What Dave Ramsey Gets Wrong About Real Estate Investing

Dave Ramsey has gotten many people out of debt and helped many others balance their budgets and live within their means. However, Dave has some interesting advice when it comes to real estate investing. He says that you should only invest in rental properties when you can pay cash for them and only comprise 5% of your liquid net worth. That means if you have $2,000,000, you can buy a $100,000 rental property. Dave also thinks you should only flip houses if you can pay cash for everything. I understand why Dave says this because his entire image is based on no debt, but his rules for real estate investing make it almost impossible for someone who is not already very wealthy to ever invest in rentals or flips. As a successful real estate investor, it is very easy for me to tell you what Dave Ramsey gets wrong about real estate investing.

Is debt bad? Should we avoid it at all costs? I agree that many people let debt get out of control and it can make it almost impossible for them to get ahead, but some people are able to use debt to their advantage and build wealth with it. Even Mark Zuckerberg used debt to buy a house to live in after he was a billionaire. Why? He said he could put that money to better use than sitting in a house. I agree with Mark and many others who use debt in a good way to build wealth.

What Dave Ramsey gets wrong about rental properties

When I talk about the rules that Dave Ramsey lays out, many people do not believe me. They ask for a source, and Dave gives us one directly from his blog post: How to Invest In Real Estate. He clearly lays out the rules for when it is okay to invest in rental properties:

Step 1: Pay in cash. When you pay for an investment property with cash, you save thousands of dollars in interest. Plus, you won’t ever have to worry about foreclosure. Creating unnecessary risk by financing an investment is just a bad idea. And one of the best perks of paying cash? You actually get to keep the money you make from rent payments!

Step 2: Diversify. As a rule of thumb, I recommend having only 5% of your net worth tied up in real estate investments. If your whole net worth is invested in real estate, any fluctuation in the market could make you panic. It’s important to keep your nest egg diversified to minimize risk. Mutual funds invested through your 401(k), Roth IRA and other retirement savings accounts should be the foundation of your wealth-building strategy.”

Dave is very clear on his show and in other articles that no one should be buying rentals until their house is paid off, their college fund is well on its way, and their retirement is moving along with mutual funds.

Why does Dave Ramsey think you should not use debt?

Dave refers to his own bankruptcy many times on his show and in his teachings. He blames real estate for his going broke, and not just real estate, but using debt with real estate. While it may be true that debt and real estate sunk Ramsey, there are some things to consider—such as the fact it would be basically impossible for any investor to invest now how he did back in the 1980s before going bankrupt.

I do not have actual knowledge of exactly how Dave Ramsey was investing, but he does admit over and over he had 90-day loans. A 90-day loan means that 90 days after you take the loan out, the bank can call it due. It is very tough for anyone to get a 90-day loan, and they are almost unheard of in real estate today. What Dave was doing was extremely risky, and using 90-day loans means he may have to pay off a lot of debt at any time.

I flipped 26 houses last year and 26 the year before that. I use plenty of debt to flip that many houses, and while loans for house flips are typically riskier than other types of real estate loans, even they have a 1-year term. Most loans for residential rental properties have a 15- or 30-year term. Some loans for commercial rentals can have much shorter terms: 10 years, 5 years, or even 3, but nothing close to 90 days.

How did Dave Ramsey go bankrupt?

Dave has said he had a 4 million dollar real estate portfolio and a net worth of one million dollars when he was 26. Then the banks called his 90-day loans due. He could not pay them off, and he went bankrupt. There is another story surrounding Ramsey’s bankruptcy, but to be clear, this is all information taken from a Bigger Pockets forum post. I cannot prove or disprove if this is what really happened.

“Here is how the investors made the big bucks. First find a totally worthless rental building, the bigger the better. Buy it for what it was worth (just about nothing). Next ,fix the place just enough to make it habitable.

Next, sign leases with folk who were at least breathing, make the rent as high as believable. Next, go to a lender who was not being properly regulated, was allowed to lend money based on the new value of the building which was now based on a totally rented fully leased building.

Easy slam dunk deal. The investor is holding $100’s of thousand of borrowed tax-free money, and the limited partners paid the mortgage plus the other expenses involved in the building. The professionals got a huge write off by owning the losses of the building without being on the mortgage docs or owning the building.

The investor had easy management. He did not worry about collecting rent, or upkeep, as the limited partners paid the freight.

The tenants never complained as most did not pay the rent anyway. But Uncle Sam threw a monkey wrench into the deal. The new tax code disallowed losses from real estate for these professionals who earned above $125k, and that is all of them.

The limited partners stopped paying the mortgage and walked away free. My friend had 2.6 million dollars of mortgages to pay on negative-cash-flow buildings. He, of course, also ran away with his credit totally destroyed forever, and the lenders mostly failed.

This, my friends, was called the S+L crisis.”

Here is the post this was taken from https://www.biggerpockets.com/forums/79/topics/37369-dave-ramsey-s-real-estate-story-

Does Ramsey’s story apply to today’s investor?

I think even Dave would admit that his bankruptcy was something that would be very hard for anyone to duplicate in today’s market. There are many more rules and regulations in regard to financing and banks. There would be almost no investors buying long-term rentals with 90-day loans.

While I can understand why Dave says don’t use debt, using his life as an example does not make sense. I would want to know how an investor can lose it all with today’s loans and regulations. I am not saying you can’t go bankrupt, but we need to compare apples to apples.

What are the 7 baby steps?

Dave Ramsey created 7 baby steps to get out of debt and build wealth…well mostly gets out of debt. I agree that saving and being smart with your money is important, and it is almost impossible to get ahead in life without doing those things. I think he takes it a little too far. Here are the baby steps:

- BABY STEP 1

Save $1,000 for your starter emergency fund.

- BABY STEP 2

Pay off all debt (except the house) using the debt snowball.

- BABY STEP 3

Save 3–6 months of expenses in a fully-funded emergency fund.

- BABY STEP 4

Invest 15% of your household income in retirement.

- BABY STEP 5

Save for your children’s college fund.

- BABY STEP 6

Pay off your home early.

- BABY STEP 7

Build wealth and give.

According to Dave, you should not be investing in real estate until step 7 when everything else is paid off. You are saving for retirement and college, and you have an emergency fund.

How has debt helped me

Dave Ramsey’s entire image is based on no debt. It would be weird for him to say it is okay to use debt when investing in real estate, but that does not mean he is right. I have used debt to buy 25 rentals, including a 68,000-square-foot strip mall. Debt has done incredible things for me, and if I would have followed Dave Ramsey’s rules, I still would not have bought my first rental. Rental properties have done amazingly well for me.

- I have bought 25 rentals and own 21 currently totaling about 118,000 square feet

- I bought 16 residential rentals from 2010 to 2015

- I bought 9 commercial rentals from 2016 to 2019

- I have built around $5 million in net worth from owning rentals alone.

- That net worth came from getting great deals, using leverage (debt), refinancing properties (more debt), and cash flow.

- I have about $15,000 in passive income coming in from my rentals after all expenses.

I bought my first rental after taking cash out of my personal house by refinancing it. You could say I got started the exact opposite way that Dave Ramsey suggests. Instead of paying off my home, I got a bigger loan on my home!

Was that smart? I guess it depends on who you ask, but it created a multimillion-dollar real estate portfolio for me. If I had invested the way Dave Ramsey suggests, I may have about one million in retirement and college savings. I may or may not have a paid-off house. I know I would not have the cars I have now (Lamborghini, Aston Martin, Porsche, Lotus, Supra, Mustang, Audi).

Dave Ramsey’s teachings can help people, but they are not for everyone. He is really good at getting people to save and reduce debt. I like to think I am really good at building wealth and creating passive income. I like the way I invest and build better because I see it as faster and much more fun! However, it also may seem riskier to others.

Debt, if used in the right way, can be a fantastic way to get ahead in life.

The video below goes over how to finance rentals:

Do you make more money with loans?

Dave suggests that whenever you buy a rental property, it should be purchased with cash, and you should get an awesome deal on it. I completely agree about getting an awesome deal on the property. He even suggests using the 70% rule to buy rentals, which is often how house flippers decide whether a deal is good enough to flip or not. He also suggests people have an emergency fund, which I agree with as well. So, what would it look like if you bought a rental property with debt but had an emergency fund and bought it at 70% of the after repaired value minus any repairs needed?

- Value of the property after repairs $200,000

- The property needs $15,000 in repairs

- That means you would buy the property for $125,000 ($200,000 x.7 minus $15,000)

- If you put 20% down, which most banks will require on an investment property, your loan will be $100,000

- You will have some closing costs and other expenses, so you probably spent about $45,000 buying the property

You now have a house worth $200,000 that you bought with $45,000 cash, but what will it make each month with leverage?

- Rent would be about $1,500 a month (this could vary greatly based on the market)

- The mortgage payment would be $500 on a 30-year loan at 4.5% interest

- You would have taxes and insurance which could be $250 a month

- You need to account for vacancies and maintenance which could be $300 a month

- You want a property manager who is $150 a month

You are making $300 a month after paying all the expenses. Not bad, but think how much you would make if you paid all cash!

- The only expense you would not have if you paid cash is the mortgage payment, which would be $500 a month

- It would take $145,000 in cash to buy the house outright and make the repairs.

With the loan, you are making $300 a month or $3,600 a year, which is 8% on your money after spending $45,000 to buy and fix up the place. With cash, you are making $800 a month or $96,000 a year which is 6.6% on your money.

Yes, you make a better return by getting a loan, and you have other advantages as well.

- Every year, you pay down about $2,000 in principle on the loan, which is another 4%.

- Every year, the interest on the loan is deductible, which could equal another $2,000 a year or another 4%

With the loan, you are making 16% on your money versus only 6.6% with cash, but that is not all.

The video below goes over using cash versus loans as well:

Why buying more properties is better

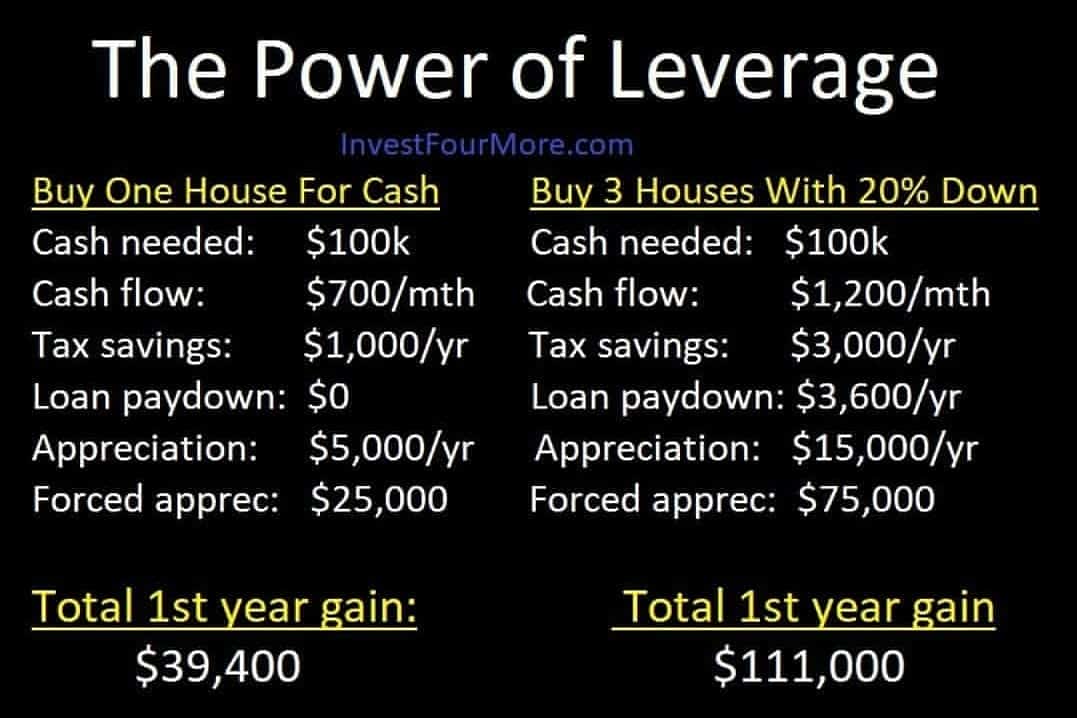

The other big advantage of using loans is you can buy more rentals. If it takes $145,000 to buy one with cash but only $45,000 to buy one with a loan, you can buy three properties with a loan to every one with cash.

We already saw how loans offer a better return on your cash. In reality, I want properties that make more than $300 a month, and my rentals do make more than that. The taxes and insurance on my rentals are less than the numbers I used, and the maintenance and vacancies are less as well, but I wanted to be conservative with my numbers. The more cash flow you make on rentals, the more advantageous it becomes to use loans.

When you buy more properties, there are even more advantages!

- You triple the equity from getting a good deal. With the example above, you spent $145,000 to get a $200,000 property. That is a $55,000 gain in equity.

- If you buy three properties, that is a $165,000 gain in equity versus a $55,000 gain in equity.

- You also get to depreciate properties on your taxes. That means you can deduct a certain amount every year even if you make money. On this property, that amount might be $4,500 a year you can deduct, which could save another $2,000 or more on your taxes.

- If you have three properties, you would be saving $6,000 a year versus only $2,000 with one.

- You are more diversified with three properties versus one. If one tenant moves out, you don’t lose all your rental income!

- If housing prices increase, you have three times the increase with loans. If that property goes up in value 10%, you will make $20,000 with one property or $60,000 with three.

You will literally make more than $100,000 more in a couple of years using loans instead of cash.

What about risk?

A lot of people will say the risk of loans is just not worth it, but are they really that risky? You have three properties that are worth $200,000 with $100,000 loans. Housing prices would have to decrease 50% for the property to be worth less than the loan amount.

If you can’t rent out the property for a while or have a tenant move out, you have the emergency fund that should be able to handle those expenses, and you are accounting for those expenses in the returns you calculated as well.

If something does go wrong and you own a house outright, it is not easy to get that money out. You would have to sell or refinance the property, which can take months. Having the house paid off is not that huge of an advantage except that your expenses are $500 a month lower.

Almost everyone who is buying their first rental will be able to get a 30-year fixed-rate loan that will not be able to be called due before that 30 years is up. What happened to Dave could not happen to you.

To me, it is not that risky to have loans.

Conclusion

Yes, it makes sense for Dave to promote no debt on everything because that is his marketing message. However, I do not think that rule is the best way to go on rental properties. You make more money every month and more money with buying below market value and appreciation upside. There are better tax advantages and the risk is not very high. Before you take Dave’s advice on rental properties, think about if that is the right advice for you.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

I am not sure if I understand how to do this.

which part?