How to Start Investing in Rental Properties (Beginner’s Guide)

How to Start Investing in Rental Properties

Rental properties can be an amazing investment. While it may seem really tough to get started as a real estate investor, it may not be as tough as you think. There are also many misconceptions about how people make money with rentals and how risky they are. This guide is going to help you learn all about rentals: why they are an awesome investment, how much money it takes to buy them, how to finance them, how management works, and many other tips and techniques. Owning rentals is not just about fixing toilets at 2 a.m. as many would make you think, and the returns can greatly outperform the stock market. There are some risks with rentals as well and we will go over those too.

Table of Contents

Why are rentals the best investment?

I have been a real estate investor for almost 20 years. Real estate has been an amazing tool that let me start as an agent and work myself into flipping and buying rentals. My rentals have allowed me to feel secure with buying exotic cars, a nice house, and going on nice vacations. I know the money will always be coming in from my rentals, whether I work or not, and that is one reason I think they are the best investment out there.

I flipped 26 houses last year and 26 the year before that. I’ve also sold more than 200 houses in a year as an agent. I have made a lot of money, but it never seems to accumulate as you think it should! I used to stress a lot about money, but one of the ways I eliminated that stress was to buy rentals.

Rental properties multiplied my wealth. For every dollar I put into them, I saw immediate returns because I got great deals and always bought properties that made money every month after all expenses. I was also able to refinance properties which allowed me to get money back so that I could buy more. The rentals gave me net worth, cash flow, and peace of mind that I was investing in something that would grow. I also knew that even if I lost all my income tomorrow, I had built passive income that would keep coming in whether I worked or not.

The video below goes over my first rental and how it performed:

While I have done well in real estate, one of the great things about rentals is you do not have to make a ton of money to invest in them. The more money you have, the easier it is to get started, but there are ways for the average income earner to become wealthy by investing in income-producing properties. I wish I would have used these strategies more when I was younger, but no matter how old you are, you can still see great returns with real estate.

My residential rentals have actually given me money back after refinancing some and selling a couple of others. I have negative money invested in them, and they still make me $6,500 a month after all expenses, including property managers. I have built millions of dollars of equity in them, and those are just my residential rentals. I have 17 commercial rentals that do even better.

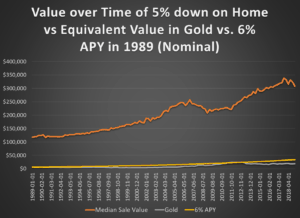

One of the great benefits of real estate is controlling a large asset with little money. The chart below shows how a small down payment increases your returns vs making a 100% investment in gold or the stock market.

How do you make money with rentals?

Many people will say the stock market is a better investment than rentals because the historical price of stocks has gone up more than the historical price of real estate. However, the price of a home is only a very small fraction of the investment when buying rentals. I love to see my rentals go up in value, but I think of appreciation as a bonus. Here is how a good rental property will make you money.

Cash flow

Cash flow is the income you make after paying all expenses. The rent minus all expenses (including the mortgage) should leave you with income every month on a good rental. For example:

- Rent is $1,500 a month

- Mortgage with including taxes and insurance is $900 a month

- Maintenance costs are $150 a month

- Vacancy allowances are $150 a month

- Property management is $150 a month

- The property makes $150 a month

$150 a month may not seem like a lot of money, but that is just one way to make money with rentals. You will also find the rents, mortgage payments, and expenses will vary greatly on each property. Some properties will make more than others, and some will not make any money at all.

Buy below market value

I always get a good deal when I buy rentals. One of the greatest advantages of real estate over other investments is that you can buy it below market value. Every house is different. It is in a different location than other houses and it has different features. This makes real estate hard to value, and because it is hard to value, that creates opportunities to get great deals. Some sellers want to sell quickly, don’t want to make repairs, or don’t care about money (sounds crazy but it happens).

When I buy rentals, I create instant equity by purchasing below market value. Here is an example:

- I bought my first rental for $97,000

- It needed $5,000 in work to get ready to rent out

- I fixed it up and rented it out for $1,050 a month

- After I had fixed it up, I could have sold it for $130,000 to $140,000

I created instant equity and increased my net worth by $30,000 to $35,000 with one rental. When you get a great deal, it makes investing in real estate much less risky.

Tax advantages

Rental properties have some amazing tax advantages as well. Almost all the expenses on a rental are either deductible or depreciable. If I get a mortgage on a rental, the interest paid on that mortgage is an expense and deductible.

The big kicker is that the structure can be depreciated as well. On residential rentals, the structure of a property is depreciated over 27.5 years. Using my first rental as an example, the structure was worth $80,000 when I bought it. Every year, I can depreciate $2,909 from my income, which lowers my tax bill. I am not spending this money, and the house is not really losing that value, but I still am able to deduct the depreciation. When I sell a rental, the profits are taxed lower than ordinary income in most cases as well, and it is possible to complete a 1031 exchange, which defers all the taxes.

Principal pay down

When you have a loan on a property, you are paying part interest and part principal with every payment. While we may only be making $150 per month on the rental example I gave above, a couple of hundred dollars is being paid off on the loan every month as well. Hopefully, you are making much more than $150 a month and are paying down the loans as well.

Appreciation

I do not like to count on appreciation, but that is what most people focus on who are trying to convince you real estate does not have good returns. Appreciation is great, but I never count on it…it is a bonus to me. It can be a very big bonus in some cases. I bought that first rental I mentioned earlier in 2010 for $97,000. It is worth almost $300,000 today. Now, to be fair, I am in Colorado, which has had one of the highest-appreciating markets in the country. I would never count on prices going up that high.

How much money do you need to buy a rental?

This is the part where many people get frustrated and give up. They know rental properties are a good investment, but they have no idea how to get the money to buy one. I will go over the traditional way to buy a rental property first.

How to buy a rental with an investment loan

The typical way to buy a rental property is to use an investment loan, which takes 20 to 25 percent down. If you buy a property for $100,000, you will need at least $20,000 for the down payment alone! This is why many people never buy a rental but don’t worry, there are more costs. You will need to pay closing costs, which can run another 2 to 4 percent of the loan amount. You also may need to have reserves in place, and the home may need some repairs.

- Down payment: $20,000

- Closing costs: $3,000

- Repairs: $10,000

- Reserves: $5,000

- Total: $38,000

That is a lot of money for one rental property! There are other ways to buy.

The video below goes over how much money is needed as well:

Buy a rental as an owner-occupant

Is it legal to buy a rental as an owner occupant? Well, if you never live in the home, no, but you can buy a house as an owner occupant then turn the property into a rental after one year. When you buy as an owner-occupant, you can get loans with much smaller down payments.

- FHA: 3.5% down

- Conventional: 3% down

- VA: 0% down

- USDA 0% down

- NACA: 0% down

You can even use down payment assistance programs to lower the down payments even more! There are even loans like the FHA 203k that allow you to finance repairs. With many of these loans, you will have mortgage insurance, which adds to the monthly costs.

Refinancing or BRRRR strategy

Another option to lower the amount needed to buy a rental property is to refinance the loan after you have owned the property for a little while. The BRRR strategy stands for Buy, Rent, Repair, Refinance, Repeat. If you get a great deal on a rental, you should be able to refinance it soon after you buy it and take some, all, or even more cash out than you have invested in the property. You can usually refinance a property for 75 percent of the value. If I would have refinanced my first rental a year after buying it, I could have pulled out most of the money I had used to buy it.

- Value $150,000 (I bought below market and it increased in value)

- New loan of 75% of $150,000 is $112,500

That new loan is more than what I bought the property for plus any repairs I made. I spent about $30,000 buying my first rental, but I could have refinanced it and taken $42,000 out or $40,000 once you take out the closing costs on the refinancing.

House hacking

House hacking is when you combine buying as an owner occupant with renting out a house. You can buy a property that has multiple units or rent out part of a house you live in to help pay the mortgage. You can buy a property that can be rented out right away with a low-money-down loan!

There are many ways to buy rentals with less money than the traditional 20 to 25 percent down. Do not let that aspect of real estate deter you!

What I wish I knew before I bought my rentals

I talked about my first rental already, but I bought more rentals in the next few years. I was not able to buy 10 rentals all at once, but I did buy:

- 1 my first year.

- 1 my second year.

- 3 my third year.

- 3 my fourth year.

- 5 my fifth year.

- 3 my sixth year.

It took time to save the money to buy rentals as I was putting 20 or 25 percent down on all of them. I was married and had kids at the time, so I was not in a position to be able to keep buying owner-occupant homes and turn them into rentals, or maybe I could have… but we can’t change the past, and I did not use that strategy. I could have bought many more much faster if I knew what I know now, but things still worked out great.

My first rentals all cost from $80,000 to $115,000. Most needed from $10,000 to $15,000 in work, and they rented out for $1,200 to $1,400 a month. I got awesome deals on all of them.

What type of property is the best rental?

We know we can make money with rentals, and that it may not take as much money as you think, but what type of property should you buy? There are single-family homes, multifamily properties, commercial real estate, even AIRBNB. I do not think there is one best strategy for everyone. A lot depends on the investor, their market, and their goals.

Single-family homes

I started buying rentals with single-family homes. A lot of people say they are not a great investment, but they have been an amazing investment for me. When I started to buy rentals in 2010, I could make just as much or more money on single-family homes than I could on multifamily properties in Colorado. Now, every market is different, and the exact opposite can be said in other markets.

The advantage of investing in single-family homes is:

- They are easy to finance.

- The tenants pay all utilities.

- The tenants usually take better care of the house.

- The tenants often stay longer.

- They are easy to sell.

Multifamily homes

A lot of investors love multifamily homes, but they are not my favorite. With multifamily, the landlord pays more expenses like some utilities, yard maintenance, parking lot maintenance, etc. There is also usually more turnover, and in my experience, the tenants can be harder to work with.

With multifamily, the expenses to maintain could be slightly lower because you have more units under one roof. However, I usually see multifamily investors needing to rehab their units much more often than I have to rehab my single-family homes. I am not saying multifamily is bad, but in my market, I am really glad I went with single-family.

Commercial real estate

I stopped buying residential rentals in 2015 because prices became so high that I could no longer cash flow with single-family homes. That is one disadvantage to single-family homes. The higher the prices are, the harder it is to cash flow on the properties.

I was going to buy rentals out of state when I discovered commercial real estate in my area. I was able to buy 7 rentals in the last couple of years that cash flowed better than my single-family homes. Commercial real estate can be very complicated, and it takes a lot of time to learn how it all works. There is an opportunity to make a lot of money, but you can lose a lot of money as well.

AIRBNB

The new fad with rentals is to AIRBNB, or use them as short term rentals. Many people are able to make more money renting properties out more like hotels than actual houses. The rates are higher, but it takes much more management, and you have to be careful with cities changing zoning laws and many areas outlawing AIRBNB.

Single-family homes or even small multifamily properties that you can house hack are a great way to start. As you get comfortable and learn the business, you can move into bigger things with apartment buildings or commercial, or just keep buying single-family homes. There is no best strategy, and it often depends on what the best properties are in your market.

Do you have to manage rentals yourself?

A lot of people think landlords are constantly unclogging toilets in the middle of the night. The truth is I have never unclogged a toilet in one of my rentals. I have never done any manual labor in one of my rentals. I have always had contractors, plumbers, or other professionals do that work. I did manage my rentals until I had seven (to be honest, my wife managed them, but I liked to take credit).

It was not difficult to manage the properties, but it did take time. After I had seven rentals, we realized that I was better off using my time to do other things besides finding tenants, collect rent, and oversee the properties. When I hired a property manager, it was awesome. I had someone to take all the calls, rent the properties, and unclog those toilets…or at least call someone else and tell them to unclog the toilet. I have not been some of my rentals for years!

The property management software I rely on: DoorLoop.

You do not have to manage the properties yourself, and for many people, you should not manage them yourself. You need to be tough and strict with tenants to make sure they are paying rent and to make sure you are not buying into sob stories. I was not tough when I managed my rentals, and I think I made more money with a property manager because they were tough and collected more money and as chose better tenants.

If you decide to manage the properties on your own, make sure you know what you are doing. Advertise the rentals well, know what the right rent to charge is, take your time screening tenants, verify references, and be strict with late fees and inspecting the property on a regular basis.

A lot of people get burned out with rentals because they manage them themselves. A good rental should make money even with property management costs.

My best-selling book Build a Rental Property Empire goes over everything in this guide and much much more! You can get it at Amazon as a paperback, ebook, and audiobook!

Rental property common questions

Should you fix up the properties yourself?

A lot of people feel the need to fix up their rentals but don’t want to buy real estate because they are not handy. I fixed up a house completely on my own in 2006. It was the worst mistake I ever made! It helped teach me that my time is better-used managing, planning, and looking at the big picture, not fixing things up.

If you are a contractor, maybe it makes sense to fix up the properties yourself. Otherwise, don’t worry about having to be handy. It takes some time and experience to find good contractors and people to work in your houses, but you do not have to do it yourself. Hire those repairs out, and if you buy the right properties, you should be able to afford it and have less on your plate.

Can you buy rentals if you live in an expensive market?

The other complaint I hear a lot is that a market is too expensive for rentals, and unfortunately, that can be true. The tough thing about rentals is they do not work well in every market. The higher home prices are, the tougher it is to make money with rental properties. You can still do it, but it takes work. You may have to look at investing out of state or in different asset classes like I do with commercial real estate.

Will you go bankrupt if your tenant leaves?

Investing in rentals can have its downsides as well. I have had tenants leave without notice and I have had to evict tenants. If you own enough rentals for a long enough time you will run into these problems as well! It is very important to have reserves when you buy rentals. That means you have money set aside to cover expenses if a tenant moves out. You also need some money set aside in case a rental needs some repairs before you can rent it again.

I would suggest having at least $10,000 in liquid funds available for vacancies or maintenance. If you don’t have any money and a tenant moves out you could find yourself in a lot of trouble or you may have to sell the property at a discount. The more rentals you have the less one vacancy or bad tenant will hurt you because you will still have money coming in from other properties.

What happens if the housing market crashes again?

A lot of people think that every real estate investor went bankrupt in the housing crash. That is not true, in fact, many investors did just fine. When housing prices decrease it does not mean that rents will. In some cases, rents stay the same or even increase because the demand for rentals goes up. If you buy properties that have cash flow and you do not need to sell them, you can do just fine when housing prices decline. The problems come when you are not making any money on your rentals and the prices decline.

Why does it take so long to buy an investment?

My career is real estate and I was in the business ten years before I bought my first rental property. I knew I should invest in rentals, because of the great returns, tax advantages and other benefits of rental properties. It took me a long time to educate myself about rental properties because they don’t teach you about rentals when you become a real estate agent. I read a lot of books, researched my market, determined market rents and found the best neighborhoods to invest in. I wanted to make sure I knew exactly what I was doing before I bought my first rental property and what the positives and negatives were. It took me a long time to save up the money to buy a rental property and I did not want to screw up and lose it all.

I was okay with taking a long time to buy a rental property because it was a huge purchase and milestone. I also had some major things going on in my life like buying a new house and my wife and I had twins in 2011 (she was pregnant when I bought my first rental). The biggest issue I had was saving up enough money to buy a rental property, but I now realize there are quite a few ways to buy rentals with little money down. There are also ways to speed up the process and educate yourself quickly while also getting involved in the business. One of the great things about rental properties is you do not have to buy a property to start learning or take action. You can look at properties with an agent, talk to a lender, determine values and do many other things to learn about your market and educate yourself before you buy.

Why did it take me so long?

My biggest issue was saving enough money to buy a rental property. There are ways to buy a rental property with little money down, but when I started investing I already had a personal residence and did not know about many of the ways to invest in rental properties with less than 20% down. I was able to save money at some points but then ended up spending it on other things like a new personal residence, a car or vacation. Saving money is the key to being able to make a lot of money with rental properties. Saving money is the key to successfully investing in almost any venture!

Most people have the same problem as I did when I tried to buy my first rental property. They do not have enough money for the down payment, repairs, closing costs and carrying costs. Here is a great article that explains how much money is required to buy a rental property. To get the great returns on rental properties that I get, you will have to use some of your own money. The less money you put down on a property the more expensive the money you borrow will be and the smaller your returns will be. I still like to finance all of my rental properties, but I always put at least 20% down unless using the BRRRR method.

How long will it take you to buy?

When I became serious about investing in rental properties, it still took me over two years to buy my first property. I don’t want to discourage anyone, but it can take some time. During those two years, I was not sitting idle; I was working hard to find a great deal, figure out the best place to invest and make sure I had enough money to invest. You can invest in rentals quicker than I did or it can take even more time depending on your financial situation, education level and drive. Buying rental properties has been one of the best decisions I ever made and rarely do the best things in life come quickly.

Some investors will buy a rental property within one month and some will take five years, while others will never buy a rental. Don’t stress yourself out about buying a property as quickly as you can. The time it takes varies with every person based on the money they have, their goals, their market and much more. I think it does help to set a goal for when you will buy your first rental.

What are the most important things to know?

The reason it takes a long time to invest in rental properties is there is a lot to learn.

- You need to know your local market or the market you plan to invest in. To get the best returns you can’t rely solely on a real estate agent or someone else to tell you what to do.

- You need to decide on the best type of property to invest in. I like single-family homes, but other markets are better for multifamily.

- You need to know how much money you will need to invest and how you will finance the properties.

- You need to know the cash flow and returns you will get from your rental properties.

- You have to find a great team to help you invest including a real estate agent, lender, and contractor.

- The most important factor maybe your own personal goals. Each person has different wants and ambitions in life. Your plan for rental properties will be different depending on what your goals are.

- You need to know what a good rental property is. Not every market and not every house makes a good rental.

- You need to figure out how to fix the properties if you are buying houses that need work.

It takes time to figure out your goals and then decide on a plan of action on how to achieve those goals. Most people give up and do not invest in rental properties because of all the work involved and the time it takes to get started. The good thing about people giving up is it leaves better deals for the rest of us who are willing to do what it takes.

Here is one of the bad rentals I bought:

Where do you start?

If you don’t know where to start and feel overwhelmed, don’t give up! There are many ways to plan and execute a massive task. The first step is to write a list of everything you have to do. Next, break down the list into actionable steps and prioritize the most important steps. From that list begin to create tasks that you can do now to get closer to your goal. Continue to change your task list and create new tasks as you learn more and get closer to your goals. By reading this blog you are already starting. Keep going and do not give up.

You can learn while you take action. Often taking action will be more important than anything you learn. Here is an example of some tasks you can give yourself:

Calculate the money you will need

Many people have an idea of how much the down payment is, but they don’t figure all the costs on a specific house. Pick a house or apartment complex in the area you want to invest in and write out what all the costs will be. If you don’t know what all the costs are, do your best with what you do know and make notes on what you need to learn.

Go see properties in your area

One of the most important things to know as an investor is your market. You can never start learning prices, rents, or neighborhoods soon enough. Go out and see properties ASAP!

Talk to a lender

A lot of people are scared to talk to a lender. I think it becomes real at that point. Now, you may actually figure out you can buy a rental. No matter how scared you are, do it. A lender will tell you what you need and how to get it if you are not ready to buy. It is free and you have no excuse not to talk to one.

Figure the return on as many properties as you can

A lot of people don’t know what they want in an investment. That is why they never buy one. Rentals are a math game. The better the numbers, the better the property, but you have to know the numbers. You need to be able to figure the monthly cash flow based on maintenance, vacancies, mortgage, taxes, insurance, and more. If you need help check out my cash flow calculator.

What education do you need?

Education is a key component of investing in rental properties, but it is not the only part. In order to invest quickly, you have to take action, not just educate yourself. While you are learning about rental properties, there are many things you can do to speed up the buying process.

- Talk to a lender as soon as you can. If you have a credit or qualifying problem they can help you get that solved. The sooner you talk to them the better.

- Start looking at houses in your market area with a real estate agent.

- Start locating contractors and insurance agents.

- Start looking for portfolio lenders.

- Start attending REIA meetings.

Not only does performing these tasks get you involved in real estate, many times these contacts can help you learn about rental properties as well. Local contacts like real estate agents and lenders can educate you about local customs and local markets.

How can your network help you move quicker?

Rental properties are not a way to get rich quickly. It takes time to learn to invest in rental properties the right way so that you can make the most money. There are many ways to get involved in the rental property game quickly, even if you are not buying properties right away. One of the best ways to progress as fast as you can is to get help. This could involve meeting local investors, agents, or lenders as I discussed earlier. However, most agents, lenders, and investors may not know the best ways to buy rentals. It may be better to learn from someone who is doing exactly what you want to do. There are many coaching programs available in the online real estate world. Some are great and some leave something to be desired. I would caution against spending tens of thousands of dollars on online coaching.

Conclusion

There is a lot to learn about investing in rental properties. I still learn new things all the time, and I have been a real estate agent and investors since 2001. Don’t be overwhelmed by all the information and different strategies that involve rental properties. Every market is very different and what I do in my market may not work in your market. Take the steps to learn about your market and develop your own strategy. If you need a little boost or direction for where to start; my program may be able to help you start investing in rental properties a little quicker than doing it all on your own.