Will the Housing Market Crash Soon? (2025 Predictions)

I have been an agent and investor for almost 20 years and I have seen many market cycles. A lot of people think we are due for another housing market crash because housing prices have skyrocketed, people cannot afford homes, and there could be economic problems. Besides these factors, there are many things that drive the housing market. What really drives market prices is supply and demand, which is impacted by these factors and many more. The last crash that occurred in the United States from 2006 to 2012 was the worst in the history of the country, it was worse for housing than the great depression. It took extraordinary circumstances to create that crash and it will not easily happen again. Could it happen? yes Will it happen? Maybe. When will it happen? No one really knows. Even with Covid-19 causing chaos, there is no guarantee a crash will happen.

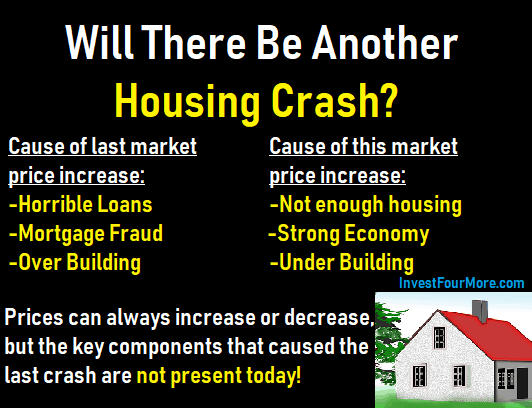

What caused the last housing crash?

I started my real estate career in 2002 before the last housing crash. I could see something was off in the real estate market but I was young and did not know what all the signs were indicating. It was not uncommon to see:

- Loans that were 120 percent of a house’s value

- Investors buying multiple properties with nothing down

- People with no income buying houses with a no money down loan

- People simply stated what their income was to get a loan with no proof

- 6-month ARMs with the payments doubling soon after buying the house

Something seemed off to me but everyone seemed to be happy! Then the bottom dropped out of the market. The banks realized that many people could not pay back their loans and there were too many houses being built for the people who could actually buy a house.

Crazy lending guidelines caused overbuilding and when the party stopped, there was a crash. Prices dropped and more foreclosures occurred because many people had no equity. Banks panicked and tried to sell all their distressed properties at once.

It was the perfect storm and the worst crash in the history of the United States housing market. The big question is can that happen again? I personally do not think so and I will tell you why below.

Are there really too few houses?

Supply is affected by foreclosures, homeowners’ willingness to move, new construction, and many other factors. Demand is driven by the economy, lending guidelines, potential homeowners’ confidence, wages, and much more. I believe the supply and demand affecting today’s housing market is much different than what drove the last housing boom. While prices could level out or decrease in some areas, I do not think we are in for a nationwide crash.

In order to have a crash, we need an oversupply of homes or the demand for homes to disappear. I do not see either scenario happening, even if the economy loses steam or crashes. Some of the stats I show in this article will show you how different the supply side is right now than it was prior to the crash.

How many housing crashes have there been?

Many people believe that because of the huge increases in prices, a crash is imminent.

“Just look at what happened in the mid to late 2000s. Prices are so crazy now that a crash has to come soon!”

The first thing you have to realize is that the last crash was the worst crash we have ever had. It was worse than the great depression. Those crashes do not happen over and over again. An increase in prices does not mean a crash is coming. Prices can increase or decrease, but that is what happens in a healthy market. A crash is much different from a down market. Other countries have seen increasing prices for decades without a crash. Just because prices go up does not mean they go down. In fact, due to inflation prices will continuously increase over time and they have increased over time.

There are also a lot of people trying to sell books, products, and coaching based on the impending doom that is coming. Be careful buying into what people say based on their motives. Look at the data!

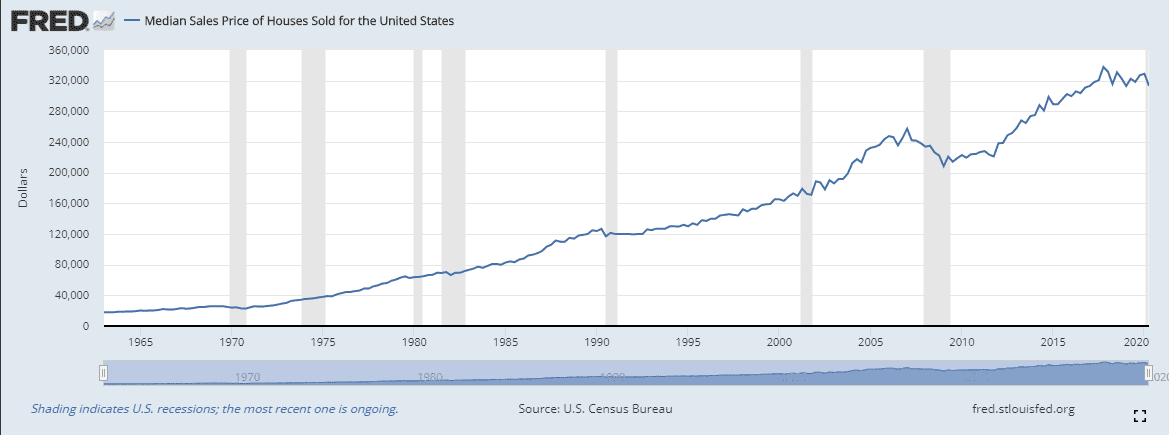

The chart below shows the median sales price in the United States since 1959. As you can see, prices can fluctuate but in the long run, they have always gone up.

Won’t a recession cause a housing crash?

The last crash was the biggest in recent memory and if you look at the data further back it is the same with small adjustments. A lot of people will also tell you we have a housing crash or recession every 10 years. If you average them out we have recessions every 18 years, but not always true for the housing market. The dot com recession did not affect housing much at all. Sometimes we have a recession 5 years after the last one and sometimes we have it 25 years after the last one. Even if we did have a recession every 18 years we have a long time to wait since the last recession was ten years ago.

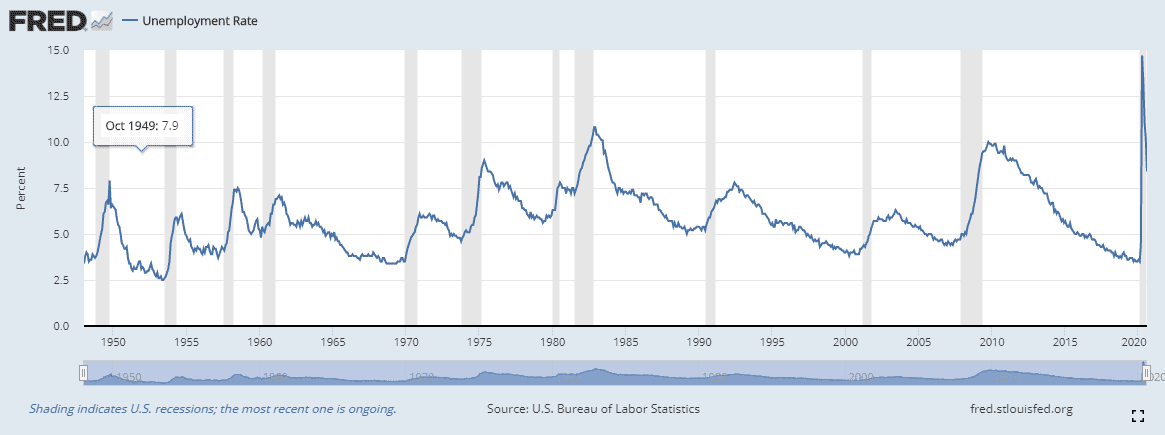

The chart below shows unemployment in the US, which is a great indicator of recessions. https://fred.stlouisfed.org/series/UNRATE

You can see from the chart that recessions are not every 18 years, but all over the place.

There are also a lot of people who have been predicting a crash for many years. There are people on YouTube promoting their gold and silver businesses by talking about how real estate will crash. One of the big marketing messages they use is that they predicted the last crash! Well, if you look at their predictions they have been predicting a real estate crash every year for the last three decades. They were bound to get it right one of those years! I was an REO (foreclosure) broker during and after the last crash and there were many people talking about how there was going to be a double-dip recession in 2012. We were going to have a tsunami of foreclosures and it would be much worse than the crash we just went through. Well, it never happened, in fact, the opposite happened.

No one knows for sure what will happen to the housing market. It could go up, it could go down, it could crash. But just because it crashed before when prices were high, does not mean it will crash again.

The video below goes over the possibility of a housing crash as well:

Will Covid-19 cause a housing market crash?

Many people are now saying that coronavirus and its impacts will cause a housing market crash. The interesting thing is that since the coronavirus started, housing prices have increased in many areas! The supply of homes has decreased because many sellers took their homes off the market. This caused prices to increase because the demand for homes has stayed relatively stable. There are the same amount of buyers fighting for fewer homes.

It is true that many people let their mortgages go into forbearance or are behind on rent. The CDC halted most foreclosures for the rest of the year. There has to be a crash right! There will be so many foreclosures being dumped on the market and that will cause prices to drop.

Foreclosures do not cause a housing market crash. Every healthy market has foreclosures. The last crash was caused by millions of foreclosures coupled with too many houses being built. Foreclosures by themselves can cause a downturn but not a crash.

It is also important to remember that Covid-19 will not automatically cause a flood of foreclosures. The government will do everything they can to stop foreclosures and in some states, it takes years to foreclose. Many people also have equity in their homes which means they can sell them instead of letting them default back to the bank.

Home mortgages are harder to get than ever

One of the main reasons people say there will be another crash is that loans are easier to get again!

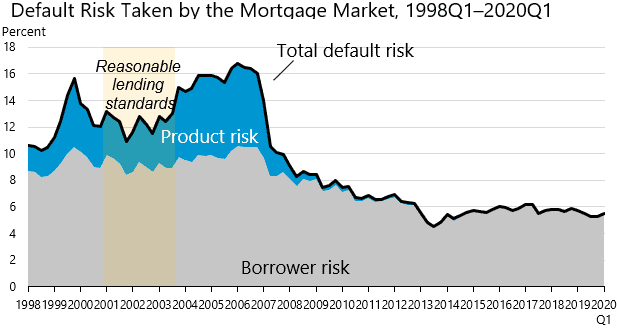

In 2005, subprime loans were rampant and as a result, the country over-leveraged itself. Subprime loans, the riskiest loan type given to borrowers with low credit scores, totaled more than $620 billion. Now, subprime originations are only 5 percent of the mortgage market and add up to $56 billion. Compare that to 2005 when subprime origination made up 20 percent of the market. This represents a 91 percent decline from the height of bad loans that set up the economic crash.

Source: Inside Mortgage Finance; Equifax

Not only has subprime lending seen a major decline, but mortgages have also become much harder to attain due to stringent lending standards. Loans are still very hard to get compared to before the last crash. This is greatly due to the type of borrowers able to qualify for loans. The current average credit score for borrowers being granted mortgages is 739. In October 2009, the average FICO score was 686, according to Fair Isaac. The lowest one percent of mortgages issued have credit scores averaging 622-624. Compared to the average range in 2001 of 490-510, the standard to get financing has risen substantially, and as a result, the likelihood of default has dropped. Lenders have done this to ensure the economy doesn’t again become propped on bad loans like it was leading up to the Great Recession.

The chart below shows that loans are even harder to get than right after the housing crash. https://www.urban.org/policy-centers/housing-finance-policy-center/projects/housing-credit-availability-index

As you can see, it is not easier to get a loan, in fact, it is harder!

Investors have even stricter lending guidelines and must put 20% down. There are stricter debt-to-income levels for investors and some banks even limit the number of loans investors can have. It is much tougher to get a loan now than almost any other period in the last century.

Is the United States housing market unaffordable?

Another reason people say the market will crash is that housing is not affordable for most people and it has to crash.

It is true that the affordability index continues to be stacked against potential home buyers. As housing and rental prices steadily increase, wages continue to stay relatively stagnant. Historically, the average income-to-housing cost ratio in the U.S. has hovered near 30 percent, but in some metro areas, that number is currently closer to 40 and even 50 percent! This strips away the opportunity to save money as a significant portion of a person’s monthly income is going to keep a roof over their head.

Source: U.S. Census Bureau

However, the United States is still much more affordable than in many other countries. Many of those countries have not seen a huge crash. People tend to find ways to buy homes, even when they are very expensive. Affordability in itself will not cause a crash. Although, it could cause a slowdown.

Some of these charts are a few years older, but it’s tough to find updated information. As you can see there are many other markets that have higher prices than the US (even after our last rise) and did not have a housing crash, or they recovered very quickly after a smaller crash. Simply having high prices does not mean a crash is coming.

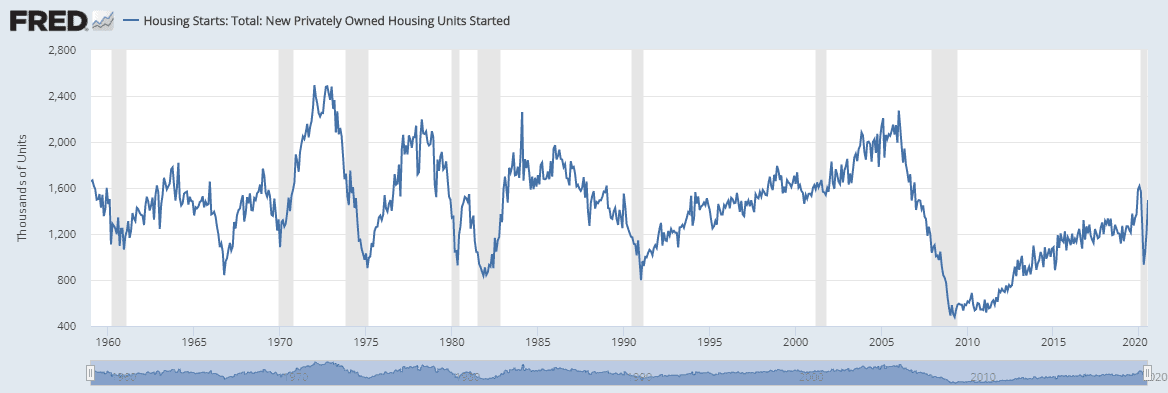

Why is supply so low?

The biggest factor causing the housing market to increase today is low inventory. The last crash was caused by horrible lending guidelines and overbuilding. We will continue to have low inventory until building picks up, and it simply has not happened. I cannot see another crash occurring until we see more new starts.

The graph below shows new building starts in the United States and as you can see there was a record low building for many years after the crash. We just got back up to the average number of new builds when Covid-19 hit and it dropped again.

There simply are not enough houses for people.

This is why prices continue to increase in the United States. The population is growing and there are not enough houses to meet the demand for everyone who wants to buy a house.

We could absorb a lot of foreclosures and still have a healthy market, a more healthy market than we have now. Having an increase in foreclosures will not crash the market. We would also need an increase in new builds which is not happening at the pace of market demand.

Will migration and population cause a crash?

Another popular theory is that baby boomers will die off and there will be too many houses for those still alive. This idea was pushed back in the early 2000’s by Robert Kiyosaki. While there were a lot of baby boomers born, there are currently more millennials than baby boomers. The millennial generation is actually increasing thanks to immigration. There are fewer people being born now, but those people will not be of house buying age for decades. It is predicted the US population will keep increasing for decades. Other countries have had decreasing populations and have not seen decreasing prices.

This article goes into more detail on baby boomers and a housing crash.

Will interest rates cause a housing crash?

Another prediction is that interest rates could rise and cause a crash. This theory is based on nothing but a guess as rising rates have never caused a crash in the past. Interest rates were 18% in the early 1980s and there was not a crash. While it seems logical that prices decrease when rates increase because houses get less affordable it does not happen. The mortgage rates on a house are typically locked in for many years. If interest rates go up it will cause fewer people to move which will decrease inventory even more! The video below has more details on this.

Why are others predicting a crash?

A lot of people are predicting a crash, but why? If the data shows that a crash is most likely not going to happen why would they predict one?

Here are some of the people who are predicting a crash:

- Gold and silver sellers who want people to invest with them and not in real estate

- Stockbrokers who want people to buy stocks and not real estate

- Real estate investors who are selling coaching programs about how to survive a crash

- Anyone who is trying to get their name in the news or create a catchy headline to sell something

- People who want cheap housing prices so it is easier to invest.

Not everyone who is predicting a crash has an ulterior motive but many do. Some very smart people are predicting a crash who may not know exactly how real estate works either. You have to be very careful who you listen to when it comes to real estate and predictions.

What can we predict?

I buy a lot of house flips and rental properties. One of the most important rules of thumb I work by is to never base my purchases on what housing prices might do. If I am flipping houses or buying rentals, I never assume prices will go up. I base my investment strategies on today’s prices. I also have a plan in place if the market decreases. Yes, we have seen huge price increases, but that does not mean prices will keep going up or that they could not go down. One of the easiest ways to get yourself in trouble is to invest in real estate because you think prices will increase.

I do not try to predict the market and most economists will not predict it either. There are too many variables to know what will happen and predicting when it will happen is even harder. If someone says they know exactly when a crash or downturn will happen, they are probably trying to get attention or sell something!

The market could go up or it could go down. The great thing about real estate is you can make money in every market if you know what you are doing.

Conclusion

The factors that caused the last crash do not exist in today’s market.

- There is not overbuilding, in fact, there is too little building.

- There are not loser lending guidelines, in fact, there are more strict lending guidelines.

- While foreclosures may increase, there are much fewer than before.

Rising prices and unaffordable housing do not cause a crash. They could cause a downturn or cause prices to level out, but a crash is much different than a downturn. If you are waiting for a crash to invest or buy, you may be waiting a very long time!

Join me on The $100M Mission!

Get exclusive updates as I work to own $100M real estate by 2030 in today's market. Whether you're just starting out or already investing, you'll get actionable insights from my real-world deals and setbacks.

Plus, I'll help you set and achieve your own ambitious goals. Transform your financial future - subscribe now for weekly updates.

Together, we'll prove that massive success in real estate is still possible.

I agree that there is not a general housing market bubble at the moment. Housing prices might stagnate in certain areas as prices begin to exceed what people can afford and may decline a bit when interest rates rise. That’s not to say there won’t be a crash, if there is it would be due to economic factors outside of the real estate market itself.

Yes, I feel about the same way Dave!

For a few years now, the reason for fast rising home prices have been blamed on tight inventory. After seeing what has happened in Toronto, I’m starting to question these claims of tight inventory in almost all major housing markets (US and globally). In Toronto, within two weeks, they went from having very low inventory to having a 50% increase. Where did all of their extra inventory come from? Could the same happen to other major cities as well? It’s possible that there are low inventory in so many places due to aggressive investor speculation, which is then causing locals to panic buy. Very similar to the irrational exuberance happening before the housing crash 10 years ago. Something can trigger these property investors to sell all at the same time, and cause buyers to pull back, similar to what’s happening in Toronto. Another housing crash is possible, and it doesn’t have to be caused by bad loans like last time.

I find it hard to believe inventory increased by 50 percent, do you have any numbers on that? To see why inventory is low you need to look at the number of sales as well. If we were selling many more homes that would indicate inventory is low because people are buying everything up, but sales are down. That indicates it is not investors buying everything, but there are simply not enough houses for sale. That is what I see in most markets. There are not enough houses for everyone who wants to buy.

“…Low-money-down loans have been available for decades, and that is not what caused the housing crash. Really bad loans to people who should not buy houses is what caused the housing crisis. …” I’m presuming this is a ‘cliff notes’ take on the market since we can’t dispense all knowledge in a post. But my quick 2 cents. As a 2nd generation broker/investor/finance degree holder, bad loans where just a part of the problem. We had funds flowing out of other ‘under performing’ investments…e.g: $’s tend to move from CDs to collectables to stocks to real estate. I’ve owned all but stocks. Further, and this a more of a localized thing, wages must support prices. Las Vegas had speculators running up prices but buyers weren’t all from out of town so prices couldn’t be sustained. Here in NW Detroit suburbs, we are seeing a lot of new industry coming in and hence price strength above what might be healthy in other parts of MI.

Real estate is very localized. I think the biggest difference between now and the last down turn was they are not building like crazy as they were before.

I apologize for coming to the table late, but lets get the record straight.

Lending to people who shouldn’t have borrowed was NOT the issue. Here is a summary of the causes. Do the conditions still exist? You bet!

Subprime lending

Growth of the housing bubble

Weak and fraudulent underwriting practices

Predatory lending

Deregulation

Increased debt burden or overleveraging

Financial innovation and complexity

Incorrect pricing of risk

Boom and collapse of the shadow banking system

Commodities boom

Systemic crisis

Role of economic forecasting

i would completely disagree with you on the lending to people who should not have gotten loans part. I was a person who got a loan during that time. I made all my payments, but it was a stated income loan with almost no verification of income. I basically said I want to buy a house for this much and they said okay. Things are so much different now.

Subprime lending – exists but is rarely if ever actually used. Much less than before. Read the stats in the article

Growth of the housing bubble – prices are higher, but not because of over demand, but because of little supply.

Weak and fraudulent underwriting practices – very rare and much less less than before.

Predatory lending – Very rare and much less now

Deregulation – nothing yet, maybe soon

Increased debt burden or overleveraging – again not nearly as common as before especially for investors

Financial innovation and complexity – to a point, but many exotic loans like 6 month arms are no longer available or stated income loans

Incorrect pricing of risk – THe investors who bought the bad loans before are much more careful now. They will not buy any package but want strict guidelines in place for lending.

Boom and collapse of the shadow banking system – I don’t know what you mean

Commodities boom – I am not smart enough to comment on this

Systemic crisis – i don’t know what that means either

Role of economic forecasting – I think people are much more careful now than pre crash.

I would agree with you, Mark. Subprime lending is available even through FHA with scores as low as 580. But the difference is that Subprime now is what it really means – people with weaker credit scores. The still have to be able to afford the mortgage as income is verified. No more sign and drive loans available.

Correct and very few lenders are actually lending on subprime now either.

Hi Mark, do you mind sharing what your plan would be in case the market decreases?

I have a video about it on Youtube but I can write something new too.