Is the House you Live in an Asset or Liability?

Assets and liabilities have had their place in the financial world for centuries. Over the last couple of decades, there has been some disagreement over what an asset is based on the book by Robert Kiyosaki: Rich Dad Poor Dad. In that book, Kiyosaki defines an asset as: “Something that puts money in your pocket”. What he means is that only something that pays you every month can be considered an asset. This is the definition that Robert uses but it is much different than the definition that accountants, bankers, lawyers, and most business people have used for centuries. To go along with this definition, Kiyosaki says that the house you live in is not an asset because it doesn’t put money in your pocket. Is he right, or is he confusing people?

What Kiyosaki says about assets and liabilities

This is directly from Robert’s website:

“The simple definition of an asset is something that puts money in your pocket. Many so-called experts on money and accountants will have a much different definition that involves complex mathematics, but the reality is that unless something is putting money in your pocket, it’s not an asset.

There are many things that can be considered assets. These include things like investment real estate, a business, products like books or art, or dividends from stock and bond investments.”

He says that real estate that is rented out is an asset because it brings in cash flow, but the house you live in is a liability because it does not bring in any cash flow.

“Using this simple and practical definition, your home is a liability because it takes money out of your pocket each month in the form of a mortgage, taxes, insurance, and maintenance costs. It does not put money in your pocket. Only if you’re able to sell it at a profit does it become an asset. Many people impacted by the Great Recession discovered that their house was a liability when they were foreclosed, sold on a short sale, or sold at a loss.”

I go over my opinion of his book Rich Dad Poor Dad here.

What do bankers, accountants, lawyers, and most business people think an asset is?

The traditional definition of an asset is:

“An asset is anything that has current or future economic value to a business. Essentially, for businesses, assets include everything controlled and owned by the company that’s currently valuable or could provide monetary benefit in the future. Examples include patents, machinery, and investments”

https://www.netsuite.com/portal/resource/articles/accounting/asset.shtml

A liability is:

“A liability is something a person or company owes, usually a sum of money. Liabilities are settled over time through the transfer of economic benefits including money, goods, or services.”

https://www.investopedia.com/terms/l/liability.asp

As you can see the traditional definitions are much different from what Kiyosaki claims the real definitions are. According to the accounting definitions the house you live in, or any real estate is an asset and the loan against it is the liability. It does not matter if the house makes money or loses money or goes up in value or down in value. If it has value it is an asset.

Why is Kiyosaki’s definition of an asset and liability confusing?

Robert says that the house you live in is not an asset because it does not bring in money. However, if you were to sell that house and make money, it would then become an asset. My problem with this, is that once you sell the house how is it now an asset when you no longer own it?

Has it become an asset for the new person, or did it switch from being a liability when you owned it to then being an asset when you owned it, but you don’t own it anymore so what is the point?

He also says that art and stocks and bonds are assets because they pay dividends (art doesn’t but he still lists it as an asset). He also is pushing gold, silver, and Bitcoin constantly. I have not heard him say those are assets, but based on his definition they would not be since they do not produce cash flow. What else is really confusing is his wife lists these as the five major asset classes on Robert’s website:

- Paper

- Businesses

- Commodities

- Cryptocurrencies

- Real Estate

Many of these “assets” do not produce cash flow and she even says real estate that produces capital gains is an asset. It would seem they have their stories a little crossed.

https://www.richdad.com/asset-class

Why is the Rich Dad definition of an asset dangerous?

I am a real estate investor and I also am an influencer like Robert Kiyosaki. I have a lot of people commenting on my social media, videos, and blog. When I talk about assets verse liabilities the conversations can get very heated! People get mad at me when I say an asset has value and that it does not matter if it makes money or not. They go on to tell me why the house you live in is bad, and why you should only buy rentals, and why I am wrong.

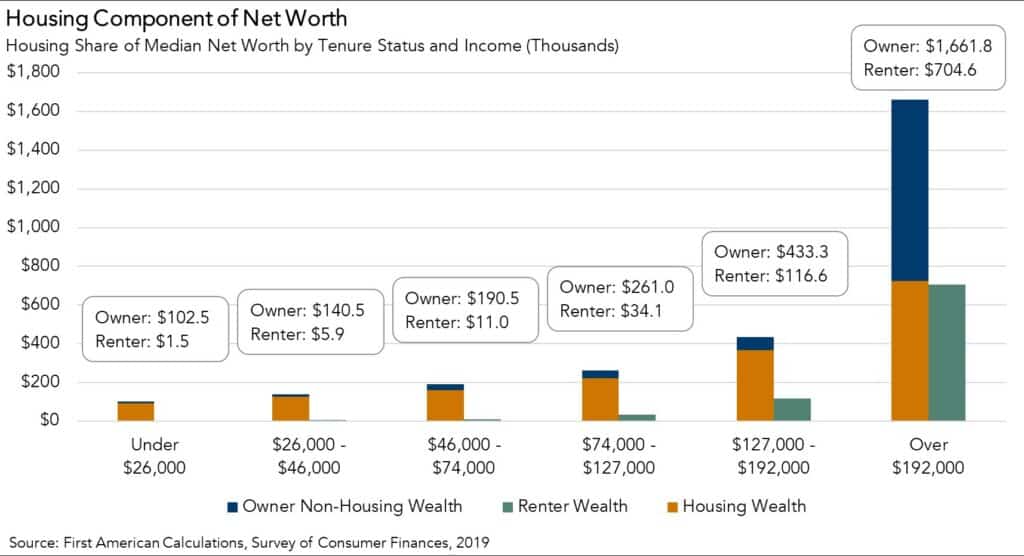

The problem with this is that the home you live in is the best investment most people will ever make. Statistics show that for people who make less than $100k a year, the house they live in creates 90% of their wealth.

For those who make the least amount of money, owning a home or not is the biggest indicator of how much wealth they will have. Homeowners have $102,500 in net worth and renters have $1,500 in net worth.

Even though Robert does not say buying a house to live in is bad and you should never do it, his definition of an asset has caused many to think that. He says the traditional definition is confusing with complicated math. The traditional definition is very simple while Robert’s is very confusing. Especially when his wife contradicts him on his website.

My personal homes made me hundreds of thousands of dollars tax-free and allowed me to buy my first investment properties. Real estate has also allowed me to fulfill my dreams of owning a few, well 10 exotic cars including 2 Lamborghinis. Yes, those are assets too. It is so much easier to just call an asset an asset. An asset does not have to be a good investment and it can even decrease in value. That is why cars are often called depreciating assets.

“But Robert uses the word asset in a different way”

I also hear people say there can be two or more definitions of an asset. They say that Robert is not talking about the accounting version of an asset, but the version where an asset means something is good or beneficial. “Carrie is an asset to the team”. If that is the case why does he say that buying a house to live in can be smart and beneficial to people but the house is still not an asset?

To my previous point, buying the house you live in is the number one investment for most Americans unless you are one in the very top wealth class. If he was saying that a house is not beneficial he would be wrong for most people. Even though a house does cost money to own, in the long run, it is much better than renting and having nothing to show for your money. Investing is good too, but buying a house does not stop you from investing either.

Does a house put money in your pocket?

The main argument that Robert uses to say a house is a liability and not an asset is that it does not put money in your pocket. Even if we accept his definition of an asset, is it correct to say that a house you live in does not put money in your pocket? I think buying makes you much more money than renting and the house you live in does put money in your pocket as well.

The argument he makes is that you must pay the mortgage, property taxes, utilities, insurance, HOA, and make repairs on a home which all costs you money. It is true that a house costs you money and almost all investments will cost you money either upfront when you buy them or over time when you maintain them.

The difference with a house is that the alternative is renting and rent is usually more expensive than the mortgage on a home. Even if the other expenses add up to be more than the rent, over time the rent will keep going up while the mortgage is usually locked, at least for people in the US. You probably have heard how a mortgage might cost you $650,000 over 30 years but they never tell you what rent would cost you over that time if you never bought. The rent after adjusting for inflation will be much more and you have nothing to show for it.

Not only is the mortgage locked in, but you are paying down the principal of that mortgage and if you don’t itemize your taxes, get some amazing tax benefits from the owner as well since the interest, property taxes, and some other expenses can be deductible as well. We have not even talked about the value of the home increasing. Most people will use a loan when they buy which they put less money down than the home costs and if the home goes up in value by 5 to 10 percent, the return on investment might go up 50 to 100 percent!

When you make repairs or improve a house that is not lost money. If you make the right improvements it will add value to the home and make it worth more in the long run. Over time, houses also gain equity through appreciation and loan paydown, which creates equity. That equity can be used to take money out of the home to invest (this is what I did) or pay down other debts. Renters will never have access to that equity and that is why they have so much less wealth than owners. In my opinion, even according to Roberts’s definition, a house is an asset because it does put money in your pocket.

The video below goes over the numbers in detail on owning verse renting.

Will buying a house to live in make it harder to invest?

One more argument against buying a house to live in that hear people use when defending Robert is that it is better to invest in a rental first, and then buy a house to live in later. This can be true in some cases where you might have a very cheap living situation and you can save a ton of money to invest. However, if you are paying rent and have to pay to live somewhere, it is usually better to own even when your main goal is to invest in rentals.

When looking to buy an investment property one of the biggest roadblocks is getting a new loan. One of the main factors a lender will look at is the debt-to-income ratio of the buyer. When you rent or buy, the loan or rent will count against your debt-to-income ratio. In fact, every loan application includes a box that asks if the borrower rents or owns their home. Banks feel more comfortable loaning money to people who own their home.

If you can buy a house to live in and get a great deal on it, that can create instant equity which allows you to pull money out of the house to invest in other properties. That is exactly what I did when I bought my second owner-occupied house. I refinanced the home about a year after I bought it, and was able to take out $50,000 that I could use to buy my first rental properties.

Conclusion

Robert Kiyosaki’s definition of assets and liabilities has confused many people and caused them not to buy a house to live in, even if that was not his intention. I think it is best to use the terms the way they have been used for centuries to avoid confusion, especially when dealing with banks or accountants. Even, using the definition Robert uses, I still believe buying a house to live in is one of the best investments anyone can make and the stats show that as well.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

Thanks Mark, you have very well explained this topic.

ThankS!