Who are the Best Hard Money Lenders?

Hard money loans are typically used to flip houses or for short term financing on other real estate projects. Finding a hard money lender is not a difficult task. A Google search for hard money lenders will turn up about 1,000 results. The tough part is finding the best hard money lenders that have reasonable rates, lends in your local market, and is experienced. Some hard money lenders charge more than 15% and some 8% many others cannot perform when a deal is on the line. I am a real estate agent as well as an investor and I have seen multiple deals fall through because a hard money lender dropped the ball. I have also used four of the largest hard money lenders in the last two years and can give you my experience working with each one. There is just one that I would use again.

There are great hard money lenders out there, but they are not always easy to find. There are a ton of companies that call themselves hard money lenders and most do very little lending. A lot of hard money lenders are also localized to one state or even one area of a state where they know the market. However, there are some larger hard money lenders that work in many states and have lower rates than a typical hard money lender. Those are the lenders I have used and will review.

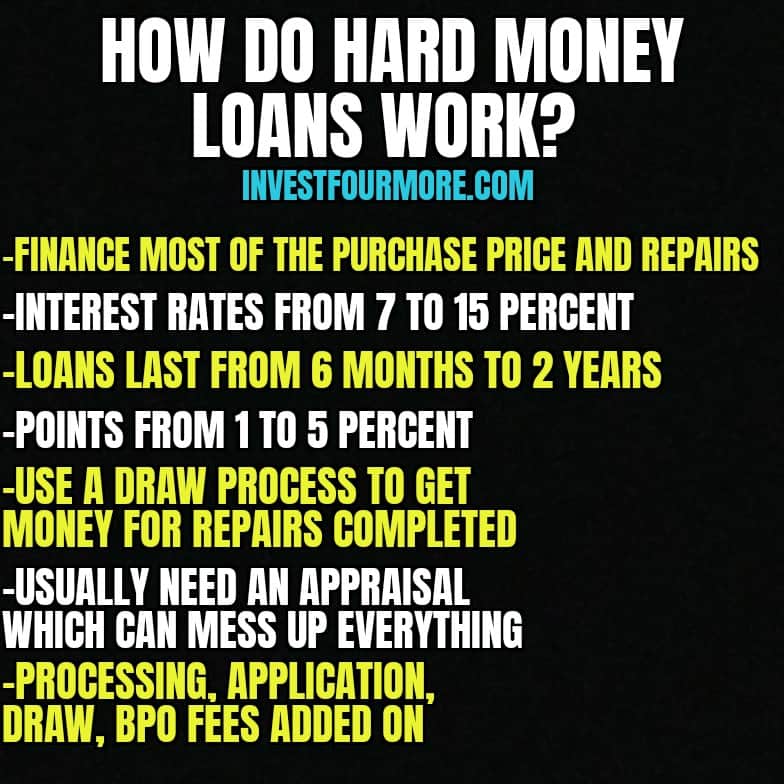

How does a hard money loan work?

Hard money loans are not loans from a bank. A hard money loan involves a company (hard money lender) borrowing money from investors and then lending that money to other investors at a higher rate. Hard money loan interest rates are much higher than bank loan rates because the hard money lenders are taking on more risk. The hard money lender is also borrowing money at a much higher rate than banks will borrow it, which means the hard money lender has to charge a higher rate to make money.

In the past, a typical hard money lender charged 12 to 18 percent plus 2 to 5 points on the loan. Points are a percentage of the loan amount and added to the loan amount (origination fee). A 5 point fee on a $100,000 loan would be $5,000.

Hard money loan rates have decreased dramatically in the last few years and most lenders are now offering rates lower than 10% and some offer rates lower than 8%. The points that hard money lenders charge have also decreased to less than 2% in many cases as well. The three hard money loans I got (one attempt failed) on my house flips were all in the 8 to 9% range.

Here is the video I did on these hard money lenders as well:

Why would investors use hard money?

There are a few reasons investors use hard money.

No other loans available

Many investors may have no other choice than to use hard money when flipping houses. Most banks do not like to lend on house flips because the loans are so short. When a bank makes a 15 or 30-year loan they do not expect it to be paid off in 6 months or a year. Hard money loans usually have terms of one to two years and are made for house flippers.

A typical mortgage is not meant to be used on a house flip and a typical mortgage requires houses to be in decent shape. If a house needs a new roof, furnace, or even has peeling paint, a typical mortgage may not work. Hard money loans can be used on houses that are in most any type of condition.

Financing repairs

Hard money loans often will finance the purchase of the property and the repairs as well. Banks will rarely finance the repairs on a house unless you are using an owner occupant FHA 203k loan. Hard money loans will often finance all the repairs needed on a home. However, the lender may not pay for the repairs upfront. They usually use a draw system where work is completed and then the lender reimburses the investor in stages.

Low down payment

Most investor loans with banks require at least 20% down. You can find some hard money lenders that will finance 100% of the deal. It is rare and those hard money lenders will be more expensive than the hard money lenders I use, but it is possible. With the hard money lenders I use, they typically finance 90% of the purchase price plus 100% of the repairs.

Speed

A lot of hard money lenders can fund a loan faster than a mortgage. It can take 30 days to complete the mortgage process. Some hard money lenders can fund a deal in a week or two.

This video goes over the different financing options I have used and how much each one costs:

Why did I use hard money lenders?

I flip from 20 to 30 houses a year and I have many ways I finance deals. I have used local banks that offer fix and flip loans as well as private money lenders. Private money lenders are people I know who will lend me money at rates similar to hard money or in some cases even higher rates. Private money can be even easier to use than hard money.

Be careful not to confuse real private money with hard money lenders calling themselves private money lenders. A new marketing trick is for hard money lenders to say they have private money, but it is the same old hard money loan with a different name. When I talk about private money I mean money from individuals who lender to other individuals, not companies lending money to investors.

I used a few hard money lenders because bank money takes a lot of cash. You must pay 25% down when you buy and finance all of the repairs, at least with the banks I use. The private money is great but more expensive than some of the cheapest hard money lenders. I decided to try a few hard money lenders to see if the cheaper rates were worth it.

In most cases, the problems I ran into did not make the cheaper rates worth it and using hard money almost cost me a couple of deals. However, I was able to find one lender who has been decent.

Who are the best hard money lenders?

I used some of the big hard money lenders that lend in most states in the US. I know there are some others I have not tried, but I am only going to mention the ones here that I have direct experience with. You will find that all lenders talk a big game, but you never know for sure how they will perform until you use them.

I have a list of these lenders with links to there sites and other lenders as well on this page: Hard money lenders.

Finance of America review

I am starting off with my worst experience first. Finance of America is a huge company and they have been around for many years. I get emails from a lot of lenders who want to lend me money thanks to my blog, YouTube, Instagram, etc. Whenever I use a lender I make sure I check their rates, terms, and requirement very thoroughly. They told me their rates would super low with very low points as well. I have looked back on my emails and I realized they would never put them in writing. I had to call in to get the rates and terms and even when I signed the agreements with them through DocuSign for the loan they never sent me the completed documents I signed so I can’t even see what the exact rates were.

One of my biggest pet peeves is when lenders refuse to put the terms and points in writing. I should have known better when Finance of America did this, but I was enticed by the low rates. I think they were less than 8% and around 1.25 points.

They call their loan a line of credit even though it is really not. The line of credit is really a credit limit but you still have to go through the loan approval process on every property. A lot of hard money lenders do this. I submitted a ton of paperwork about my financials, tax returns, bank accounts, etc. When they finally had everything they needed they said I had to pay a $700 application fee! No other hard money lender had done this and there is no way I would have paid it except I knew they were one of the largest hard money lenders in the country, or at least they said they were.

I had my “line of credit” approved and I waited for a property to finance with them. I found a deal in November of 2019 from a wholesaler. I was going to buy for $190,000, spend about $30,000 on the repairs and sell for $280,000. I got the deal under contract on 11/15 and told Finance of America about it. The closing was going to be on 12/2 and I mentioned this to my representative a few times and they said it would be no problem closing that fast.

They gave me more forms and applications to fill out which were pretty in-depth and took some time. I did not want to finance the repairs even though I could have. I would rather pay for those myself and avoid the annoying draw process and fees. I was going to put down 10% for the loan and they did need an appraisal. I had to pay $525 for the appraisal upfront and they promised it would be done in time.

The tricky thing with this deal was it being a quick closing and Thanksgiving happened to be during the escrow period. A week before closing and before Thanksgiving I emailed Finance of Americal and asked if everything was on track to close the 2nd, which was the Monday after Thanksgiving week. This was the response I got:

“Final Underwriting has been completed and the loan has now moved to Pre Closing Audit.”

I thought that meant things were good to go, but they were not very clear about it. I still had not heard anything by the end of the week so I emailed asking if everything was set to close on Monday and this was the response I got:

“Good morning Mark,

We are not clear to close. I’m still waiting on your appraisal report and your CPL

Thank you”

I did not get this response on Friday when I sent it but Monday, the day of closing. Luckily, I knew something was amiss and I had back up financing in place. I had talked to my private money lenders who were prepared to close if this company could not. On top of that, it turns out the title company was not ready to close either as they apparently forgot about Thanksgiving and took most of that week off. We delayed closing two days to give time for the title company to close.

I asked Finance of America when we could close and if they could still do the deal in two days. And they said they did not have the appraisal back and had no idea when they could close but do not worry because closing is not for another year! What!!??

Apparently I had written 12-2-20 as the closing date on one one of the application forms and they were going by that despite my numerous emails, the contract, and phone calls that said the closing was 12-2-19. I closed on the property using my private lender and told Finance of Amercial I would not be using them.

It has been three months since that deal fell through and I got a generic email saying sorry your deal did not work please fill out this survey. I filled out the survey and emailed a few people about what happened and not one person has ever responded to me.

I wasted $525 on an appraisal that may or may not have been completed and $700 on an application fee. I also spent hours getting them documents and they would have cost me the deal if I did not have back up financing in place.

My recommendation would be to never use Finance of America for a loan.

Lending One review

Lending One had emailed me for a long time trying to get me to try them out for a loan. Last year I finally decided to give them a shot. I made another mistake and decided to have them finance two properties at once.

I was drawn to Lending One because they said I would not need an appraisal and rates were less than 8% with points around 1.25%. In my business, I am not always able to complete an appraisal on a property before I buy it. I may have to close fast or the property may not be accessible for an appraisal.

I got two properties under contract that were both occupied and were from wholesalers. Lending One knew I could not do appraisals but they said they would do BPOs (broker price opinions). After I got the houses under contract Lending One said they wanted to do appraisals, but they would be exterior appraisals. The appraiser would value the home without going inside. Lending One promised there would be no issues.

I had to pay for those appraisals again and when they came in there were horrible. One house I was buying for $212,000 and I thought it would be worth around $300,000 when done. On the other house, we were buying it for $240,000 and I thought it would be worth about $320,000 when it was done. The appraisals came in at $260,000 and $279,000. That was the after repaired values and what Lending One would be basing the loans on because they would only lend 70% of the after repaired values.

Because the appraisals came in so low I had to bring tens of thousands of dollars more to the closing. I tried to challenge the appraisals and the appraiser would not raise them at all. After doing some research the appraiser appeared to live in Utah and was doing these appraisals in Colorado. He had an address in Denver which was still 50 miles away from me, but that address was a UPS store and all the other addresses pointed to Utah.

I decided to stay with Lending One for one property and use private money for the other. The process did not get any better trying to close the deal. The representative at Lending One got in an argument with the wholesaler (who was a big investor and who I have bought at least 10 properties from). The wholesaler called me up and was furious at the lender and basically said they would not work with me anymore if I used this lender on another deal. The big issue was Lending One was insistent on knowing how much the wholesaler bought the property for. I have no idea why that mattered at all, especially since the loan amount was much lower than what it should have been based on the low appraisal.

We did get that deal done, but I never used Lending One again and both houses sold for more than $300,000.

Patch of Land review

The first hard money lender I used was Patch of Land. I used them because I met one of their reps at a conference. It turned out we both went to the University of Colorado and lived in the same dorm at the same time, but did not know each other.

Patch of Land had slightly higher rates but they were still very good. I got a loan with them and they did not require an appraisal! They did do a BPO and it came in low as well, but we were able to get it increased to what it would be worth. That is one issue you will find with hard money. It is tough to get the after repaired value high enough because most appraisers don’t do appraisals on after repaired value, but current value.

With Patch of Land, I financed the repairs but it was a pain. I had to pay a couple of hundred dollars each time I wanted a draw. An inspector went out to see if enough work was done and they would release the money to me. We had more problems with those inspectors not thinking enough work had been done to necessitate the draw.

The biggest issue I had was Patch of Land was charging me interest on the money for the repairs whether I had it or not. So if my repair amount was $50,000 I pay interest on that full $50,000 as soon as I buy the house.

Otherwise, it was not bad working with Patch of Land. My contact at Patch of Land left for another company and I have not used Patch of Land again because I found lower rates with other companies.

Kiavi review

Kiavi was the most recent hard money lender I worked with. I used them to finance a house flip in 2019. I had just used Lending One and had all those issues so I was waiting for issues to come up with Kiavi as well.

However, I had no problems! Maybe I got lucky, but they were great to work with and there were no issues with the BPO, no unknown fees, and the reps were easy to work with. For me, Kiavi is the company I will use if I want to go the hard money route. I promise that if I use them again and have problems I will update this article!

How do you find local hard money lenders?

If you prefer to work with a local hard money lender I would be very careful who you deal with. Referrals are always the best way to find reputable business partners. Here are a few ways to find some hard money lenders.

- Ask around at a local real estate investor meetup. Many times hard money lenders will sponsor and speak at the meetings.

- Ask your real estate agent or a lender if they know of any hard money lenders. There is a good chance they may not know any, but it does not hurt to ask.

- Check with online real estate investing communities like forums.

- Search online, but be very careful! We had a hard money lender who a buyer was using on a HUD deal recently and they could not provide a proof of funds letter to show they had money to lend the buyer.

Conclusion

Hard money lenders can be difficult to work with but sometimes that is the only financing option for house flippers or rental property owners who are looking for short term financing when using the BRRRR method. I had some problems with the lenders I used but it is hard to know if it was an isolated incident or a common problem with that company. I will mention that I can send a lot of business to these companies with my blog and social media, which they all knew. I would think they would have tried extra hard to make my deals go smoothly. There are also some companies that I have heard good things about like Visio and Lima Capital, but I did not review them since I have never used them. I also heard good things about all of the companies I reviewed before I use them.

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

Have you heard of are used We Lend LLC at all?

no I have not