, really high insurance, or the rent-to-value ratios are really low, it may make sense to rent. For example, in one market you may be able to rent a $100,000 house for $800 per month. In another market, you may rent that same house for $1,300 per month. It all depends on supply and demand. This again assumes you are moving fairly quickly and not staying in one house for many years.

- If you live in a very expensive area, it might make sense to rent instead of buy.

How have my houses been a good investment?

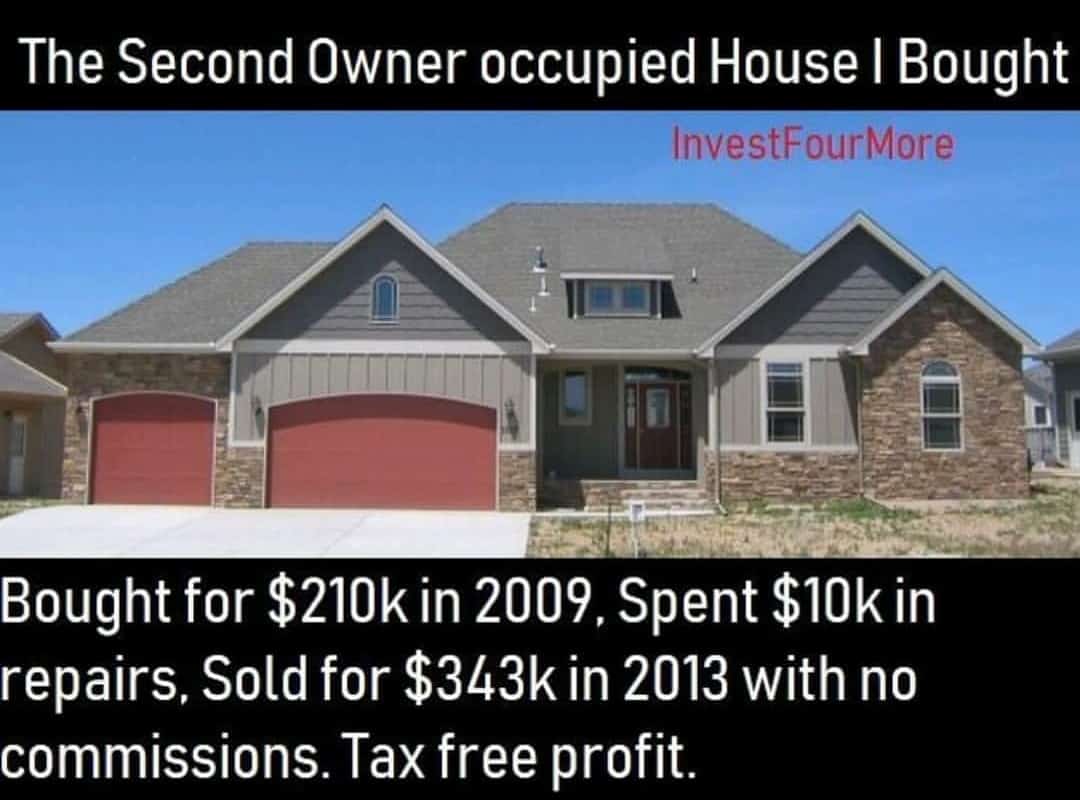

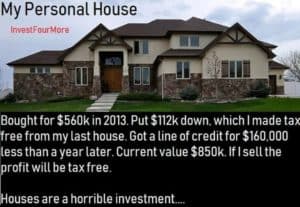

Here is my anecdotal story about making money with my primary house. I bought my second house from the foreclosure sale in 2009 for $210,000 and sold it in 2013 for $343,000.

I did not have $210,000 in cash, which I needed to buy the house from the foreclosure sale. My sister and father in law agreed to lend me the money I needed for a few months. I was able to buy the house, wait a few months, and refinance the house for $230,000, which allowed me to pay everyone back and have a little leftover.

We ended up living in this house for 4 years. I sold the house to my team manager and friend Justin for $343,000 in 2013. We had no real estate commissions, and I spent less than $10,000 making repairs on that house. At $343,000, it was still a good deal for Justin, and I made well over $100,000 on that house tax-free.

I wanted to buy rentals for many years, but part of the reason it took me so long was saving up the money for the down payment. Since I got a great deal on my second personal residence, it was easy to refinance. I refinanced it once right after I bought the house and again one year later. I was able to pull out $50,000 the second time I refinanced it. I used that $50,000 to buy my first rental in 2010. Not only did the property make me more than $100,000 tax-free but it also allowed me to buy my first rental.

It took some work to make that deal happen, but there are much easier ways to get deals on houses. You also don’t need cash to buy most properties unless you are buying from the foreclosure sale as I did.

Conclusion

Buying a house can be an amazing way to build wealth without having much money to start with. It has helped me tremendously, and the numbers show it is a good investment for most people, even when they have no idea what they are doing. For those who want to get ahead in life, it can be a great way to create capital for investing or starting a business. Sure, if you buy a $1,000,000 house with 20% down, it may not be the best use of your money. So, don’t buy a million-dollar house! If you live in a crazy expensive market and want to get ahead in life, why not move somewhere cheaper?

If you want to be a real estate investor, which has been awesome for me, buying a primary house can lead to many opportunities. Do not ignore the tax advantages and the low-down-payment loans you can get with a primary home!

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

I enjoy each and every one of your blogs and look forward to them. Thanks for sharing.

Great blog! I’m a real estate investor and like to read different blogs to grab sufficient investment information. Your blog provides great knowledge of investment in a good manner. Thank you!

very nice blog and informative thanks for sharing .and keep sharing like these type of content .

Great blog! Thanks for sharing