How to Retire Early with Rental Properties

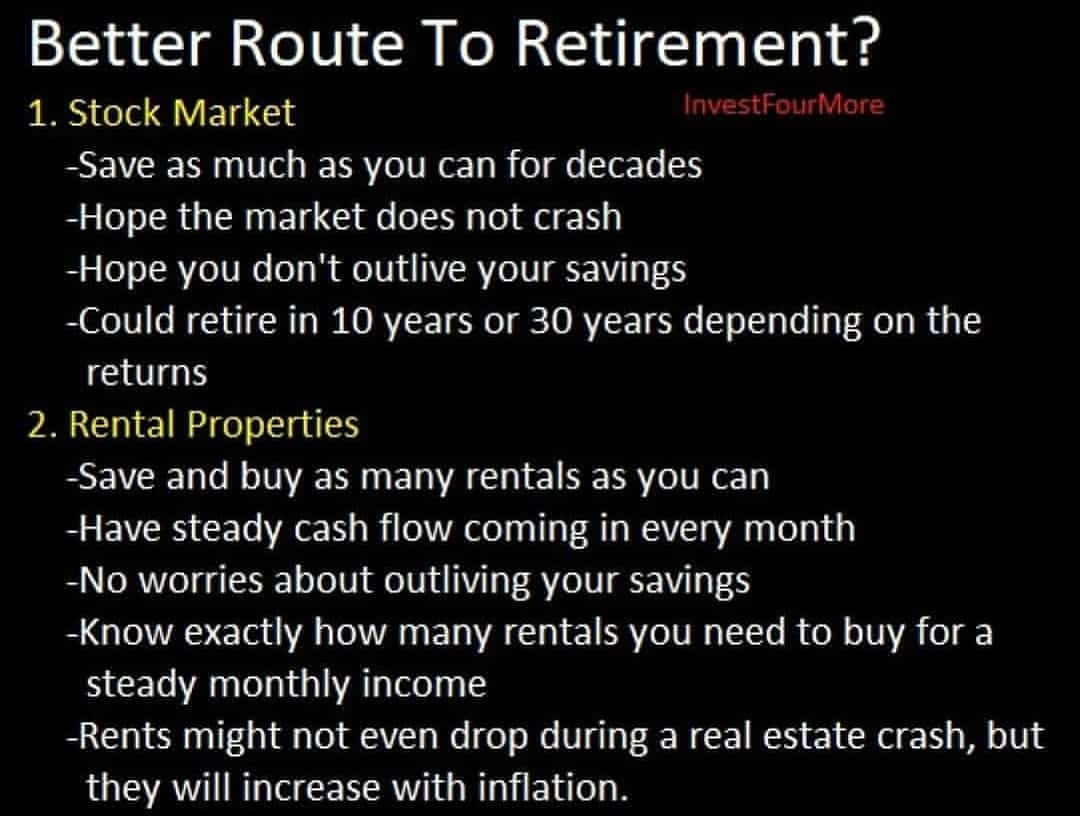

We have all been told to go to college, get a good job, invest money in the stock market, and retire at age 65. The stock market is said to be the safest and fastest way to retire early. There are advertisements all over television, the radio, and online. The retirement calculators tell us how much to save based on how long we want to live. The calculator is scary because if you live too long, you run out of money! For most of us to make money last in retirement, we have to be frugal and spend less money than we did before we retire. I never liked the idea of guessing about my retirement and hoping I don’t live too long. I don’t want to be one of those elderly people who have to be supported by their children, or worse, have to go back to work.

I have more than a few issues with this plan, and I choose to do something completely different for my retirement. The key to early retirement for me is investing in rental properties or another income-producing investment. I am 40 with three kids and a beautiful wife, and I could retire now if I wanted to. I could have retired a few years ago thanks to the cash flow my rentals provide. Unfortunately for me, I have expensive tastes and love my work (house flipping, real estate broker, blogger)! I will probably never retire, but I could if I wanted to. I have made a lot of money, but there is still no way I could have produced the results I have up to now by investing in the stock market or mutual funds or bonds. Real estate was the fastest way for me to build a passive income that comes in whether I work or not!

What is wrong with the stock market retirement model?

Many people make a lot of money from the stock market. I am not bashing the stock market or saying it is a horrible investment, but the way it is advertised as a route to retirement for most people is flawed. We are supposed to invest continually into the market, hope the market goes up, hope we have enough money to live on, and hope we don’t live too long.

Make money –> Invest in Stocks, bonds, mutual funds –> Investment increases –> Start taking money out when you have enough

Once you start taking money out of your investment accounts, the balances decrease because there is usually not enough money to sustain your living expenses just from the return you are making. But what if you have millions of dollars in the investment accounts?

If you have $2,000,000 in your investment account and make a 7% return, you can take out $140,000 a year. That is awesome, right? Except you might be paying taxes on that money depending on what type of account you have and maybe 30 years in the future when you are taking this money out. The bad news is that inflation makes that money worth much less than it is worth now.

That $140,000 is only worth $67,000 30 years from now. That may not be enough money to live on per year depending on what your lifestyle is like.

The other problem is that most financial advisers suggest being very conservative when you near retirement age. You don’t want to see your $2,000,000 turn into $1,000,000 if the stock market crashes right before retirement, so they suggest investing in bonds that make much less than 7%. If you follow their advice, you aren’t making that $140,000 per year. You’re maybe making $100,000 per year, and after inflation, you are only making $47,000 a year and maybe paying taxes on it.

Now you see why the retirement account starts losing value very quickly, and every year in retirement, you get a little closer to running out of money.

How much money do you need to save to retire?

The other issue that most people run into is saving enough to grow their investment to $2,000,000. That is not an easy task as it takes 30 years of saving $20,000 a year with a 7% compounding interest rate. You might make more than 7%, but you also might make less or even lose money, which really sucks.

How many people are actually able to save that $20,000 a year? How many of them are able to get that 7% every single year without any setbacks? That also assumes you are paying no fees on your investment either.

The cool thing about rental properties is that you can invest much less money, get better returns, have more stable returns, and not eat into your investment balance in retirement. You can also create the income you need to retire much sooner, and they are a hedge against inflation!

Does all this sound too good to be true? Well for me it did, but I learned as much as I could and invested in rentals, and they have been one of the best things I have ever done in my life. Besides personal stuff like having kids, getting married, all that…

What is the catch? There is none! It is easy! Just kidding. Investing in rental properties is much harder than investing in stocks, bonds, or mutual funds. It takes more research, more time, more guts, and not every market has amazing rentals. But, if you are willing to put in a little bit of work, they can be an amazing investment.

Early retirement with rentals thanks to cash flow

One of the biggest problems I have with conventional wisdom regarding retirement plans is we have to guess when we are going to die. We use a retirement calculator to find out how much money we will need in retirement and then put an age in the equation to make sure we don’t run out of money. How depressing. No one wants to play the guessing game for when they will die.

This is one of the main reasons I love investing in rental properties. I can use the cash flow from rental properties for retirement without eating away the principal balance.

If I have $5,000 a month coming in from rental properties, that $5,000 is going to keep coming in every month until I sell the homes. It may even increase as rents go up and my mortgage balances go down. No more calculating when you are going to die and worrying about if you will outlive your savings.

You will have income by doing minimal or no work every year for the rest of your life. You can hire a property manager and never worry about the repairs or vacancies and retire in style. Many investors end up quitting their day jobs and concentrating on investing in rental properties at a very young age. They buy a couple of properties, realize how great of an investment it is, and they get hooked.

What is cash flow?

Cash flow is the money you make from rental properties after paying all the expenses. You do not buy rentals so that one day they will be paid off and finally make money. At least I don’t. I buy rentals that make money now. Here is an example:

- Rent: $1,500 a month

- Property taxes: $150 a month

- Insurance: $75 a month

- Maintenance: $150 a month

- Vacancies: $75 a month

- Property management: $150 a month

The cash flow is $900 a month! That is pretty awesome, right? Yes and no. That is assuming you paid all cash for a property. And to buy a rental that makes $1,500 a month in rent, you may have to pay from $100,000 to $250,000 depending on what market you are in. If you pay $250,000 for the rental, that is a 4% return, and if you pay $100,000 for the rental, that is a 10% return. Not horrible, but not amazing, and I like amazing.

You might also notice we included maintenance and vacancies in the expenses. When you own rental properties, you will have times when the properties are vacant or need work. You cannot assume everything will always go perfectly.

Using leverage to increase returns

Leverage basically means you are borrowing money in relation to real estate. If you get a loan when buying rentals, you only have to put 20% or 25% down, not the entire purchase price. Now, instead of spending $100,000 or $250,000 in cash to buy that rental, you are spending $20,000 or $50,000.

It is true that you will now have a mortgage payment, but the returns actually increase with leverage when you buy the right properties. Your payment would be about $400 a month with the $80,000 loan or $1,000 a month with the $200,000 loan. Now you are making from $500 to $1000 a month with the rental property. That doesn’t seem like much, but that is a 30% return with the $100,000 property! With the $250,000 property, not so much.

This shows why it is so important to buy good rentals and not just any property you find for sale. Honestly, it will be really hard to find a property for sale for $100,000 that rents for $1,500, but they do exist! I have bought a few commercial rentals with those numbers.

You also may be paying more than $20,000 to get that $100,000 rental because there will be closing costs, some repairs might be needed, and it may be vacant for a little while. You will probably spend at least $30,000. Without writing a book, which I have done 8 times, the truth is a good rental will make 10 to 15 percent from the cash flow alone.

Other advantages of rental properties

The really cool thing about rentals is that the longer you own them, the more awesome they become. Not only are you making a few hundred dollars a month on each one (assuming you buy single-family rentals), but you are also paying the loan down, have tax advantages, properties can appreciate, you can buy below market, and they are a hedge against inflation.

Mortgage paydown

Each month you are paying at least $100 of the mortgage off.

Tax advantages

Rental properties also have some amazing tax advantages. You can depreciate the property, deduct the interest as an expense, and even sell tax-free when you exchange the property.

Appreciation

I do not count on appreciation, but it does happen, and it happened for me in a big way. I live in Colorado, and I am currently selling the first property that I bought for $97,000 in 2010 for $275,000! I would never expect that much appreciation, but it does happen.

Buy below market value

One amazing thing about real estate is you can buy a house worth $150,000 for $100,000. Again, this is not easy, but it is possible. I got awesome deals on all of my rentals. I bought my first rental for $97,000, but it was worth closer to $130,000 at the time.

Inflation

We saw earlier how much inflation destroyed the value of money when you invest in the stock market. Rentals are a natural hedge against inflation because rents go up with inflation. Your mortgage payment will most likely stay the same or close to it, but rents go up, which means your returns increase over time. Eventually, your loans get paid off, which increases your returns even more! Instead of worrying about time destroying the value of your money, you can be happy that time is increasing your investment returns!

Why are rentals a faster option?

It takes money and discipline to find and buy your first investment property and create passive income. If you had that same amount of money, ($600,000 or $20,000 per year for 30 years) you could buy from 10 to 20 rentals in the same amount of time. Depending on how much you paid for the properties and the cash flow, you would be making from $50,000 a year to $200,000 a year without eating into the principal investment or counting loan pay down, appreciation, tax advantages, or buying below market value. You are making more money per year, which means you can retire faster with more confidence.

But how did I create enough passive income to retire early?

We went over the basic concept of rentals, but there are many more tricks and techniques you can use to increase your returns even more.

- Refinancing. I refinanced my rentals and took cash out to buy faster. I own 20 rentals now that bring in $13,000 a month in income. I bought those rentals in less than 10 years, including a 68k square foot strip mall, because I took cash out to grow faster.

- Different types of rentals. I started with single-family rentals but moved on to commercial rentals when prices got too high to cash flow in Colorado with residential rentals. Commercial properties are riskier but amazing.

- I make a lot of money. Real estate has been good to me as a house flipper and a real estate agent. I make a lot of money that I can invest in rentals. I have been able to invest much more than $20,000 a year.

- You don’t always have to put 20% down. I have bought a number of properties with less money down.

What are the cons of rentals?

I love rental properties, but there are some downsides to using them as a retirement vehicle.

Not liquid

If you need to sell a rental or take money out of the property, it is not easy to do. You will need to refinance the property or sell it. Each option can take at least a few weeks or longer. Make sure you are not counting on getting money out of a property fast.

Not every market has great rentals

I bought single-family rentals in Colorado from 2010 to 2015. That was a great time to buy, but prices became too high to cash flow after 2015. I was going to invest in another market, but then I discovered commercial real estate. I have bought 7 commercial rentals in Colorado that cash flow in the last few years. If your area has very high prices, it will be tough to make money with rentals. You may need to look at different markets or niches.

It takes work

Finding great deals on rentals, analyzing the numbers, finding property managers, agents, and contractors is not easy. However, most things that are worthwhile in life are not easy. If you want to retire early, it is going to take work no matter what you do.

I don’t want to wait to retire until I am 65

I don’t want to retire at 65 because I want to live life now. I may work that long, but I don’t want to have to work that long. With an average income invested in the stock market or a mutual fund, you are not going to be able to retire at 45 unless you make huge sacrifices. To retire early, you have to start saving at 15 or live extremely frugal before and after retirement. Most of you reading this are probably past the age of 15! In order to retire early without living frugal, you need to change the way you invest or get a higher-paying job. I like the idea of having a high paying job and investing wiser.

Conclusion

Rental properties are one of the best tools for early retirement because of the passive income they provide. That money will increase as I get older. I could retire now, but I have too much fun with real estate. If I would have used the stock market to retire, I would have $500,000 in my stock accounts. With real estate, I have multi-millions in equity and more than $100,000 a year coming in without doing any work. To me, the choice is clear.

My book Build a Rental Property Empire, goes over how to use the BRRRR method to retire early with rentals. It covers how to find deals, finance rentals, manage them, and much more! It is available as a paperback and ebook on Amazon or as an audiobook on Audible.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

Great stuff as always, Mark! I’m with you 💯 on this article!

Thanks DJ!

Thank you, Mark. I really appreciate the article. Reaffirms why I begin real estate years ago.

Glad you like it!