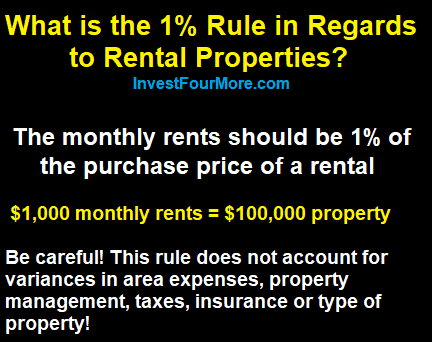

What is the 1% Rule in Real Estate Investing?

Rental properties can be an amazing investment, but not every property will make a good rental. One way many people analyze rentals is with the 1% rule. The 1% rule in real estate investing states if the rents are 1% or more of the purchase price (or purchase price plus repairs) of the property, it will be a good rental. For example, if property rents for $1,000 a month, to be a good investment, it cannot cost more than $100,000. I think this is a good general rule, and I bought many of my properties close to this rule, but I am not a fan of using only rules to figure out what a good rental is. There are also many things that can change the returns on a property besides the rent and purchase price. The expenses can vary greatly based on the type of property, location, loan, and much more.

How do you calculate the 1% rule?

It is fairly easy to calculate the 1% rule:

- Monthly Rents = 1% or more than the purchase price.

There can be some variations on the rule since many rentals are bought needing a little work. A property that needs $30,000 in repairs cannot be considered the same as a similarly priced property that needs no work. Many people also include the repairs into the calculation:

- Monthly Rents = 1% of more of the purchase price + repairs

If you bought a property for $100,000 but it needed $30,000 in work, you would need to get $1,300 a month in rent for that property to meet the 1% rule.

The video below goes over the 1% rule as well:

How much money will you make with the 1% rule?

The 1% rule can be a great basic rule in the right market, but how much are you actually making if you meet the rule? Where did the 1% rule come from? Investors have typically found that properties need to meet the 1% rule in order to make enough money every month to cover expenses and leave something for the landlord.

Here are what the expenses could be on a rental property that rents for $1,500 a month:

- Property taxes: $200 a month

- Insurance: $100 a month

- Property management: $150 a month

- Possible maintenance: $150 a month

- Possible vacancies: $75 a month

That totals $675 a month in expenses, which would leave $825 a month in profit! That is pretty good, except most investors will get loans and have a mortgage they have to pay as well.

If you were to get a $120,000 mortgage, which would be the amount if you put 20% down on a $150,000 house, your payment would be $608 a month. That is on a 30 year, 4.5% rate mortgage. Now, your profit is only $217 a month, which is okay, but not amazing. You can see how the 1% rule may be the bare minimum needed to make money on a rental property.

Why is the 1% rule not always correct?

The numbers I used in the above scenario were made up by me. The tricky thing with rental properties is that the numbers change in every market and for every person. This is why I do not like rules like the 1% rule or 50% rule because it may work for some people but not others. Here is an example of how different the returns can be:

Here are what the expenses could be on a rental property that rents for $1,500 a month in a different market:

- Property taxes: $70 a month

- Insurance: $60 a month

- Property management: $120 a month

- Possible maintenance: $150 a month

- Possible vacancies: $75 a month

Now the expenses are $475 a month instead of $675! The profit would be $1,025 with no loan and $417 a month with a loan. This looks more like the type of rental property I would want to buy! As you can see, the returns are much different based on the property taxes and the insurance. There is more to consider.

How do maintenance and vacancies affect the returns?

Not only do the taxes and insurance affect the returns, but the maintenance and vacancies will also affect the returns. Some houses will need more maintenance than others, and some houses will have more vacancies than others.

When you own rental properties, there will be problems that occur. The houses are not going to be rented all year round, every year, without any work needing to be done. You have to account for vacancies that will occur and some maintenance that will be needed.

Houses that are recently remodeled will have less maintenance than houses that are 100 years old and will need major updates soon. When I use my cash flow calculator, I have a number of different amounts I use for maintenance allowances based on the age and the condition.

You may want to account for 5% of the rents on some houses for maintenance or 20% based on the condition. That could mean $75 to $300 a month. The same goes for vacancies. Some areas have higher vacancies than others, and certain types of properties have different vacancy rates.

How can the type of home and the area affect the return?

If you have properties that are in areas with very high vacancies, you need to account for that. Some types of properties will have different vacancy rates. If you own a $300,000 home that is in perfect shape and take your time finding the perfect tenant, you may be able to get that tenant to stay for years. There is a decent chance they will take care of the property as well.

If you own a $20,000 property in an area with very high vacancy rates, abandoned homes, and a decreasing population, there is a chance you won’t be able to rent out that property! It may be vacant for months, and when you do get it rented out, the tenant may be more likely to cause damage, stop paying rent, or leave early.

You will also find that the vacancy and maintenance numbers will change based on if the property is a single-family home or an apartment in a 400-unit building. The 1% rule does not account for any of these variables, and that is why I do not like to rely on rules. Every property, every owner, and every area is very different.

If you are buying commercial properties, that is something completely different because the tenants may pay all of the expenses! A .7% rule may be great for investors in that sector.

What can the 1% rule in real estate investing tell us?

The 1% rule can be useful if you know your market well. However, you may not want the 1% rule. You may want the 2% rule in some areas with low-priced properties, or you may be okay with the .8% rule in another area with low taxes and more vacancies. You don’t have to go by the 1% rule, but you can come up with a rule that works for you.

Personally, I like to write out all the returns on every property and not rely on rules.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.