What is the Best Way to Invest in Real Estate?

There are many ways to invest in real estate with fix-and-flips, long-term rentals, vacation rentals, REITs, short-term rentals, crowdfunding, nonperforming loans, wholesaling, and your personal residence. If you are a beginner and learning about the business, it is best to expose yourself to the different ways to invest so that you can pick the best one to start with.

I invest in real estate with long-term rentals and house flips, although I also own a real estate brokerage. I love long-term rentals because they offer great returns which continue to pay you as long as you own the property. I also love to flip houses because of the money you can make, and it is a lot of fun to transform old houses into something new.

What is real estate investing?

I flip houses, but I do not consider house-flipping an investment. House flipping is more of a business or a job. Every time I sell a flip, I must work to find another one to make more money. A great real estate investment provides a great return on your money without much effort. Rentals bring me money every month without much work and without having to keep buying more rentals. I use the flipping income to buy as many rentals as I can. I still list house flipping in this article because most people consider anyone buying or selling real estate an investor.

Each way to invest in real estate has a different level of risk, return, and time commitment. Some investments in real estate are more of a full-time job than an investment like fix-and-flipping, while some investments like REITs take almost no work.

Rental properties

Long-term rental properties are my favorite way to invest in real estate. It can take a lot of cash, but the returns are incredible if you buy right and are patient. I make over 15% cash-on-cash returns on my long-term rental properties, and that does not include appreciation, equity pay-down, or tax benefits.

When you invest in real estate with long-term rentals, you must focus on cash flow. The best way to get a lot of cash flow is to buy properties at below market value, make repairs to increase value, and choose houses that will give high rent-to-purchase price ratios. It is not easy to find properties like this as it can take me months to find the right deal for a long-term rental.

Not every market has great rental properties either. I was buying many residential rentals in Colorado after the housing crash, but prices increased so much I could no longer cash flow in this area. I was going to invest in real estate in Florida until I found I could make money with commercial rentals locally.

I invest in single-family rentals because they give me better returns than multifamily. However, in different areas of the country, multifamily properties may offer better returns. Part of the reason I can get better returns on single-family houses is there are more of them. With more volume, there is a better chance I can find that great deal.

Commercial rentals are tricky. Lease terms are usually much longer with commercial properties, but it can take a very long time to find a tenant. There are many types of leases: some leases have the tenant paying for everything, including repairs and maintenance. Other leases have the owner paying for almost everything, including converting/remodeling the property to the tenant’s needs. With commercial properties, loan terms are much different with shorter terms and higher interest rates.

Below is a video of my latest commercial rental property:

House Flipping

I started to invest in real estate by flipping houses. My father has been a Realtor since 1978, and he flipped houses since I was in high school. When I started in real estate in 2001, I became a real estate agent. I loved fix-and-flips, but selling houses to strangers, I did not love so much. I am naturally an introvert, and fix-and-flips were perfect for me because I could focus on the house. I could find great deals, decide how to repair them, and sell for a profit.

On one fix-and-flip, I repaired the house myself. I installed new cabinets, counters, appliances, windows, doors, hardwood floors, and painted everything. This was one of the biggest mistakes I ever made in my real estate career! It took me 6 months to complete the repairs because I was not a contractor and I learned on the job. The biggest error in my judgment was the time it took to repair the house. My other business suffered greatly because I spent all my time working on the house.

We barely made a profit on that deal because it took me so long to complete the job. I learned never to repair houses myself! I think many first-time fix-and-flippers try to save money by making repairs themselves, and they don’t realize they are actually costing themselves money. It can cost $50 to $100 per day to hold a property that is vacant after interest, utilities, and insurance costs. It is usually much more beneficial to have a contractor do the work who will do it quickly and correctly.

I have flipped over 185 houses now, including 26 each of the last two years. House flipping is a great way to invest in real estate, but it takes a lot of work. You have to find deals, manage contractors, keep track of accounting, and get houses sold. It also takes a lot of money for down payments and repairs, although hard money can be an option to reduce the cash needed.

I have videos of almost all of my house flips on YouTube.

Wholesaling

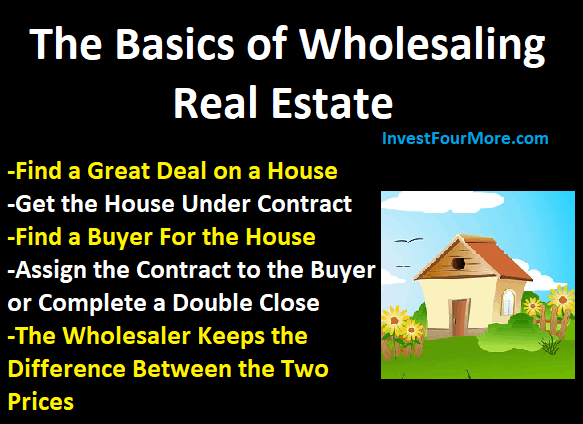

Wholesaling real estate is when an investor buys a house or gets a house under contract and they immediately sell the house to another investor without making repairs. An investor can wholesale a house without buying it by getting them under contract and then assigning that contract to another investor or completing a double close. The advantage of wholesaling is you don’t have to make repairs on a house and it is sold very quickly.

Many gurus teach wholesaling as an easy way to make millions in real estate, but it is not that easy. Wholesalers must find really good deals to be able to sell them to other investors who can still make money. Usually, wholesalers find properties through direct marketing or driving for dollars. Once the wholesaler finds a deal, they also must find a buyer for it as the houses cannot be listed on the MLS.

You can make a lot of money wholesaling, but it takes months to learn the business and find a deal. You also have to work constantly to keep the flow of deals moving.

Personal house

Your personal residence is another way to invest in real estate. Some may not consider a personal residence a way to invest in real estate because you aren’t bringing in any rent or income. I think there are definitely ways to make your personal residence a great investment. You also have to pay rent if you do not own your house, so even if you are not making money, you are saving money in most cases.

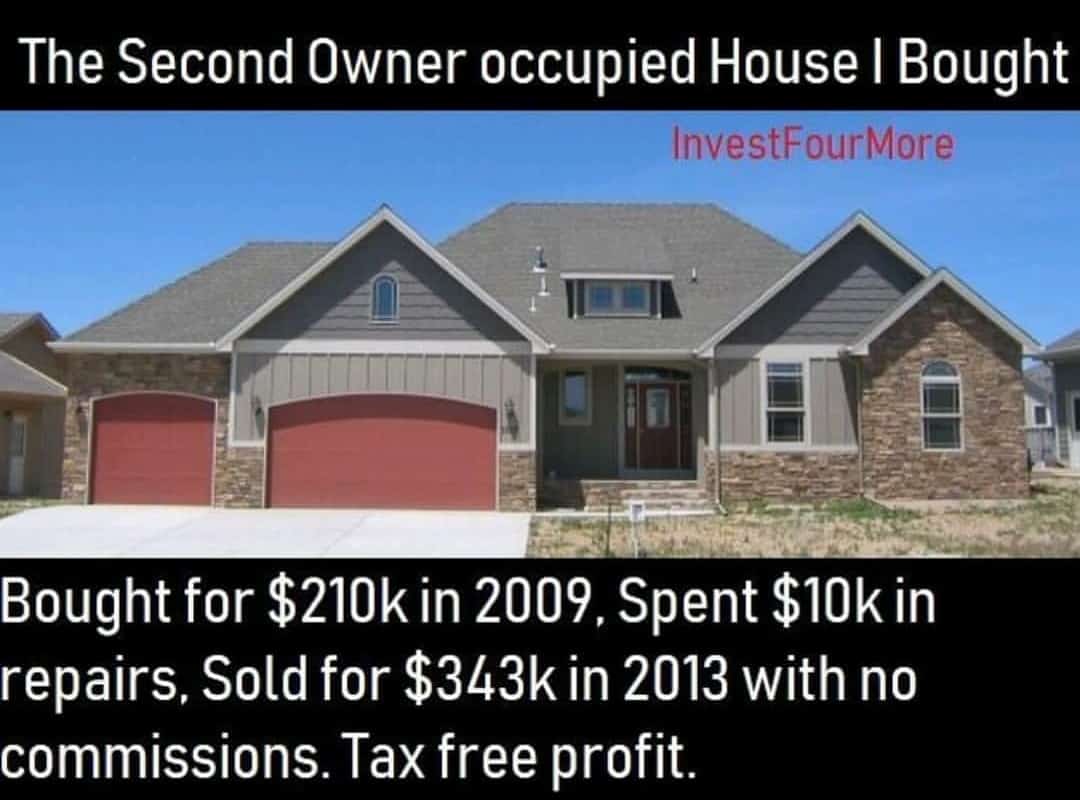

I bought the house I owned before my current house at the foreclosure sale in 2009. I sold it for $150,000 more than I bought it for because I bought it at below market value. The nice thing when you invest in real estate with your personal residence is you can make a tax-free profit if you live there for two years or more!

One of the biggest advantages of buying real estate is being able to buy below market value. You cannot do that with most investments. On every house I flip, I get a great deal, and owner-occupants can do that as well. In fact, HUD and other banks often sell their foreclosures to owner-occupants first.

It is also possible to buy a personal residence that you can turn into a rental property. This is a great way to buy a rental property with little money down. You can buy more than one property this way and build up a portfolio of rentals with small down payments.

You do not have to sell your personal house to make it a good investment either. I was able to refinance my house a short time after I bought it and take out all the money I had used to purchase it and then some. I was able to use that money to buy my first rental. Another huge advantage of buying a house that you live in is you can get loans with 3.5 percent down payments or less.

REITs

REITs are Real Estate Investment Trusts and are purchased like stocks or mutual funds. I have purchased a few of them in my IRA in the past. REITs are large funds that invest in real estate and then pass on dividends and profits to the shareholders. REITs will invest in large commercial projects, land, industrial buildings, or even government buildings.

REITs are the easiest way to invest in real estate since the trust decides what to invest in and handles all the management. The returns may be great but can also go up and down like the stock market. I prefer to invest in real estate with a more hands-on approach because I can make more money. You can’t buy a REIT below market value like you can a house.

Investing in different housing markets

Many people would love to invest in real estate but find house prices extremely high in their market. New York, San Francisco, and many other areas have incredibly high prices for real estate. If the price for a starter house is $500,000, that makes it very hard to invest in real estate. It will take a lot of upfront cash with high prices and be very difficult to cash flow.

Investors are starting to invest in real estate by investing hundreds or thousands of miles away. There is a lot of work needed to make long-range investing work. You need to pick a market, find a great realtor, find a great property manager, and find the right property or properties. I have not tried to invest in real estate long distance, but I have talked to and learned from many people who have.

Tips on long-distance investing:

Pick a location

One successful investor I know hired a firm that keeps track of detailed sales information to find the best markets for his fix-and-flips. He then spent 6 months there exploring the market and then decided to invest in real estate in that area. I am not saying you have to spend 6 months in an area; after all, this investor makes his living flipping. It is smart to spend some time meeting people and exploring any area you want to invest in. I think it is smart to start with areas you may have lived in before or where you have friends or family.

Find a great Realtor

A great realtor is key to any successful investment strategy. If you want to invest in real estate long distance, you need an awesome agent. That agent will help you find deals, possibly inspect houses for you, and schedule inspections. If possible, I always suggest investors become agents themselves, but that is difficult with long-distance investing.

Find a property manager

If you want to invest in long-distance rental properties, you need a property manager. A good property manager can mean the difference between profitable rentals and a disaster. A property manager will rent out the house, manage the expenses, hire contractors, and look over the house for you.

Find a great contractor

It can be tricky to find a great contractor in your local area; it’s even tougher long distance. This is where you need a great Realtor and property manager to help you find a great contractor. The best way to find a contractor is word of mouth or referrals. You need to have people you can trust in the area you are investing in to refer contractors.

Vacation rentals

Vacation rentals are not my specialty, but I know the basics. Buy a house in a great tourist location, use a great property manager to rent it out for you, and collect the rent. The difficult part of a vacation rental is the extremely cyclical market. Peak season can bring top dollar while low season can bring almost nothing because demand goes down. I have stayed in many vacation rentals, and the key, in my opinion, is to price a vacation rental low enough that the unit stays rented.

The cash flow on vacation rentals can look amazing at first, but the management fees, expenses, and vacancies will almost always be much higher on a vacation rental than a long-term rental. Vacation rentals take a lot of management if you want to take on that task yourself. I am not saying you cannot make money with vacation rentals, but you must be very careful.

Speculating

I think that investing only to hope your property goes up in value is speculation. Many investors will invest in real estate and hope it appreciates, so they can sell the property for a profit. This is a very risky tactic. Most of the time, cash flow is not the primary goal, and people end up losing money every month when they invest for appreciation.

It is very difficult to hold a property for years when you are losing money every month. Many times, the investor will be forced to sell the house in a down market and lose even more money. If you invest for cash flow and look at appreciation as a bonus, you can avoid this mistake.

Other investors are sometimes forced to move out-of-town or they want a nicer house but cannot sell their current house. The investor ends up renting out their house and hoping the market improves enough to sell the house in the future. This tactic is also dangerous because there is no guarantee the market will appreciate. The market could continue to decline and make things even worse.

Non-performing notes

Non-performing notes are mortgages that have been taken out against a house and the homeowners stopped paying or have fallen way behind. The interesting part about investing in non-performing notes is you can buy them for a huge discount. Many companies sell notes to investors.

When you invest in non-performing notes, you are not buying the house, only the mortgage. If the owner defaults, you must foreclosure yourself, complete a Deed in Lieu, allow a short sale, or come up with another solution. Buying notes can be a great way to invest in real estate without actually buying a house.

Crowdfunding

Real estate crowdfunding is a newer strategy where a company gets many investors together to loan money to other investors. It is similar to hard-money lending for house flippers. The rates and terms for the investors can provide a decent return, but there is a risk that the end investor could default and you lose your money. There are many companies that have started crowdfunding sites.

Real estate agents

If you want to make money in real estate but don’t know about investing yet, you may want to look into becoming an agent. I have made a lot of money selling houses as an agent and broker over the years.

You can also save a lot of money by being a real estate agent when you invest in houses as well. I save hundreds of thousands of dollars a year as an agent and get more deals as well.

How to invest if you don’t have a lot of money

I talk to a lot of real estate investors through email, Facebook, and in my coaching programs. One of the most common questions is, “how do I get started if I don’t have the money?” There are a lot of gurus who teach real estate is the answer to any financial problem. Real estate can be an awesome way to invest your money and build wealth. It can even be a great way to make a lot of money when you have very little. However, real estate investing is not easy, and if you want to make a lot of money, it will take time and sacrifice.

What is the first thing you should do?

If you don’t have any money right now, don’t feel bad. Most people live paycheck to paycheck, and 15 percent of Americans live below the poverty line! America is one of the wealthiest nations in the world, and it is important to remember we still live in one of the best times ever. Some sources claim 50 percent of Americans lived in poverty during the 1800s. Even in the 1950s, up to 30 percent of Americans lived in poverty. While some say the American dream is dead, I disagree and believe this is a great time to be alive.

If you are low on funds, you have the ability to change that. Changing your attitude about money, changing your spending habits, and changing how you think about those who have money are all ways to improve your finances. If you have bad money habits, real estate will not solve all your money problems. It is important to save money, invest it wisely, and have a plan. Floating through life hoping things get better rarely if ever, works.

While real estate will not magically fix your money problems, but it can be a great way to invest and build wealth. However, you also need to work on basic money management.

Here are some questions I ask people who tell me having no money is their biggest problem:

- Besides investing in real estate, what are you doing to fix the problem? Have you looked for a better job, an extra job, another job, or asked for a raise?

- Do you have a budget and know how much you spend? Most people have no idea how much money they spend or what they spend it on.

- Do you have a car or house payment that is too high compared to your income? Lenders do not care about how much money you can save when they give you a loan. You should not buy the most expensive house or car you can.

- Have you talked to a lender? Lenders can give you an idea of if or when you can buy a house. They can also help with credit problems, debt-to-income ratios, and give you things to work on. Talking to a lender is free!

- If you have another business besides real estate, should you be focusing on it instead? A lot of people lose focus and try to do too much at once. I always tell people who are trying to become real estate agents to avoid trying to be investors at the same time. Focus on one career, and once you have mastered it, expand.

Too many people rely on real estate to fix all their money problems without looking at why they have no money. The better off you are financially, the easier it will be.

What is the best way to start?

Being low on money does not mean you cannot invest in real estate. It makes it harder, and you need to realize it will take sacrifices and hard work to make it happen. If you want it all to be easy or don’t have time to dedicate to the process, you will probably be broke the rest of your life. Sorry to be blunt, but most people want the easy way out, and easy rarely, if ever, works. The best way to invest in real estate if you don’t have the money is to buy a house to live in.

Many people cannot buy their own house because they have bad credit, bought a car that was too expensive, or don’t control their finances. All of these problems can be fixed, but again, most people will not make the sacrifices needed to fix them. I drove a 1991 Ford Mustang as my daily driver for 10 years before I had a car payment. I always made my payments on everything, even if it meant making sacrifices in other parts of my life. Gurus love to claim you don’t need good credit to succeed, but it sure makes life easier.

When you buy a house for yourself, do not buy any house on the market that you or your family love…buy an awesome deal. Again, it takes sacrifice. Getting a great deal takes time, research, patience, and the ability to do some work. Most people don’t want to make those sacrifices.

If you make those sacrifices and get an awesome deal, you can earn tens of thousands of tax-free dollars from your house. Or, buy an awesome deal that you only have to live in for a year, and rent it out once you leave. Buying the right house can be life-changing and set you upon an amazing path. You can buy houses over and over again as an owner occupant as long as you live in them for a year.

House Hacking

When you buy as an owner occupant you can start as an investor at the same time. House hacking is when you buy a multifamily property to live in the unit and rent out the other units. If you buy the right property you could end up making money every month while you live for free! You can even buy a single-family home and rent out rooms to earn money (be careful with zoning laws). House hacking is a great way to get started with very little money, but again, you need decent credit and some money.

What if you can’t afford to buy a house yet?

Many people may have to wait a couple of years before they fix their finances or can buy a house. If you cannot buy a house yet, do not give up hope! There are ways to make money in real estate without getting a loan. Stay focused on fixing your finances, and don’t assume real estate investing will fix everything. When using these techniques, you still need to work on your credit and savings.

Wholesaling can be a great way to get started in real estate and is often taught as the easiest way to make millions doing so. Wholesaling is difficult, and it takes time to get systems set up. If you are looking to earn extra money or start a new career, you could also become a real estate agent. You can even flip houses with little to no money if you find the right people to work with. Buying rentals is another way to invest in real estate that can be done with little or no money.

Do you need a business plan?

Many people get overwhelmed by educating themselves and trying to figure out the best course of action to take. There is a lot to learn, and there are many different techniques that can be used. To keep track of everything, you need to have a plan. You must write down your goals, the steps you will take to reach those goals, and when you will complete those steps.

This will give you a road map to get where you want to be. You do not have to write out a fancy 50-page business plan. Get a notebook and just start writing down the things you need to work on. Write in it every day, and eventually, you will see the right path for you. While making your plan, you can write down other ways you will improve yourself financially. Things do not magically change overnight, but making small changes every day can lead to big changes in the long run.

Conclusion

Real estate is an amazing business, but you have to work hard and smart to make it work for you. It will not magically transform your life when you have no money, no credit, and are not willing to work hard to change things. Real estate can help you make more money, but at the same time, the more you improve your financial situation, the easier it will be.